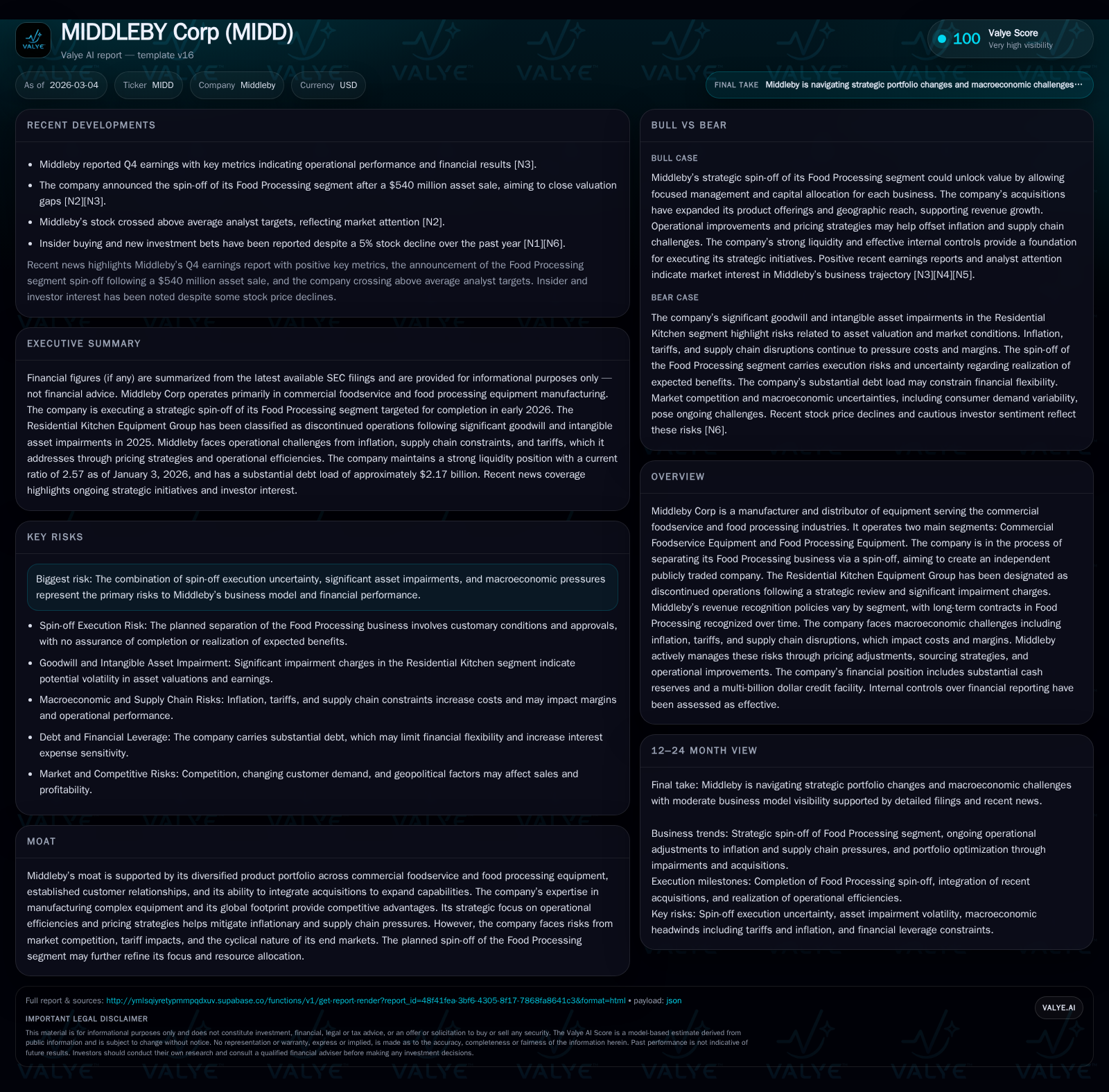

Middleby Corp’s Strategic Spin-Off and Its Impact on Growth Trajectory

Middleby’s planned Food Processing segment spin-off coincides with strong revenue growth but steep net income contraction, reshaping its operational and financial outlook.

Middleby Corp experienced robust revenue growth of 19.6% in FY2025, driven primarily by its Commercial Foodservice segment and resilient long-term contract execution in Food Processing. However, this came with a dramatic net income decline of 91.4%, heavily impacted by significant impairment charges related to its discontinued Residential Kitchen Equipment operations. The company is proceeding with a spin-off of its Food Processing segment, aiming to concentrate resources and strategic focus on Commercial Foodservice Equipment. Capital structure adjustments ahead of the spin-off include amended credit facilities and substantial debt repayments, while capital allocation has notably skewed toward aggressive share repurchases despite subdued ROE near 1.3%. Key metrics to monitor post-spin include segment-specific revenue contribution, margin sustainability amid inflationary pressures, and contract backlog developments.

Historical Revenue and Profit Dynamics: Growth Drivers and Shifts

Middleby Corp’s fiscal year ended January 3, 2026 (FY2025) marked a pivotal inflection point characterized by a duality of robust top-line expansion against severe bottom-line contraction [F1]. Revenue increased by an impressive 19.6% year-over-year to approximately $3.2 billion, fueled specifically by strength in the Commercial Foodservice Equipment segment which accounted for roughly $2.35 billion in sales vs. $850 million from the Food Processing Equipment segment [S5][S16]. This broader portfolio diversification afforded relative resilience across geographic regions including the U.S., Europe, Asia, and Latin America.

Contrasting the revenue momentum was a daunting -91.4% plunge in net income down to just over $36.9 million for FY2025 [F1]. The principal driver was a non-cash impairment charge exceeding $700 million tied predominantly to the Residential Kitchen Equipment Group’s goodwill and trademark assets following a strategic review that designated this group as discontinued operations [S19]. Despite this shock to net results, operating income remained relatively resilient albeit down 12.4% YoY at around $574 million [F1], underscoring underlying operational strength outside impairment distortions.

Operating cash flow sustained a stable trajectory generating $630 million in FY2025 [F1], supporting capex investments which rose substantially by +43% YoY to $70.7 million as Middleby reinforced facility upgrades and innovation efforts [F1][S21]. In essence, Middleby’s historical performance reveals growth propelled by broad-based product demand tempered by strategic restructuring costs that materially curtailed earnings.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 37 | 630 | 575 | 71 | -91.4% |

| 2024 | 428 | 687 | 656 | 49 | +6.9% |

| 2023 | 401 | 629 | 635 | 85 | -8.2% |

| 2022 | 437 | 333 | 640 | 67 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 724 | 559 | 1.3 |

| 2024 | 35 | 638 | 11.8 |

| 2023 | 75 | 544 | 12.3 |

| 2022 | 265 | 265 | 15.6 |

Source: SEC companyfacts cache [F1].

Unpacking the Spin-Off: Strategic Rationale and Execution Risks

In February 2025, Middleby publicly declared its intent to spin off its Food Processing business into an independent public entity distributed tax-free to existing shareholders [N9][S2]. The rationale centers on sharpening each business unit's strategic focus: enabling Commercial Foodservice Equipment to intensify market penetration while allowing the Food Processing division—characterized largely by long-term contracts—to pursue tailored growth trajectories unencumbered by integration complexities.

This separation is expected in the first half of calendar year 2026 pending customary SEC approvals and final Board consents [S2][S3]. Though structured for tax efficiency under U.S. federal law, execution risk looms large given dependencies on regulatory clearance, capital market receptivity amidst macroeconomic uncertainty, and operational disentanglement challenges [S10].

Management has appointed leadership for the new standalone Food Processing company ahead of the transaction closings signifying progress but reinforcing that any delay or transaction modification could adversely impact shareholder value or operational stability [S3]. Hence, stakeholders should actively track filings and announcements related to this material corporate reorganizational event.

Supply Chain Pressures and Inflation: Operating Margin Implications

Middleby's equipment fabrication inherently depends on complex assemblies and sourced components exposed acutely to global inflationary forces—ranging from wage inflation through surge pricing on raw materials like steel and electronic parts—as well as tariff-imposed cost escalations linked to ongoing geopolitical frictions [S1][S2][N1].

To counterbalance these pressures, Middleby leverages contract structures often embedding variable consideration such as volume rebates within its Commercial Foodservice portfolio while recognizing revenues over time for sizable Food Processing projects based on performance obligations' satisfaction [S5][S26]. The company actively implements pricing adjustments consistent with cost pass-through concepts complemented by efforts in dual sourcing and operational improvements aimed at keeping gross margins from eroding materially [N1][S18]. Despite improvements in supply chain availability noted during late FY2025 periods, continued vigilance remains necessary given residual uncertainties around logistics bottlenecks [S18].

Forecasting Post-Spin Revenue Streams and Growth Barriers

Upon spin-off completion, Middleby's standalone Commercial Foodservice Equipment segment will represent the majority of remaining revenues projected at around $2.35 billion for FY2025 equivalence absent structural shifts [S16][N9]. This segment's reliance on point-in-time revenue recognition combined with aftermarket parts sales suggests more volatile quarter-to-quarter top-line rhythm compared with steady state production-oriented contracts inherent in Food Processing.

Analyst consensus anticipates subdued but positive growth prospects conditioned on easing inflationary headwinds and expansion into emerging markets underpinning moderate demand recovery post-interest rate stabilization [N5][N1]. However, external risks—particularly competition intensification and tariff retaliation risks affecting exported equipment sales—may cap upside potential or delay new order bookings [N9][S10]. Advanced metrics such as monitoring contract backlog composition alongside variable consideration estimates will provide forward-looking insight into sustainable margin trends during this transformative phase.

Capital Structure and Liquidity: Managing Debt Post-Separation

As of January 3, 2026, Middleby carried total borrowings of approximately $2.17 billion comprised mainly of term loan facilities under an amended Credit Facility designed with provisions facilitating the planned spin-off transaction [S4]. This facility enforces stringent financial covenants including a secured leverage ratio capped at 3.75x EBITDA (adjustable temporarily upward post-qualified acquisitions), alongside minimum interest coverage ratio requirements of at least 3x EBITDA coverage—conditions Middleby confirms compliance with at period end [S4].

Interest rate exposure stemming from floating-rate debt is mitigated via cash flow hedges consisting of interest rate swaps transitioning reference rates from one-month LIBOR to SOFR without material accounting impacts noted [S1][S23]. Foreign currency forward contracts further protect against FX volatility given international revenue streams primarily denominated in multiple currencies.

Liquidity stands robust with $1.7 billion borrowing capacity remaining available under revolving facilities alongside cash equivalents totaling roughly $222 million—the balance positioning Middleby favorably entering spin-off-related financial realignments [F1][S8]. However, pro forma balance sheet effects following asset divestiture inherent to structuring warrant monitoring concerning covenant headroom dynamics.

Capital Allocation Priorities: Buybacks, Dividends, and Investment Plans

The company's capital deployment strategy took a markedly aggressive turn during FY2025 when share repurchases ballooned dramatically to over $723 million from about $35 million spent in FY2024—a reflection possibly indicating management’s confidence in equity valuation or desire for EPS accretion absent alternative uses amidst earnings pressure [F1][S12][S13]. Dividends have not been prominently disclosed as significant returns relative to buybacks suggesting emphasis lies on stock repurchases presently.

Simultaneously capex outlays expanded materially (+43%) indicative of investments underpinning manufacturing capability enhancements potentially aligned with streamlining operations ahead of segmentation refocus downstream from spin-off completion [F1][S21]. Although reported ROE tumbled sharply resulting near an estimated lowly ~1.3%, operational free cash flow remained solid at approximately $559 million (CFO minus capex), thus sustaining flexibility for future investment or shareholder returns if executed prudently within capital structure constraints.

Key Performance Metrics to Monitor in the Transition Phase

Investors and analysts should closely track several vital KPIs during this transitional epoch:

- Revenue concentration shift exclusively toward Commercial Foodservice post-spin reflected also through margin analysis allowing discernment between segments' intrinsic profitability drivers;

- Contract liabilities/assets evolution particularly concerning long-term contract margins given their complex recognition timetables impacting quarterly earnings visibility;

- Adjusted EBITDA trends per reporting segment as measure removing nonrecurring impairment distortions enhancing comparability;

- Inventory levels and working capital changes reflecting supply chain health amid ongoing logistical challenges;

- Pricing strategy effectiveness vis-à-vis inflation pass-through capability assessed via gross margin progression;

- Updates regarding spin-off milestones including regulatory clearances or Board decisions influencing timelines or strategic outcomes;

- Currency hedging efficacy considering multinational exposure mitigating foreign exchange risk impacting net income volatility.

This comprehensive set provides actionable insight into operational execution fidelity as Middleby navigates this substantive corporate restructuring while contending with macroeconomic headwinds.

This analysis synthesizes verified regulatory filings along with contemporary market reporting without speculative forecasts beyond documented company guidance or disclosures. It offers an informed perspective grounded in observed historical results contextualized amid unfolding strategic repositioning.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments