Monroe Federal Bancorp: Community Banking Firm with Regional Mortgage Focus in Ohio

A newly established savings and loan holding company centered on residential mortgage lending in Miami and Montgomery Counties, Ohio.

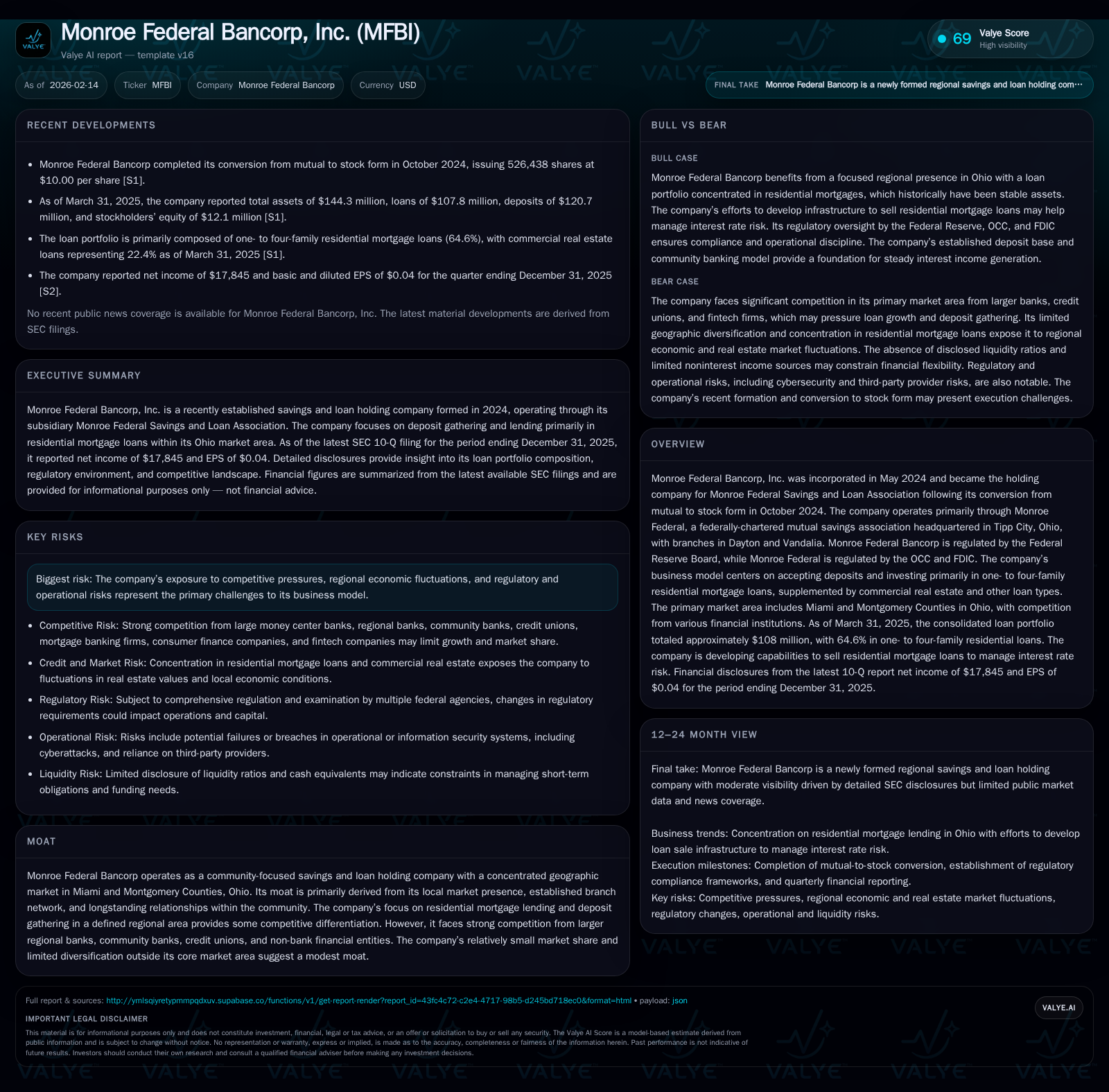

Monroe Federal Bancorp, Inc. was created in mid-2024 as the holding company for Monroe Federal Savings and Loan Association following its mutual-to-stock conversion. Its operations are geographically concentrated in southwestern Ohio, primarily serving Miami and Montgomery Counties, with a lending focus on one- to four-family residential mortgages supplemented by commercial real estate loans. The firm faces intense competition from larger banks, local community banks, credit unions, and non-bank lenders within its markets. Regulatory oversight by the Federal Reserve Board (holding company) and OCC/FDIC (savings bank) adds layers of compliance demands, while deposit gathering remains central to funding its loan portfolio. Its modest market share and narrow regional footprint imply a limited competitive moat despite strong community ties.

Introduction

Monroe Federal Bancorp, Inc. represents a distinct example of a modern community-oriented savings and loan holding company rooted deeply in southwestern Ohio. Incorporated in May 2024, its establishment coincided directly with the transition of Monroe Federal Savings and Loan Association from a mutual to a stock form institution by late October that year [S1]. This structural shift enabled capital raising through equity issuance while preserving its core mission: serving local customers through retail deposit gathering and focused residential mortgage lending.

Business Overview

Operating primarily via Monroe Federal S&L, the organization maintains its headquarters in Tipp City alongside branches in Dayton and Vandalia—cities situated within Miami and Montgomery Counties —near Dayton. This geography defines the company’s primary market area where it mobilizes deposits to fund a conservative loan portfolio comprised largely of one- to four-family residential mortgage loans complemented by commercial real estate exposures [S1]. The bank holds federal charters regulated by the Office of the Comptroller of the Currency (OCC) alongside Federal Deposit Insurance Corporation (FDIC) oversight for deposit insurance. At the holding company level, regulatory supervision falls under the Federal Reserve Board.

Market Position & Competitive Landscape

The banking environment in Miami and Montgomery Counties is crowded with various financial institutions—larger regional banks providing scale advantages; other community banks offering local familiarity; credit unions appealing through nonprofit member benefits; plus non-bank lenders innovating digitally [analysis]. Monroe Federal Bancorp’s niche lies squarely within this densely contested segment. Its competitive edge is grounded substantially on localized customer relationships formed over years via brick-and-mortar presence coupled with personalized service—a focal point for many community institutions striving to preserve relevance amid industry consolidation trends.

Nevertheless, its modest market share constrains pricing power and operational leverage. Lack of diverse geographic exposure could amplify risk during localized economic downturns that impact real estate demand and property valuations.

Financial Highlights & Operational Metrics

Recent filings report net income of $17,845 as of year-end December 31, 2025 (unaudited figure extrapolated from latest data) illustrating the early-stage profitability post-conversion while reflecting scale limitations relative to peers [F1]. Although detailed balance sheet composition is partially redacted or truncated in available documents, strategic emphasis remains clear on maintaining prudent underwriting standards within residential mortgages to protect asset quality.

Liquidity depends heavily on stable deposit inflows—a hallmark trait for mutual-founded banks transitioning into public companies—and consistent loan demand within core counties [S2]. Interest rate fluctuations represent an ongoing challenge affecting net interest margins due to their impact on loan origination volume and prepayment speeds.

Regulatory Environment & Risk Factors

Monroe Federal Bancorp operates under comprehensive regulatory scrutiny: banking regulations impose capital requirements, reserve levels, consumer protection statutes, and audit controls from multiple agencies [S1]. The company acknowledges significant risk exposures:

- Macroeconomic conditions influencing borrower creditworthiness,

- Real estate price volatility impacting collateral values,

- Technological changes necessitating ongoing investment in security infrastructure,

- Competitive encroachment potentially compressing margins,

- Regulatory rule updates altering cost structures or capital allocation,

- Operational risks including cyber threats or third-party vendor dependencies.

Retention of key employees amid industry talent shortages further shapes risk perspectives.

Strategic Outlook & Industry Context (Analysis)

Within the broader American banking industry framework circa mid-2020s, small-to-mid-sized community banks like Monroe Federal face stark choices—accelerate digital transformation or deepen community relationships—or attempt both simultaneously. Given its nascent public-company status following conversion less than two years ago, Monroe Federal Bancorp seems positioned toward measured growth rather than expansive branching or aggressive diversification [S1][S2].

The local real estate market dynamics within Miami-Montgomery Counties will continue playing a pivotal role; affordability constraints or demographic shifts could alter home loan demand materially. Regulatory environments remain dynamic post-financial crisis reforms but may ease gradually to support smaller institutions’ viability.

Finally, fintech entrants increasingly compete for mortgage origination market share via streamlined online platforms—a challenge to traditional underwriting models requiring adaptation over time [analysis].

Conclusion

Monroe Federal Bancorp serves as a quintessential emerging community bank holding company focusing on a defined regional footprint with concentrated lending strategy anchored by residential mortgages. Its strengths lie in established physical presence within local markets and historical ties valued by customers preferring relationship banking. However, scale limitations combined with intense competitive pressures necessitate continual vigilance on operational efficiency and risk management facets.

As the company matures beyond its early conversion phase into stock form ownership structure, balancing growth ambitions against economic cyclicality inherent within residential real estate financing will be crucial. Investors monitoring this institution should consider the interplay of localized market conditions alongside evolving regulatory landscapes shaping small bank prospects.

This analysis is intended solely for informational purposes based on publicly available data as of early 2026 without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments