Altria Group’s Q1 2026 Results Spotlight Stable Cash Flow Amid Regulatory Headwinds

Altria’s latest quarter reveals steady earnings and robust dividend capacity as it navigates entrenched regulatory and liquidity challenges.

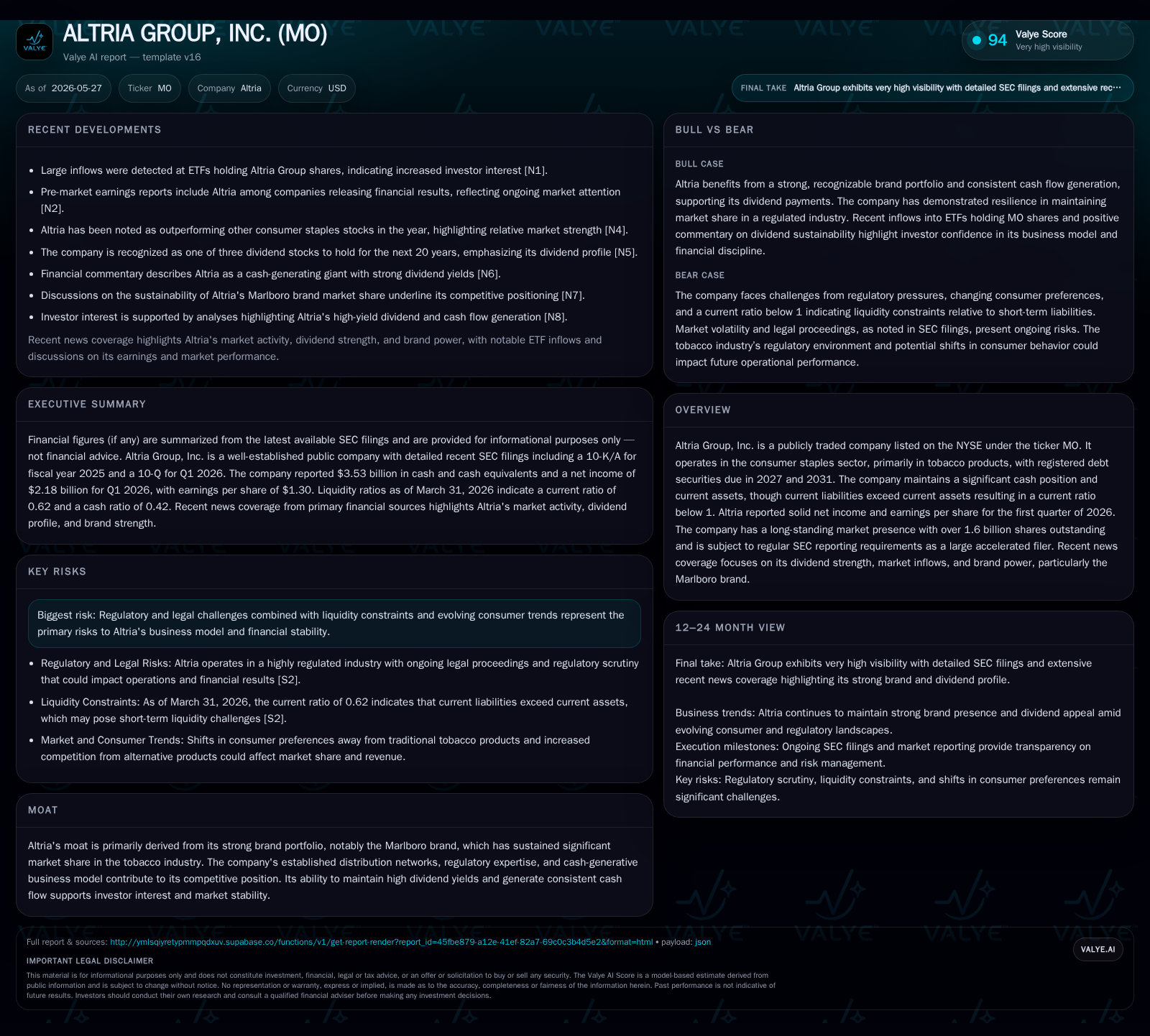

Altria Group reported a stable financial performance in Q1 2026, maintaining solid net income and earnings per share despite ongoing regulatory pressures. The company’s business model centers on its dominant tobacco portfolio led by Marlboro, leveraging pricing power and entrenched distribution networks. While competitive within the consumer staples sector due to its brand moat and dividend appeal, Altria faces growth constraints from regulatory uncertainties and liquidity limitations. Strategic focus on innovation and operational efficiencies underpins its growth outlook, but watch for regulatory developments and capital allocation updates. The balance sheet reflects strong cash reserves yet a current ratio below one, underscoring careful liquidity management amid substantial leverage.

Examining Altria’s Latest Quarterly Operating Update

In its latest Form 10-Q filing dated April 30, 2026, Altria Group reported consistent operational performance through the first quarter of 2026. The company sustained solid net income and earnings per share figures, affirming the resilience of its core tobacco business during ongoing industry headwinds [S2][N1]. Notably, the filing confirms there have been no material changes to previously outlined risk factors, indicating stability in Altria's regulatory and legal exposures for now [S2]. Legal proceedings remain disclosed but do not appear to have escalated materially this quarter, supporting a steady operating environment.

The absence of risk factor amendments suggests that the regulatory landscape remains a predictable variable for investors in the short term; however, ongoing legal risks continue as an inherent business challenge given tobacco industry dynamics.

Business Model Analysis: Revenue Drivers and Brand Strength

Altria’s revenue mechanics revolve around the sale of combustible cigarettes and smokeless tobacco products dominated by its flagship Marlboro brand — a near-ubiquitous leader with durable pricing power owing to strong brand loyalty and limited consumer switching [S1][F1]. Consumers pay premium prices for Marlboro due to perceived quality and taste preferences reinforced by longstanding marketing efforts.

Pricing strategies are supported by relatively inelastic demand characteristic of tobacco consumption patterns where addiction creates high switching costs. Volume trends remain mixed as public health pressures gradually depress cigarette unit sales over time.

The company’s comprehensive distribution network ensures deep retail penetration, allowing effective price realization even as tax-driven cost pressures elevate retail prices. Product mix improvements focus on growth in reduced-risk products (RRPs) which command differentiated positioning under increasing regulation.

Overall, Altria monetizes both unit volume sales and pricing power with margins benefiting from fixed-cost leverage inherent in manufacturing infrastructure.

Competitive Position within the Tobacco and Consumer Staples Sector

Within the tobacco landscape — characterized by significant regulation and high entry barriers — Altria holds a formidable competitive position largely attributable to Marlboro’s dominant market share and trusted consumer franchise [S1][N2]. Its expertise navigating complex federal and state regulations differentiates it from newer entrants or international competitors less versed in U.S. compliance nuances.

Furthermore, recent ETF inflows highlight investor appetite for Altria’s stable dividend yield profile compared to other consumer staples peers facing more cyclical volatility [N2][N9]. This positions Altria as a preferred income-generating asset amidst market uncertainty.

By contrast with peers that may lack scale or are more exposed to rapidly evolving product categories (like vaping), Altria's broad portfolio breadth combined with conservative capital management reinforces resilience against sector headwinds.

Key Growth Drivers and Strategic Initiatives

Growth initiatives revealed in recent filings point towards expansion in reduced-risk product categories and incremental margin improvement through operational efficiencies [S3][N6]. These RRPs include next-generation nicotine delivery systems tailored to shifting consumer preferences toward lower-harm alternatives.

Geographic expansion is limited given the domestic focus mandated by regulatory frameworks; thus growth relies heavily on innovation adoption rates and market penetration within existing channels.

Management commentary emphasizes disciplined margin control alongside cautious portfolio repositioning to mitigate declining combustible volumes while capitalizing on healthier product segments [S1][S3]. Maintaining robust cash flow supports reinvestment strategies without jeopardizing shareholder returns.

Key performance indicators tied to growth include RRP unit volumes, pricing mix shifts, and operating expense ratios — all closely watched in quarterly disclosures going forward.

Risks and Challenges Impacting Future Performance

Altria continues to confront entrenched regulatory pressures including potential incremental taxes, advertising restrictions, flavor bans, and litigation exposure documented extensively in its SEC filings [S2][S5]. These factors exert structural constraints that limit volume growth prospects while elevating cost structures.

A salient watchpoint is liquidity management: with current assets at approximately $5.2 billion juxtaposed against current liabilities at $8.4 billion as of March 31, 2026, Altria’s current ratio stands at a modest 0.62 indicating near-term liquidity pressure [F1]. This situation demands ongoing prudence in working capital deployment.

Evolving consumer behaviors away from combustible tobacco products towards cessation or alternative nicotine forms threaten volume trajectories despite offsetting premium pricing strategies. Macroeconomic uncertainties further complicate demand visibility.

Taken together, these risk vectors underscore the importance of vigilant regulatory monitoring alongside strategic capital allocation balancing growth investments against prudent leverage control.

Near-Term Catalysts and What to Watch Next

Investors should track upcoming quarterly earnings releases for updates on RRP adoption rates and margin trends as key operational barometers post-Q1 [S3][N8]. Regulatory announcements concerning flavored product approvals or restrictions could materially influence revenue pacing given their disproportionate impact on younger demographics.

Capital allocation decisions — dividends versus share repurchases — remain relevant signals regarding management’s confidence in sustainable cash flow generation [N10]. Further clarity around litigation developments or settlements will also bear on risk assessments.

The trajectory of policy changes at both federal and state levels merits attention due to potential immediate impacts on excise taxes or marketing capabilities affecting top-line performance.

Brief Financial Profile: Liquidity, Debt, and Cash Flow

At March 31, 2026, Altria held approximately $3.5 billion in cash and equivalents with total debt outstanding near $25.9 billion recorded at fiscal year-end 2025 resulting in net debt of about $22.4 billion after factoring available cash reserves [F1]. Current assets totaled around $5.2 billion against current liabilities approximating $8.4 billion yielding a current ratio of roughly 0.62 reflecting tight short-term liquidity conditions requiring managed working capital turnover [F1].

Net income generation remains solid supporting continued dividend payouts which remain appealing given the company’s stable cash flow profile despite higher leverage levels constraining financial flexibility somewhat [S2]. Ongoing operational cash flow conversion underpins funding capacity for strategic initiatives while servicing debt maturities scheduled over the medium term.

This balance sheet snapshot communicates moderate leverage balanced by strong brand-driven cash flows albeit mandating disciplined liquidity management under evolving market conditions.

Financial position in context

As of 2026-03-31, companyfacts shows $3.5bn in cash and equivalents and $25.9bn of total debt [F1]. The same snapshot implies net debt of roughly $22.4bn, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $5.2bn and current liabilities of $8.4bn imply a current ratio near 0.62x for 2026-03-31 [F1].

Disclaimer: This analysis is for informational purposes only based on publicly available documents as of May 27, 2026. It does not constitute investment advice or research views regarding Altria Group or any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments