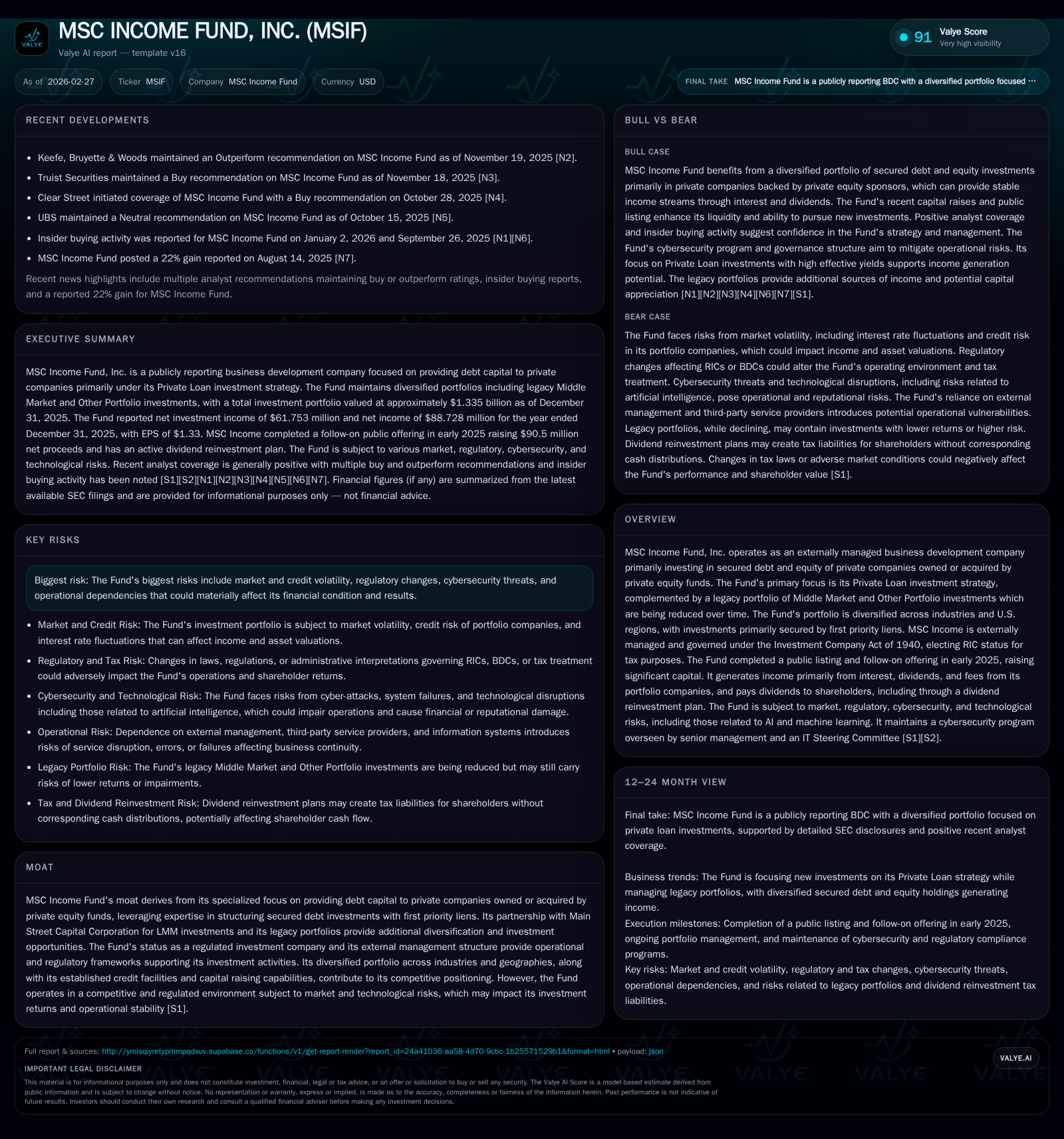

MSC Income Fund's Strategic Focus on Private Loans Supports Portfolio and Capital Evolution in 2025

Following its 2025 public listing, MSC Income Fund, Inc. (MSIF) concentrated on Private Loan investments, reshaping its portfolio and capital structure while delivering strong net income growth amid typical BDC risks.

MSC Income Fund, Inc. prioritized Private Loan investments after its 2025 listing, reducing legacy Middle Market and Other portfolios. The fund expanded equity capital through a $90.5 million net follow-on offering and maintained a diversified portfolio with a majority in first lien secured debt. Total borrowings increased moderately with refinanced credit facilities lowering borrowing costs to an average of 6.1%. MSIF reported a 57% net income increase to $88.7 million in 2025 despite negative operating cash flow driven by investment activity. Dividends rose to $67.6 million while share repurchases declined due to suspension of prior programs. The fund continues managing interest rate sensitivity, credit risk, and regulatory factors inherent in BDC operations.

Company Overview

MSC Income Fund, Inc. (MSIF) is an externally managed business development company investing primarily in secured debt and equity interests of private companies sponsored by private equity funds. Its principal focus is on Private Loan investments secured by first priority liens on portfolio company assets across diverse industries and U.S. regions [S1]. Legacy Middle Market and Other Portfolio holdings are being actively reduced as MSIF concentrates new platform investments exclusively on Private Loans following its public listing in early 2025 [S22], [S23]. The Fund elects Regulated Investment Company (RIC) status for favorable U.S. federal tax treatment [S1].

Historical Performance and Growth Drivers

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 89 | -70 | +56.9% |

| 2024 | 57 | -28 | -14.6% |

| 2023 | 66 | 50 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 68 | 12 | 12.0 |

| 2024 | 58 | 21 | 9.0 |

| 2023 | 56 | 24 | 10.6 |

Source: SEC companyfacts cache [F1].

Net income rebounded strongly in FY2025, increasing nearly 57% year-over-year largely driven by higher interest income aligned with the expanded capital base post-follow-on offering which generated net proceeds of approximately $90.5 million [F1], [S14]. Operating cash flow was negative $70.3 million reflecting active investment deployment exceeding asset monetizations typical for growing BDCs [F1]. Equity grew significantly due to the equity issuance combined with retained earnings from improved profitability [F1]. Dividends paid increased alongside earnings while share repurchases declined following suspension of prior repurchase programs before the listing event [S8], [S11].

Portfolio Composition Shift

Post-IPO, MSC Income adopted a strategy focusing all new platform investments on Private Loans while allowing legacy Middle Market and Other Portfolio investments to run off through repayments or sales [S22], [S23]. As of December 31, 2025:

- Approximately 81 Private Loan portfolio companies held at fair value near $809 million.

- Lower Middle Market (LMM) portfolio comprised about 55 companies valued around $488 million but shrinking given cessation of new LMM deployments.

- Nearly all debt investments (>99%) within these segments are secured by first lien positions.

- Geographic diversification spans the U.S., led by West (

22%), Midwest (21%), Southwest (19%), Southeast (18%), Northeast (~15%), with smaller Canadian and other non-U.S exposures [S15], [S18], [S19]. - Industry exposure is broad including electrical equipment, commercial services, machinery, professional services, construction & engineering among others supporting risk diversification [S15].

Reported weighted average yields for end-2025 approximate ~10.7% for Private Loan debt and ~12.4% for LMM debt portfolios with contractual floors on floating rate loans mitigating downside interest rate risk [S19].

Capital Structure and Liquidity

At December 31, 2025, total outstanding debt was approximately $603 million consisting of:

- Corporate Facility commitments increased from $165 million pre-2025 to $245 million post-amendment with an accordion capacity up to $300 million; maturity extended through November 2028 with extension options subject to lender approval [S4], [S6].

- SPV Facility commitments remained at $300 million with accordion capacity up to $450 million; revolving period extended through February 2029 with final maturity February 2030 [S5], [S6].

- Fixed-rate Series A Senior Notes totaling $150 million at a coupon of 4.04%, maturing October 30, 2026 [S6], [S7].

Weighted-average borrowing costs declined materially from approximately 7.5% in FY2024 to about 6.1% in FY2025 reflecting refinancing efforts that lowered interest expense despite incremental borrowings ([F1],[S9]). Total interest expense fell from roughly $39 million in FY24 to ~$33.9 million in FY25 consistent with these trends.

The Fund remained compliant with all financial covenants under its credit facilities throughout the period without any breaches or forbearance noted demonstrating strong financial discipline consistent with regulatory oversight for BDCs [S4], [S12].

Dividend Policy and Share Repurchase Activity

MSIF pays dividends primarily supported by net investment income distributions consistent with RIC tax requirements.

Effective March 6, 2025, coinciding with the MSC Income Listing, the dividend reinvestment plan transitioned from an opt-in to an opt-out structure enhancing shareholder flexibility while conserving capital for investment opportunities [S8], [S17].

Dividends paid increased to $67.6 million in FY25 compared to $58.2 million in FY24 reflecting improved earnings power; however, share repurchases declined sharply to $11.6 million following suspension of prior quarterly repurchase programs before listing completion [S8], [S13]. A new open market repurchase plan capped at $65 million across twelve months beginning March ’25 was established alongside Main Street Capital Corporation’s parallel plan intended to support NAV per share stability when market prices trade below NAV levels [S8], [S20].

Risk Considerations

MSIF faces risks typical of externally managed BDCs including:

- Interest rate sensitivity impacting borrowing costs versus asset yields given a majority floating-rate loan portfolio (~78%) partially mitigated by contractual floors limiting downside exposure [S1].

- Credit quality volatility inherent in lending primarily to middle-market private companies potentially affecting income sustainability.

- Regulatory changes governing BDC operations or tax laws that could affect distribution levels or corporate structure.

- Cybersecurity risks related to operational dependencies that may disrupt financial reporting or client relations.

No material default or impairment trends were reported as of December ’25 indicating prudent underwriting standards generally maintained [S1].

Forward-Looking Considerations

Though explicit forward guidance is not provided in current filings, key factors influencing future performance include:

- Ability to source accretive Private Loan assets within disciplined risk parameters amid evolving credit markets.

- Management of legacy portfolio runoff balancing timing of realizations against market valuations.

- Interest rate movements relative to SOFR/Prime affecting net interest margins particularly given absence of hedging programs currently employed.

- Efficient capital recycling deploying proceeds from repayments into new investments sustaining dividend streams.

- Impact of potential regulatory or tax code changes affecting RIC status or BDC governance structures.

Conclusion

MSC Income Fund has strategically refocused on secured Private Loan financing supported by a strengthened equity base following its public offering and refinanced credit facilities resulting in lower funding costs during fiscal year ended December ’25 ([F1],[S4]). The fund realized strong net income improvement reflecting these initiatives offset by operating cash flow pressures typical for investment companies scaling deployments ([F1]). Dividend increases have been executed prudently within regulatory frameworks balancing shareholder returns against financial flexibility ([S8]). Investors should monitor credit cycle developments impacting collateralized loan portfolios alongside shifts in interest rates influencing cost of capital dynamics given the floating-rate asset profile constrained by floors ([S1]). Additionally, MSIF’s partnerships including co-investments with Main Street Capital add structural complexity influencing execution and returns.

This report summarizes publicly available data as of early 2026 based on SEC filings and company disclosures without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments