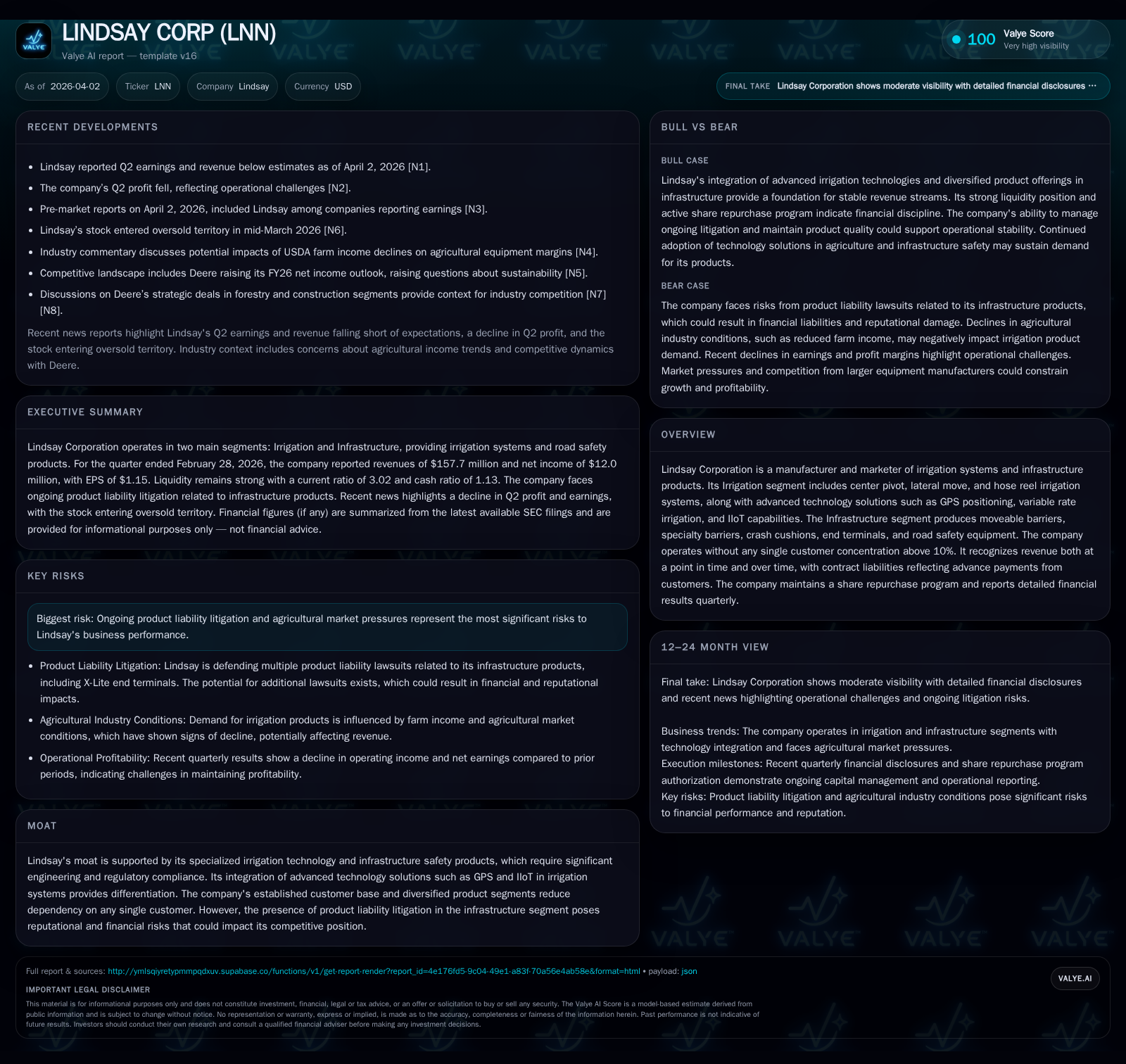

Lindsay Corporation’s Stalled Momentum and Legal Risks Amid Agricultural Market Headwinds

Lindsay Corporation contends with flat revenue growth and mounting litigation pressures while investing heavily in irrigation technology innovation.

Lindsay Corporation's annual financials show a plateau in revenue growth alongside declining operating income and rising capital expenditures, reflecting margin pressures and investment in advanced irrigation solutions. Its specialized irrigation segment leverages GPS, variable rate irrigation, and IIoT to sustain competitive differentiation amid challenging agricultural conditions. However, ongoing product liability litigations related to its X-Lite end terminal create operational uncertainty, despite no loss accruals recorded. The company balances capital returns through dividends and modest share buybacks, supported by solid cash flow generation and a healthy liquidity profile. Investor attention should focus on the progression of litigation cases and agricultural sector developments influencing contract flows.

Revenue Plateau After Earlier Expansion: Key Drivers Behind Recent Performance

Lindsay Corporation's latest fiscal year (FY2024) results reflect a pronounced stalling in top-line momentum. Revenues edged up a mere 0.3% to $676.4 million from FY2023's $674.1 million, far below the robust growth patterns seen earlier (FY2022 revenue was $770.7 million) [F1]. Operating income contracted notably by 13.8% from $102.2 million to $88.1 million over the same period, highlighting compression in margins potentially from a combination of elevated input costs or altered product mix within both irrigation and infrastructure lines [F1]. Net income remained relatively stable at $74.1 million, a modest increase of 2.3% year-over-year.

Agricultural sector headwinds have exerted downward pressure on equipment demand industry-wide; analyses point to softening farm incomes impacting capital expenditures among growers [N3], a key end market for Lindsay's irrigation products. Competition within precision ag markets also intensifies during shifting customer budgets [N12],[N13]. The plateauing revenue reflects these dynamics alongside cautious spending signals across its core customer base.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2024 | 676 | 74 | 133 | 88 | +0.3% | +2.3% |

| 2023 | 674 | 72 | 120 | 102 | -12.5% | +10.6% |

| 2022 | 771 | 65 | 3 | 95 | +35.8% | +53.8% |

| 2021 | 568 | 43 | 44 | 54 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2024 | 16 | 90 | 13.9 |

| 2023 | 15 | 101 | 15.9 |

| 2022 | 15 | -13 | 16.6 |

| 2021 | 14 | 17 | 12.6 |

Source: SEC companyfacts cache [F1].

Financial data shows stagnation in revenues contrasts with selective investments reflected in capex increases.

Technology-Driven Irrigation: Differentiation and Sector Tailwinds

The Irrigation segment remains Lindsay's primary engine, incorporating advanced technology suites that distinguish its portfolio amid competitive precision agriculture solutions [S2]. Core offerings include center pivot systems enhanced with GPS positioning for automated guidance, variable rate irrigation technologies enabling water application tailored to spatial variability in fields, and IIoT frameworks for remote monitoring and scheduling.

These features shape Lindsay's moat by embedding engineering complexity and software integration that are difficult to replicate quickly . Revenue recognition practices indicate a blend of point-in-time sales alongside over-time contract fulfillment — often tied to multi-year installations or service agreements — signaled by contract liabilities that suggest deferred revenue streams across these projects [S2]. This layered approach supports stability amidst fluctuating sector demand.

While the broader agricultural market softness tempers growth prospects, the pivot towards sustainable water management positions Lindsay well with customers who prioritize efficiency gains aligned with environmental compliance trends ([N1]). Continued investment in R&D appears vital to maintaining this edge amid peer moves.

Infrastructure Segment: Litigation Risks Temper Operational Outlook

Lindsay’s Infrastructure segment faces significant reputational and operational challenges due to ongoing product liability litigation related to the X-Lite end terminal highway barriers [S5][S8][S18][S24]. Lawsuits allege defective design causing failures during vehicle collisions resulting in removal mandates by Missouri transportation authorities with claims encompassing strict liability, negligence, breach of warranties, fraud allegations, and public nuisance [S18]. Similar cases filed under state Fraud Against Taxpayers Acts (FATA) in Tennessee and California courts introduce jurisdictional complexity [S28].

Despite management denying the probability of loss based on current evidence — leading to no accrual for liabilities — the claims create material uncertainty around future capital requirements or reputation damage that could constrain the segment’s growth trajectory or pricing power [S5][N9]. The company’s insurance coverage provides some mitigation but does not eliminate risks inherent in protracted litigation processes, which may attract further industry scrutiny given precedent judgments against competitors.

Regulatory compliance complexities around barrier safety standards heighten scrutiny within this product line; thus investor sentiment remains cautious pending definitive judicial outcomes.

Capital Deployment Priorities: Dividends, Share Repurchases, and Investment Spending

Lindsay has sustained disciplined capital allocation policies balancing shareholder returns against reinvestment needs amid mixed operational results [F1][S9][S23][S25]. Dividends paid increased gradually from $14.6 million in FY2022 to $15.7 million in FY2024, reflecting consistent payout commitment.

Share repurchases were modest over recent years relative to prior multi-year programs scaled down after FY2018; FY2024 repurchases totaled $11.5 million compared with historically larger buys exceeding $48 million several years ago [F1]. This restrained buyback approach suggests caution given legal uncertainties.

Rising capex spending—from approximately $18.8 million in FY2023 to nearly $42.5 million in FY2024—reveals an intensified focus on growth investing especially aligned with advanced irrigation technology improvements and facility enhancements [F1]. This tradeoff between distributing cash and funding innovation highlights strategic prioritization challenges as Lindsay seeks to combat structural headwinds.

Financial Returns and Balance Sheet Strength: ROE, Cash Flows, and Liquidity Profile

The company’s return on equity approximated a healthy ~13.9% in FY2024 calculated as net income relative to year-end shareholders’ equity [$74M / $533M] providing moderate shareholder value creation despite margin pressure [F1]. Notably, operating cash flows grew by about +11% year-over-year reaching $133 million due to effective working capital management even as revenues stagnated.

Free cash flow generation—operating cash flow minus capex—remained solid at roughly $90 million supporting both dividend payouts and measured debt reduction efforts [F1]. Balance sheet liquidity positions are strong; current assets stand at about $499 million versus current liabilities near $165 million delivering a current ratio above three times—a robust cushion for near-term obligations including litigation-related contingencies if required [F1][S4][S6][S11].

Long-term debt remains manageable at approximately $115 million dominated by Series A Senior Notes maturing beyond one year without significant immediate repayment pressure providing financial flexibility for strategic initiatives or reserve funding should legal settlements arise.

Forward Indicators to Watch: Market Conditions, Regulatory Outcomes, and Contract Timing

Looking forward, several key external factors warrant close observance given their potential impact on Lindsay’s operational cadence:

- Agricultural sector metrics such as USDA farm income trajectories will influence grower spending capacity on irrigation upgrades impacting order volumes [N3].

- Developments in ongoing legal disputes particularly outcomes of similar qui tam suits filed since late-2023 under Tennessee and California Fraud Against Taxpayers Acts carry implications for contingent liabilities or settlement costs that could reshape risk profiles [S28].[N7]

- Upcoming quarterly earnings cycles should offer insight into how strong backlog execution is translating into realized revenues amidst economic challenges as highlighted recently by missed Q2 estimates raising caution flags [N1].[N2]

- Contract backlog levels disclosed may provide leading visibility on near-term performance backed by milestone-based billing mentioned within contract asset/liability disclosures signaling multi-month delivery commitments which could buffer volatility if effectively managed [S2].

Investors would benefit from monitoring court rulings’ timing combined with sector cyclical indicators for irrigation demand that collectively will inform risk-return tradeoffs inherent within Lindsay’s combined infrastructure-irrigation business model.

This analysis synthesizes public disclosures as of April 2026 without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments