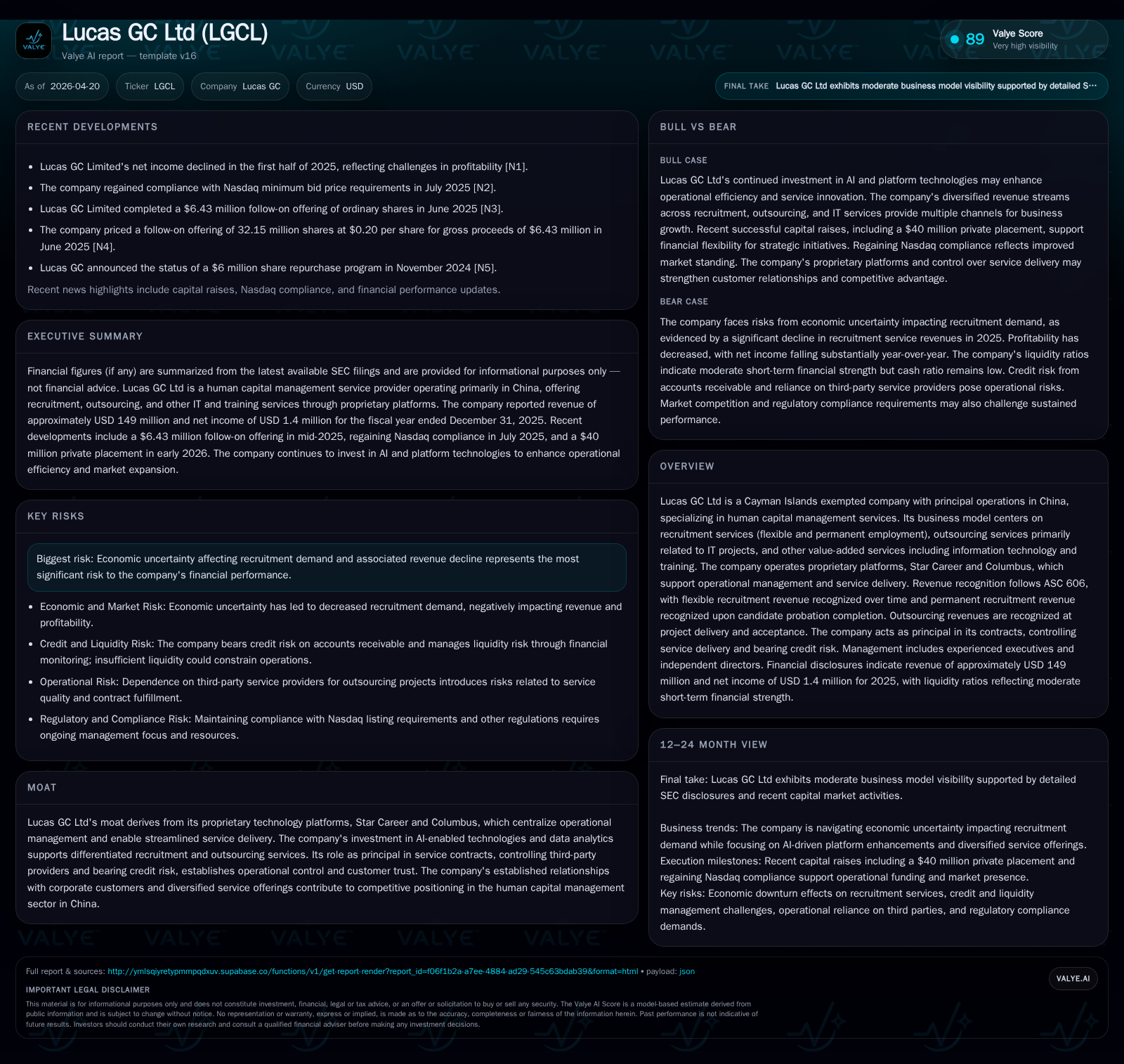

Lucas GC’s $40M Private Placement: Capitalizing on Tech-Driven Human Capital Services in China

Lucas GC Ltd’s recent $40 million private placement strengthens its platform investments as it shifts focus toward margin improvement in China's evolving recruitment and outsourcing market.

In February 2026, Lucas GC Ltd closed a $40 million private placement under Regulation D exemptions, bolstering liquidity to support continued platform upgrades and AI integration. The company operates in China’s human capital management sector, delivering flexible and permanent recruitment alongside IT outsourcing through proprietary platforms that drive operational control and efficiency. While facing economic headwinds that depress recruitment demand, Lucas GC is strategically pivoting from revenue scale to gross margin enhancement, leveraging AI-enabled two-way matching algorithms to expand its user base cost-effectively. Growth is constrained by macroeconomic sensitivity and rising labor costs, but sustained R&D investment underpins differentiation. Upcoming execution milestones will hinge on deploying the new capital toward technology enhancements and improving user retention amid competitive pressures.

Private Placement: Immediate Implications for Growth and Liquidity

Lucas GC Ltd announced a $40 million private placement in early February 2026 [S2], executed under the exemptions afforded by Section 4(a)(2) and Rule 506 of Regulation D of the Securities Act of 1933. The private placement did not involve any public offering or general solicitation, targeting accredited investors exclusively. Closing around February 10, the proceeds are earmarked for general corporate purposes, broadly encompassing working capital needs and investments in technology upgrades that are critical for maintaining Lucas GC's competitive posture.

This fresh influx of capital bolsters the company's liquidity position substantially, enabling a more aggressive posture towards R&D investments particularly focused on enhancing its PaaS platforms — Star Career and Columbus — which form the backbone of service delivery [S1]. The timing of this raise aligns with strategic priorities set forth in the latest annual report emphasizing margin expansion over topline scaling.

Business Model Analysis: Technology-Powered Recruitment and Outsourcing Solutions

Lucas GC operates a multi-service human capital management model primarily focused on China’s professional labor market. It offers flexible recruitment (short-term engagements), permanent recruitment (longer-term talent placement), outsourcing services predominantly tied to IT projects, alongside value-added offerings such as training programs [S1]. The company recognizes revenue under ASC 606 principles with flexible recruitment revenues recognized over time as services are rendered, while permanent placements are accounted for upon candidate probation completion. Outsourcing revenues become recognizable upon project delivery acceptance.

Crucially, Lucas GC acts as the principal in contractual relationships controlling service delivery processes from end-to-end and bearing relevant credit risks associated with customer contracts [S1]. This principal role enhances its operational leverage over third-party labor providers and preserves client trust critical for recurring engagements.

The company’s proprietary Star Career platform facilitates recruitment activities while the Columbus platform manages operational workflows across outsourcing projects. Both platforms incorporate AI-driven algorithms enabling precise two-way matching — connecting job seekers' preferences with employer requirements efficiently — reducing reliance on costly sales or manual matchmaking efforts. Additionally, data analytics capabilities enhance decision-making both internally and for client enterprises.

Competitive Positioning within China’s Human Capital Management Market

The Chinese human capital management market remains highly fragmented with many smaller operators competing on price. Against this backdrop, Lucas GC’s moat stems from technological integration that leverages multidimensional datasets combined with AI algorithms fostering superior matching accuracy . This technological edge creates a virtuous cycle where better matches attract more users, enlarging data pools that further enhance platform intelligence.

Operational control as principal contractor allows Lucas GC to optimize service quality standards across dispersed third-party labor providers — an important trust signal for corporate clients sensitive to workforce quality variability [S1]. Moreover, established long-term relationships with corporate customers support service diversification across different industry verticals.

However, industry challenges persist including intense price competition compressing margins and inflationary labor costs exerting upward pressure on worker compensation necessary to retain flexible talent pools . Regulatory oversight related to employment services also imposes compliance costs affecting operating efficiency.

Growth Opportunities Enabled by AI and Data Analytics Platforms

Growth drivers focus principally on expanding platform capabilities through continuous R&D investment aimed at upgrading AI functionalities embedded within Star Career and Columbus [S1]. Management highlights ongoing increases in R&D spend devoted to technology payrolls, third-party technology services for platform development, and data analysis functions supporting operational scalability.

Advancements in AI capabilities are expected to improve both demand-side (corporate client) customization and supply-side (worker) user experience by boosting matching accuracy and real-time responsiveness. Enhancements in two-way matching synergy can drive positive network effects facilitating organic user base expansion without parallel increases in user acquisition costs — key given the company’s strategic realignment from revenue scale maximization towards value optimization through gross margin enhancement [S1].

Moreover, product innovations including broader workforce coverage across multiple industries strengthen cross-selling opportunities for complementary value-added services such as training — enhancing client stickiness beyond initial recruitment or outsourcing projects.

Constraints: Economic Sensitivity and Cost Control Challenges

Lucas GC's business model exhibits structural sensitivity to macroeconomic conditions influencing corporate hiring activity within China’s tertiary industries [S1]. Economic uncertainty in recent years has dampened recruitment demand causing a shift towards higher-margin outsourcing solutions favored by clients aiming to reduce fixed personnel costs during uncertain cycles [S18].

Rising labor costs constitute an enduring challenge impacting unit economics especially within flexible recruitment where fee rates paid to workers underpin cost structures . Concurrently, higher absolute research and development expenses represent an increasing share of total costs given the prioritization of platform enhancements — creating a trade-off between technological differentiation investment versus near-term margin pressures [S1], [S7]. Balancing spending between marketing activities designed now more around targeted value generation rather than broad growth initiatives adds another layer of operational discipline needed.

Capital Deployment and R&D Investment Priorities

Capital allocation post-private placement centers on augmenting technology infrastructure essential for sustaining Lucas GC's differentiated service offerings [S2], supported contextually by capex trends detailed in the annual report indicating roughly doubling capex year-over-year peaking at approximately $11.9 million in 2025 [F1], [S7], [S19], [S28].

Research and development outlays continue their upward trajectory driven by payroll-related costs for technologists plus payments to external tech service providers engaged specifically on AI upgrades within the core PaaS systems [S1]. Such investments underpin anticipated gains in user matching precision as well as operational efficiencies.

Simultaneously, marketing expense evolution points towards scaled-back mass acquisition spending but allocation favoring optimized campaigns targeting higher-value corporate clients who contribute disproportionately to the outsourcing revenues segment demonstrating better margin profiles [S1], [S19]. These moves align with broader corporate goals shifting focus from top-line growth scale towards sustainable profitability gains.

Financial Overview: Recent Performance Trends and Capital Structure Metrics

Lucas GC's financial results reveal a slowing revenue environment alongside contracting profitability metrics reflecting economic headwinds plus ongoing investment phases. Revenue grew modestly by approximately 2.3% year-over-year reaching $149 million USD in fiscal 2025 following declines from prior years largely attributed to weaker recruitment demand balanced partially by stronger outsourcing growth [F1], [S1].

Operating income declined meaningfully -26.7% year-over-year to approximately $2.8 million USD with net income contraction of over 74%, attributable primarily to elevated R&D expenses combined with softer revenues [F1]. Despite these earnings pressures, operating cash flow improved significantly (+83%, $5 million USD approx.) as working capital management tightened including collections efforts—indicative of operational discipline gains amid transition phases [F1].[F1]

Liquidity ratios remain robust post-capital raise with a current ratio near 1.61 ensuring comfortable buffer against short-term obligations while elevated capex underscores active deployment into future-oriented assets such as software platforms critical for competitive positioning.[F1]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 149 | 1 | 5 | 3 | +2.3% | -74.3% |

| 2024 | 146 | 5 | 3 | 4 | -29.8% | -50.2% |

| 2023 | 208 | 11 | -5 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | 3.1 |

| 2024 | -3 | 15.1 |

| 2023 | -7 | 40.0 |

Source: SEC companyfacts cache [F1].

Key Investor Takeaways and Near-Term Execution Milestones

The $40 million private placement stands as a pivotal catalyst enabling Lucas GC Ltd to continue investing heavily in proprietary technologies critical for sustaining differentiation within a highly competitive China-based human capital marketplace. Execution emphasis will rest on effectively deploying these funds into accelerating AI-driven platform upgrades aimed at improving matching efficacy resulting in better user engagement metrics—a leading indicator of ongoing value creation potential.

Investor attention should monitor quarterly disclosures concerning progress against R&D milestones particularly relating to Star Career & Columbus platform enhancements—their impact on gross margins—and shifts in customer acquisition efficacy as marketing strategies evolve toward more value-centric models consistent with management's margin optimization goals outlined at year-end reporting.

Setbacks related to external macroeconomic factors threatening recruitment demand or unexpected cost escalations could weigh considerably on near-term profitability prospects underscoring need for prudent cost control coupled with strategic agility.

Overall cautious optimism arises from the combination of strengthened balance sheet flexibility post-private placement coupled with clear strategic intent driving technology-led differentiation designed to weather cyclical volatility inherent in workforce services sectors within China.

Disclaimer: This analysis is based solely on publicly available filings referenced herein including Form 6-K dated February 10, 2026 ([S2]) and Form 20-F dated April 20, 2026 ([S1]) as well as companyfacts data ([F1]). It does not constitute investment advice or recommendations regarding securities of Lucas GC Ltd.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments