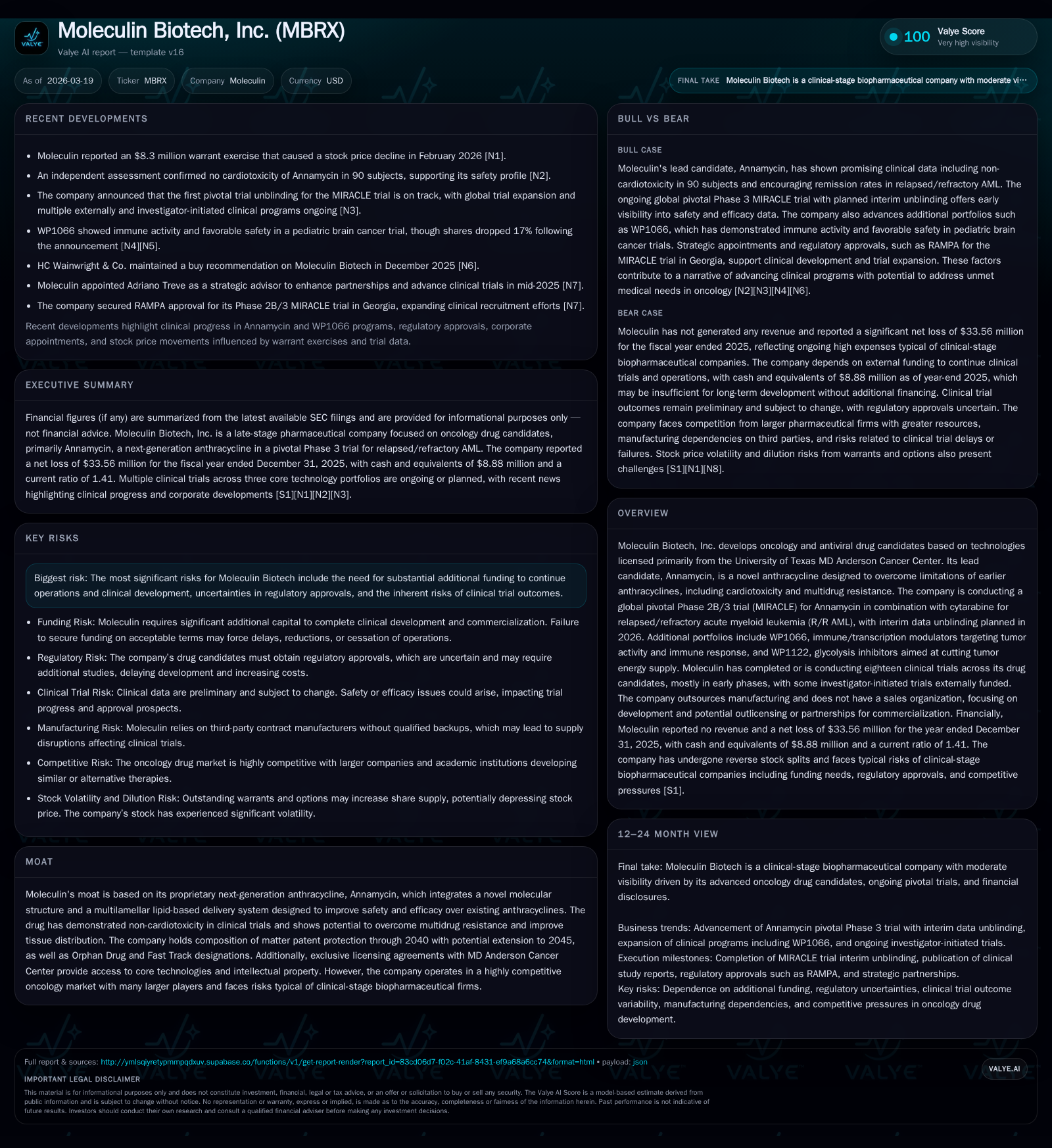

Moleculin Biotech’s Pivot to Pivotal Trial Success Amid Persistent Cash Burn and Regulatory Risks

Moleculin Biotech advances its lead oncology candidate Annamycin toward pivotal Phase 3 milestones while managing cash constraints and development uncertainties.

Moleculin Biotech, a clinical-stage biopharmaceutical company licensed primarily from MD Anderson Cancer Center, is focused on developing innovative oncology drug candidates, notably Annamycin for relapsed/refractory acute myeloid leukemia (R/R AML). The company is conducting a global pivotal Phase 2B/3 trial ("MIRACLE") with interim data expected in mid-2026, representing an inflection point for validation. Historically, Moleculin has operated at operating losses exceeding $25 million annually with no revenue, relying on capital raises including recent warrant exercises. The company faces significant risks typical of clinical-stage biotech players, including funding challenges, regulatory unpredictability, and patent litigation risks stemming from its reliance on university-licensed technology and limited manufacturing partners. Returns have been negative to date with a cash runway requiring near-term capital raising or partnership moves. Future growth hinges heavily on successful clinical trial outcomes, regulatory approvals, and strategic capital management given the competitive oncology landscape and high orphan drug development costs. Monitoring Annamycin’s MIRACLE trial readouts constitutes a key milestone event for the company’s trajectory and valuation outlook.

Company Overview

Moleculin Biotech, Inc. is a clinical-stage pharmaceutical developer specializing in oncology and antiviral drug candidates based predominantly on proprietary technologies licensed from the University of Texas MD Anderson Cancer Center in Houston. Its flagship drug candidate, Annamycin (naxtarubicin), represents a "next-generation" anthracycline designed specifically to address safety issues such as cardiotoxicity seen in earlier anthracyclines while overcoming multidrug resistance mechanisms that limit efficacy. This candidate embodies a unique multilamellar lipid-based delivery system meant to optimize tissue distribution and broaden its therapeutic window.

Besides Annamycin, Moleculin leverages two additional technology portfolios: WP1066 compounds that modulate immune signaling pathways to inhibit tumor growth and WP1122 glycolysis inhibitors targeting cancer cell energy metabolism. Collectively, these platforms have supported or initiated eighteen clinical trials (investigator-initiated or company-sponsored) mostly in early phases but include some progressing into Phase 2 or beyond [S1].

Historical Financial Performance

Moleculin remains pre-revenue as it pursues clinical validation of its pipeline candidates. The company’s financials reflect heavy investment in R&D without any commercial sales recorded through FY2025 [F1]. The following table summarizes key financial metrics for the last four fiscal years:

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -34 | -23 | -25 | -54.2% |

| 2024 | 0 | -22 | -24 | -27 | +26.9% |

| 2023 | 0 | -30 | -24 | -30 | -2.6% |

| 2022 | 0 | -29 | -28 | -31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -23 | -223.6 |

| 2024 | -24 | -364.0 |

| 2023 | -24 | -114.2 |

| 2022 | -28 | -55.6 |

Source: SEC companyfacts cache [F1].

Operating expenses have shown modest improvement between FY2024 and FY2025 (-5.8%) though net losses deepened due primarily to non-operating items [F1]. Operating cash flow remains consistently negative reflecting ongoing investment in development without commercial inflows.

Capital expenditures are minimal relative to operations, highlighting focus on outsourced clinical activities rather than fixed assets [F1]. Equity declined substantially over this period due to accumulated losses.

Growth Prospects and Pipeline Milestones

The cornerstone growth opportunity lies in successfully advancing Annamycin through the MIRACLE trial — a global pivotal Phase 2B/3 study evaluating the combination of Annamycin with cytarabine for relapsed/refractory AML patients [S1]. Preliminary blinded data has been released with an interim unblinding expected mid-2026 followed by further data later that year which could validate registration-enabling efficacy.

Positive results would enable potential regulatory submissions leveraging orphan drug designation benefits held by Annamycin [S1]. Parallel portfolios WP1066 and WP1122 continue investigator-initiated trials and preclinical work aiming for collaborations or licensing.

Challenges include reliance on single-source suppliers for active pharmaceutical ingredients (API), typical biotech clinical uncertainties like patient enrollment or adverse events, plus limited prior experience conducting pivotal trials independently [S1][S4]. International regulatory processes add timing uncertainty given differing country requirements [S19].

Capital Allocation & Financial Health

Capital allocation focuses almost exclusively on research and development without dividend payments or share repurchases due to funding needs [F1],[S1]. With net losses exceeding $33 million in FY2025 alongside negative operational cash flows near $23 million annually [F1], liquidity constraints are significant.

Year-end cash reserves were about $8.9 million against current liabilities of approximately $6.85 million yielding a current ratio of 1.41 indicating manageable short-term liquidity but limited runway absent new financing [F1]. A recent warrant exercise raised about $8.3 million in February 2026 contributing fresh capital but also increased share dilution pressure coinciding with stock price weakness [N1][S3].

Given planned pivotal trial expenses plus milestone payments owed under licensing agreements with MD Anderson Cancer Center—potentially several hundred thousand dollars—the company will likely require additional equity financing or strategic partnerships within this calendar year to maintain operations through upcoming critical data readouts [S18][S26].

Competitive Moat & Risks

Annamycin’s differentiation arises from its novel chemical structure designed to reduce cardiotoxicity common among older anthracyclines while overcoming multidrug resistance mechanisms, supported by its proprietary lipid-based delivery platform enhancing therapeutic index [S1]. Exclusive licensing arrangements provide patent protection through at least 2040 plus orphan drug exclusivity advantages.

However, risks include intense competition from large pharmaceutical companies active in oncology; intellectual property challenges including patent infringement claims or invalidation threats potentially requiring costly litigation; dependence on third-party manufacturers vulnerable to supply disruptions; evolving healthcare regulations affecting pricing; and clinical trial execution risks such as enrollment delays or adverse events [S4][S12][S24]. Additional operational risks stem from cybersecurity vulnerabilities and legal exposures typical for biopharma firms [S22].

Outlook & Critical Milestones To Watch

The primary near-term catalyst is the interim data unblinding from the MIRACLE trial expected mid-2026 which may provide early efficacy and safety signals ahead of finalizing Part A of this two-part study [S1]. Favorable outcomes could spur partnering interest or improve fundraising prospects; unfavorable results might severely impact valuation.

Continued regulatory engagement especially FDA acceptance of international trial data plus supply chain reliability remain essential operational considerations [S19][S21]. Investors should monitor communications regarding capital strategy as expenditures ramp toward potential NDA submission milestones.

Conclusion

Moleculin Biotech exemplifies a late-stage biotech facing high scientific promise anchored by academic-licensed drugs alongside substantial financial strain and regulatory/commercial execution risk common among developmental companies without revenues yet.

Its future depends critically on success in the MIRACLE pivotal trial for Annamycin which if achieved could transition it toward commercial viability amid intense oncology competition.

Monitoring upcoming clinical milestones alongside financing developments is essential to assess evolving risk/reward dynamics.

This analysis is based exclusively on publicly filed documents including SEC filings up through March 2026, public news sources as cited.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments