Logistic Properties of the Americas: Portfolio Expansion and Lease Diversification Drive Growth with Emerging Market Regulatory Risks

LPA capitalizes on strategic logistics real estate developments across Latin America, targeting mid-to-high teen returns amid an evolving regulatory landscape.

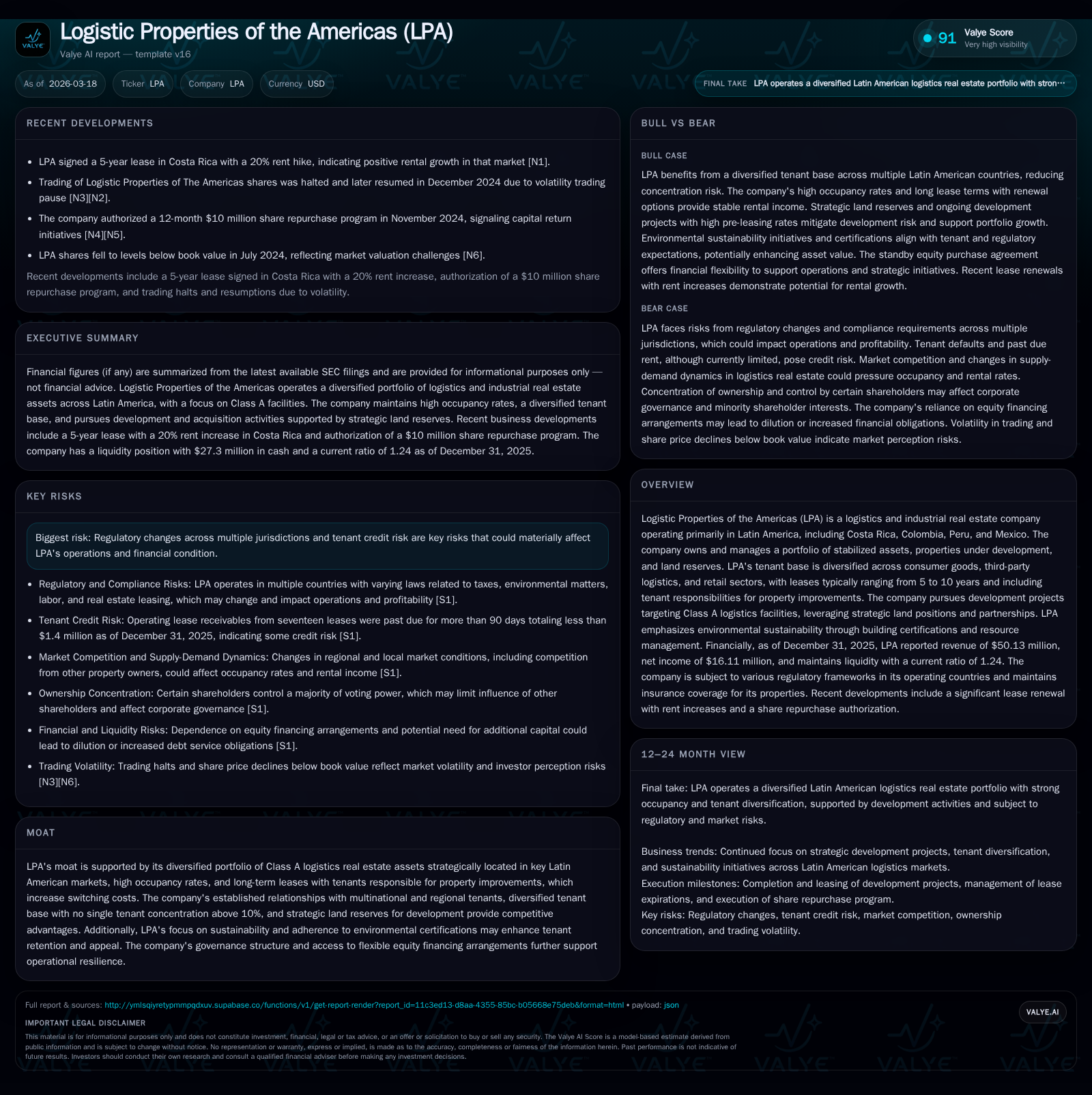

Logistic Properties of the Americas (LPA) has demonstrated notable growth in revenues and net income through a diversified portfolio of Class A logistics assets across multiple Latin American countries. Their rental business benefits from long-term leases with multinational tenants and a development pipeline that leverages sizeable land reserves primarily in Colombia and Peru. Despite promising expansion prospects, LPA faces regulatory complexity and tenant credit risks inherent to emerging markets. Capital allocation has focused on development yield premiums over stabilized assets, supported by a recent equity purchase agreement to provide financial flexibility.

Company Overview and Historical Performance

Logistic Properties of the Americas (LPA) specializes in logistics and industrial real estate within Latin America, focusing its operations mainly on Costa Rica, Colombia, Peru, and Mexico. The firm's asset base encompasses stabilized properties generating rental income, active developments aiming at Class A facilities, as well as extensive land reserves poised for future projects [S1].

Financially, LPA reported significant top-line expansion with revenues rising from approximately $39.4 million in 2023 to over $50.1 million in 2025—representing a compounded upward trajectory punctuated by a 14.3% YoY increase from 2024 to 2025 [F1]. Net income performance has been volatile but significantly improved to $16.1 million in 2025 after experiencing a loss the year prior; this reversal reflects stronger occupancy rates alongside enhanced operational management controlling costs effectively [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 50 | 16 | +14.3% | +182.9% |

| 2024 | 44 | -19 | +11.2% | -371.5% |

| 2023 | 39 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 5.0 |

| 2024 | -7.2 |

| 2023 | 2.7 |

Source: SEC companyfacts cache [F1].

The rebound between 2024-25 signals effective capital deployment in line with LPA’s strategy leveraging its development pipeline.

Operating Portfolio and Tenant Base

As of December 31, 2025, LPA’s portfolio aggregates roughly 7.56 million square feet combining owned and right-of-use assets—including operating properties with an exceptional occupancy rate near or at 100%. The geographic distribution is weighted heavily toward Costa Rica for stabilized holdings (2.5 million sq ft), complemented by significant presence in Colombia (1.25 million sq ft) and Peru (~1.6 million sq ft), along with emerging assets in Mexico [S1][S8].

Tenant composition is broadly diversified:

- Consumer Goods: ~35.8% of rental revenue

- Third-Party Logistics: ~29.1%

- Other Retail: ~26.8%

Major tenants like Kuehne + Nagel (~7.3%) represent well-known logistics operators with regional penetration; importantly no single tenant holds more than approximately 10% leased space ensuring resilience against individual tenant credit events [S8]. Leases generally run just under five years with tenants responsible for internal property improvements—this design reduces turnaround costs on vacancy and enhances switching costs.

Growth Prospects

LPA pursues growth chiefly through selective development of Class A facilities often situated on strategic land parcels already held within its portfolio—a cost-efficient approach that yields materially higher returns than market-traded stabilized assets by an estimated margin of two to three percentage points on yield-on-cost basis [S4]. Full ownership projects target mid-to-high teen returns on equity; joint ventures or partnerships with local actors offer potential for even higher return spreads while leveraging fee structures.

The company’s land bank totals approximately $40 million fair value spread over Colombia (72.7%) and Peru (27.3%), representing over one-half million square feet poised for phased development aligned to market demand cycles [S15]. Development activity is buttressed by thorough location analysis emphasizing established infrastructure access routes critical to logistics functionality.

Future growth may encounter limitations if regulatory shifts increase compliance burdens or if supply-demand imbalances dampen achievable rents; nevertheless ongoing infrastructure improvements across Latin American trade corridors provide tailwinds supporting logistics real estate demand.

Capital Allocation and Financial Health

As of year-end 2025, LPA maintains robust liquidity with $27.3 million in cash equivalents relative to current liabilities totaling approximately $32 million—yielding a current ratio around 1.24—indicative of prudent working capital management given the capital-intensive nature of real estate development projects [F1][S16].

Capital expenditures reflect continued investments into both ground-up developments and acquisition opportunities aimed at deepening presence within key markets [S7][S9]. Notably on September 23rd, 2025 LPA executed a Standby Equity Purchase Agreement enabling issuance up to $30 million shares subject to terms providing financial flexibility for opportunistic transactions or balance sheet fortification without immediate dilution pressure [S7].

Dividend policy remains discretionary; payout decisions are contingent upon operating performance as well as distributions received from subsidiary LLP entities—which themselves face local market variability—thus making dividends uncertain near term [S13]. Given these dynamics capital appreciation rather than direct income may constitute primary shareholder gains presently.

Risk Factors Contextualized

Operating across multiple Latin American jurisdictions exposes LPA to complex regulatory environments encompassing varied tax codes, urban zoning laws, labor regulations, environmental compliance requirements including sustainability standards integral to their Class A positioning—all necessitating vigilant management oversight to mitigate potential fines or operational disruptions [S5][S14][S18][S22].

Emerging economies also introduce tenant credit risks exacerbated by volatile economic cycles which may impair rent collections despite historically low past-due receivables reported under $1.4 million past ninety days as of December 31st, 2025—a manageable level but one warranting continuous monitoring due to industry cyclicality [S4]. Ownership concentration is notable; directors/officers control about 83.5% voting power potentially limiting minority shareholder influence on strategic decisions introducing governance considerations unique within such controlled companies listed on NYSE American exchanges [S23][S21].

Legal exposure is inherent given Cayman Islands incorporation complicating enforcement actions related to U.S securities laws; shareholders face challenges executing cross-border claims particularly where senior officers reside outside U.S jurisdictional reach—a common issue among foreign private issuers headquartered offshore but listed publicly here [S10][S12][S20].

Outlook Considerations

Future milestones worth tracking include successful completion and stabilization of ongoing development projects—especially in Peru where properties under right-of-use exhibited increasing leased rates approaching full occupancy nearing late-2025 projections—and potential expansion into adjacent logistic hubs pending capital availability balanced against geographic concentration risk.

Monitoring shifts in regulatory frameworks related to property leasing terms or enhanced environmental legislation will also be pivotal given their impact on operating freedom and cost structures.

Furthermore, adoption or maintenance of sustainability certifications branded by LPA could bolster tenant retention amid growing corporates’ ESG commitments influencing site selection criteria within Latin American logistics sphere.

Conclusion

Logistic Properties of the Americas stands as a growing contender within Latin America's industrial real estate sector by forging a foothold through carefully targeted developments combined with diversified tenant leasing strategies—offsetting inherent emerging-market idiosyncrasies via strong liquidity posture backed by flexible equity financing options.

However investors should remain cognizant of layered regulatory complexities alongside ownership concentration dynamics potentially shaping future governance outcomes.

This memorandum is prepared solely for informational purposes based on publicly available data as of March 18th, 2026 sources cited throughout the document without any recommendation regarding trading or investment decisions involving Logistic Properties of the Americas securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments