Mountain Crest Acquisition 6 Corp IPO Proceeds Held for Strategic Deal Execution in Competitive SPAC Space

Mountain Crest Acquisition 6 Corp closed a $60 million IPO and holds those proceeds in trust as it seeks a target business combination; the latest quarterly filing reflects ongoing risk factors and operating losses typical of a newly formed SPAC.

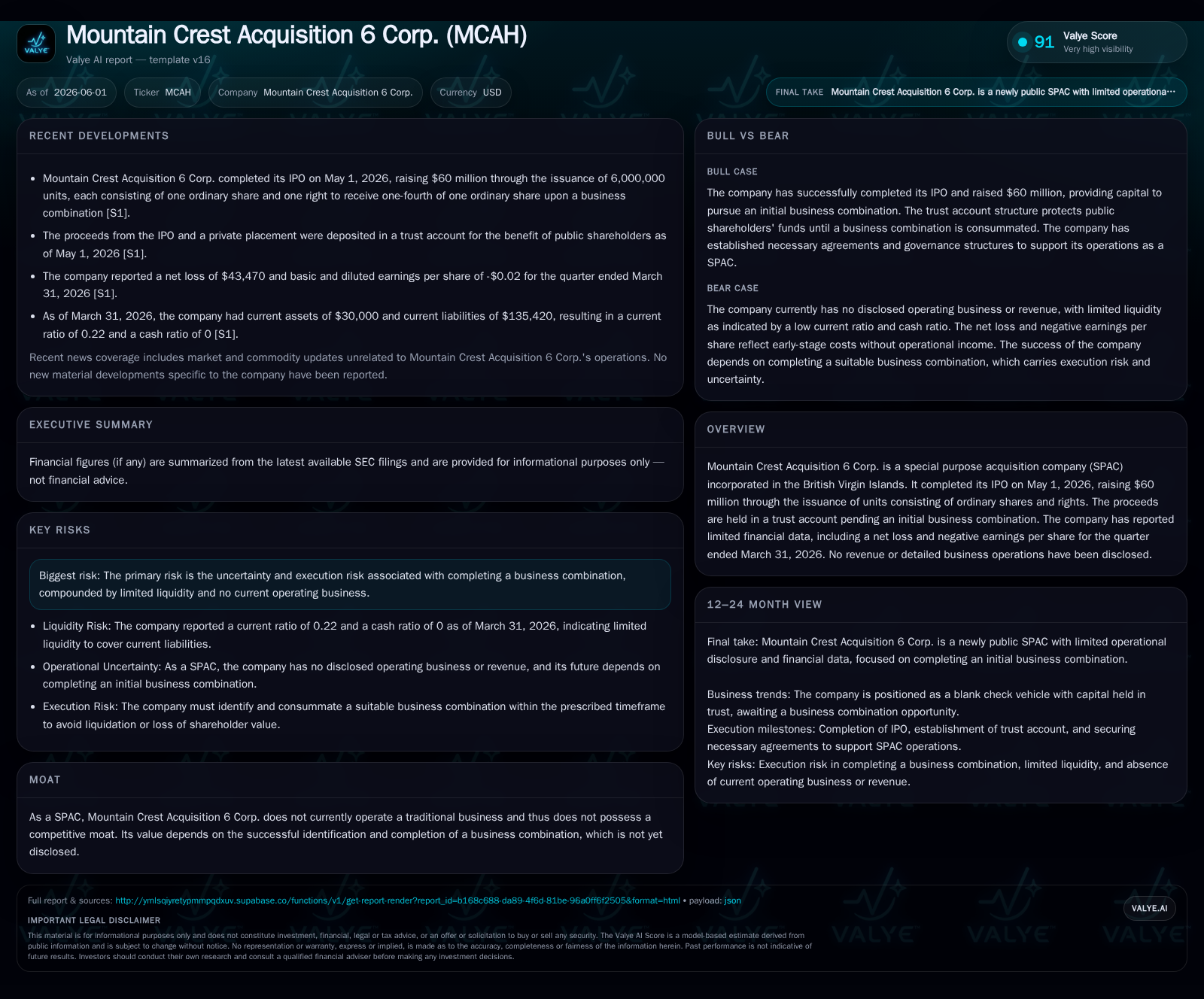

Mountain Crest Acquisition 6 Corp (MCAH) completed its IPO in early May 2026, raising $60 million through the sale of units comprising ordinary shares and detachable rights. These funds remain securely held in a trust account pending execution of an initial business combination, with no revenues or commercial operations reported yet. The company's most recent quarterly report reaffirms previously disclosed risk factors, highlights a net loss consistent with startup costs, and reflects a liquidity profile typical for a blank-check company without operating cash flows. MCAH's future growth depends entirely on identifying and consummating a business combination within regulatory timelines amid the evolving, competitive SPAC market environment.

IPO Closing and Latest Filing Snapshot

Mountain Crest Acquisition 6 Corp finalized its initial public offering on May 1, 2026, issuing 6 million units at $10 per unit to raise gross proceeds of $60 million. Each unit consists of one ordinary share and one right entitling holders to receive one-fourth of an ordinary share upon consummation of an initial business combination [S3]. Simultaneously, a private placement involving the Sponsor secured additional capital via purchase of private units at the same price. The combined proceeds were deposited in a trust account as stipulated by SEC regulations to safeguard investors’ capital against premature use [S3], [S9].

The firm’s first quarterly report ending March 31, 2026—covering pre-IPO periods—discloses operating losses totaling around $43,470 attributable largely to administrative expenditures typical for corporate formation stages. No revenues have been recorded to date as MCAH operates solely as a special purpose acquisition company without any commercial operations or product offerings yet [F1], [S2]. Risk factors in the IPO prospectus remain fully applicable with no new material updates observed in the latest filings [S10].

SPAC Business Model Mechanics Explained

MCAH exemplifies the classic SPAC structure: raising capital from public markets through an IPO by issuing units that blend immediate equity stakes with contingent conversion rights designed to preserve shareholder upside post-merger. The company holds proceeds in a managed trust account, securing principal amounts until an acquisition target is identified and approved by shareholders. This mechanism protects investors from misappropriation risks while maintaining pressure on sponsors to find value-accretive combinations within prescribed timelines.

The absence of current revenues underscores that value creation is postponed until the consummation of an initial business combination—that event being pivotal for transforming MCAH from a shell entity into an operational enterprise. Thus far, MCAH has not disclosed any acquisition targets or sectors under consideration.

Sponsor Participation and Unit Structure

Sponsor economics and alignment play critical roles in the SPAC lifecycle. In MCAH’s case, the sponsor purchased private units aggregating to $900,000 at IPO pricing terms [S11]. These private units mirror public ones but come with transfer restrictions limiting sponsor sales before initial business combination completion—intended to demonstrate sponsor commitment and reduce selling pressure immediately post-deal announcement

Further details embedded in registration rights agreements echo typical industry practices ensuring sponsors can register their holdings when needed but are incentivized to support long-term value realization. Sponsor lock-ups also help stabilize stock liquidity during the post-IPO but pre-combination phase.

Market Positioning within the SPAC Sector

The competitive backdrop for SPACs continues evolving after several years of soaring popularity followed by regulatory tightening since late 2024, notably curbing speculative issuance volumes and increasing due diligence standards. Investor appetite parallels this sentiment shift with heightened caution toward management quality and acquisition pipeline credibility.

Against this backdrop, MCAH enters the market freshly capitalized but untested operationally or strategically beyond filing formalities. Its British Virgin Islands incorporation situates it among offshore-structured vehicles that often attract cross-border deal-making strategies yet face complex regulatory scrutiny regarding disclosure transparency.

In this challenging environment, differentiation depends heavily on sponsorship pedigree, deal sourcing capabilities, and timing precision relative to the limited five-year window typically allowed before liquidation requirements arise within SPAC frameworks.

Growth Potential Through Business Combination Outcomes

MCAH's intrinsic growth prospects rest exclusively on completing an initial business combination targeting an attractive private company with promising fundamentals or sector positioning. Successful deals typically unlock re-rating potential as markets transition valuation focus onto revenue growth trajectories, profitability catalysts, or unique competitive advantages held by the acquired enterprise.

Given no current disclosures on target sectors or pipeline status exist, all prospective value creation remains hypothetical at present. However, robust deal-making capabilities among founders can be expected to identify companies exhibiting structural demand drivers such as scalable revenues, pricing power resilience, or defensible customer relationships.

Risks Linked to Execution Timeline and Liquidity

Execution risk dominates MCAH’s risk profile—as common among newly minted SPACs—stemming from several dimensions: transaction timing constraints impose pressure to identify and close deals within defined statutory periods or return investor funds if unsuccessful; operational costs consume cash reserves independent of revenue generation; shareholder approval dynamics introduce uncertainty around deal closures.

From a liquidity perspective, pro forma current assets excluding trust balances stand at about $30,000 while current liabilities reach approximately $135,420 resulting in a low current ratio near 0.22 at quarter end—normal for non-revenue generating entities absorbing legal and administrative expenses without income inflows [F1]. The secure segregation of IPO proceeds in trust accounts mitigates direct financial risk associated with operating liabilities.

Key Milestones to Monitor Post-IPO

Critical developments warrant attention going forward:

- Identification and public announcement of potential business combination targets,

- Filing proxy statements detailing transaction terms,

- Scheduling shareholder votes on proposed deals,

- Completion or termination deadlines pursuant to SEC-imposed timelines,

- Possible exercise of over-allotment options related to underwriting agreements,

- Updates on sponsor-unit lock-up expirations which could affect supply-demand balance in the security trading environment. Monitoring these will provide directional insight into the pace at which MCAH transitions from shell status towards becoming an operational enterprise capable of delivering fundamental value gains.

Financial Overview and Liquidity Assessment

Latest financial data reveal MCAH incurred a net loss of $43,470 during Q1 2026 reflecting typical outlays associated with SPAC pre-combination governance costs including legal fees, audit expenses, director compensation accruals, and administrative overheads—none unusual for companies solely established as acquisition vehicles [F1]. Liquidity measured via conventional metrics appears constrained absent trust account assets; nevertheless, the segregated cash backing IPO proceeds preserves core shareholder interests intact until deployment towards acquisitions occurs [S3].

This analysis focuses exclusively on Mountain Crest Acquisition 6 Corp’s declared facts as per its latest SEC filings up to June 1st, 2026. It does not speculate regarding target opportunities or future stock performance. Readers should consider that Mountain Crest Acquisition 6 Corp’s value depends largely on successfully navigating highly competitive SPAC conditions amidst ongoing market scrutiny.

Financial position in context

Current assets of $30000 and current liabilities of $135420 imply a current ratio near 0.22x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments