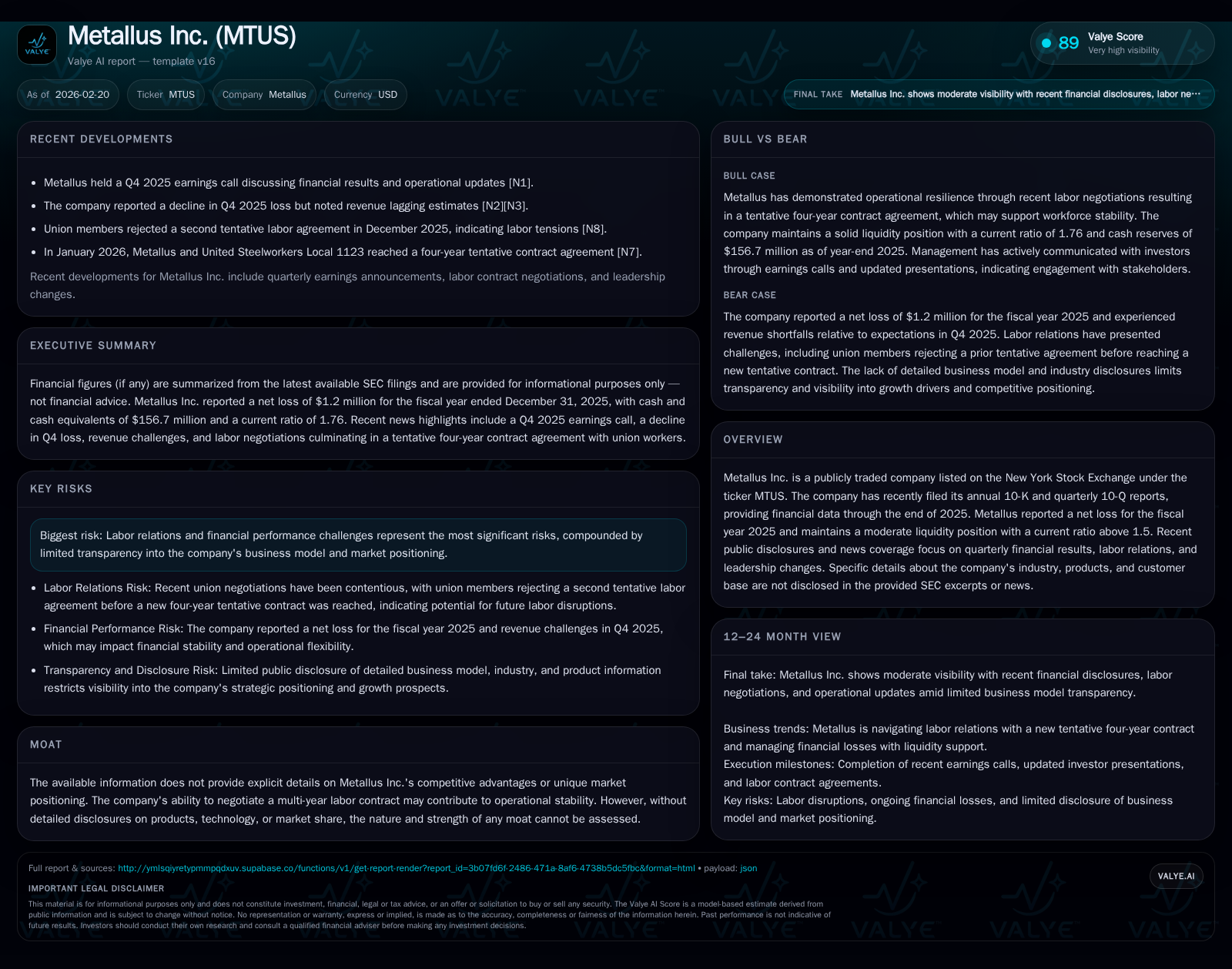

Metallus Inc. Faces Profitability and Transparency Challenges despite Labor Agreement Stability

Metallus Inc. reported a net loss in 2025, grappling with operational headwinds and opaque business disclosures.

Metallus Inc., a publicly traded company on the NYSE, closed fiscal year 2025 with a modest net loss following years of mixed profitability. While liquidity remains adequate with a current ratio above 1.5, limited transparency into its operations and market positioning clouds future outlooks. A newly negotiated four-year labor contract with unionized employees provides some operational stability, but ongoing challenges with financial performance and unclear growth drivers persist.

Company Overview and Historical Performance

Metallus Inc. (NYSE: MTUS) remains an opaque entity from a business model perspective owing to scarce disclosures about its industry verticals, product offerings, or key customers. The company’s latest filings give a picture primarily defined by sporadic financial performance and recent labor developments rather than market-facing details [S1], [S8].

From a pure financial vantage point, Metallus has experienced significant volatility over the last half decade. Operating income swung from substantial losses exceeding $100 million in 2015-2016 to positive territory by 2018 before resuming losses in subsequent periods [F1]. Net income tells a similar story — profitability seen as recently as FY2023 ($69.4 million) collapsed into a $1.2 million loss in FY2025 [F1]. This deterioration signals operational challenges or margin compression that have yet to be fully disclosed.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | 16 | 16 | -192.3% |

| 2024 | 1 | 40 | 18 | -98.1% |

| 2023 | 69 | 125 | 12 | +6.6% |

| 2022 | 65 | 135 | 11 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 13 | 0 | -0.2 |

| 2024 | 38 | 23 | 0.2 |

| 2023 | 33 | 113 | 9.5 |

| 2022 | 52 | 124 | 9.5 |

Source: SEC companyfacts cache [F1].

*Calculated versus FY2017 operating income which was negative $23.4 million; exact recent operating incomes not fully provided [F1].

Note: Revenue data is not available in the provided XBRL tags; hence YoY revenue trends cannot be analyzed.

Operating cash flow (CFO) has shown steep declines from peaks above $125 million to $16 million in FY2025 while capital expenditure outlays have remained moderate around $16 million annually [F1]. This declining cash conversion ratio may point toward deteriorating working capital management or increased costs.

Liquidity and Capital Structure

As of December 31, 2025, Metallus held cash and cash equivalents of approximately $156.7 million against current liabilities totaling nearly $315 million, yielding a robust current ratio of roughly 1.76 [F1]. This implies satisfactory short-term financial health.

Despite recurrent operating losses recently, the company's equity remained substantial at $686 million as of FY2025 end [F1]. However, returns on this equity base are minimal or negative; using net income over stockholders’ equity yields an approximate ROE of around -0.2% for FY2025 [F1], signaling negligible shareholder profitability.

The company continues moderate share repurchase activity albeit less aggressively than earlier periods; buybacks dropped from levels above $50 million in FY2022 down to just over $13 million in FY2025 [F1]. No dividends were indicated in recent filings suggesting Metallus prioritizes liquidity conservation or restructuring over direct shareholder payouts.

Labor Relations and Operational Stability

A significant development for Metallus' operational landscape occurred early in 2026 when it secured a four-year tentative labor contract with United Steelworkers Local 1123 [N7]. This agreement likely mitigates risks linked to workforce disruptions and provides cost visibility within negotiated labor expenses.

However, without transparency regarding the company's production scale or customer concentration, it is difficult to assess how labor cost changes might impact margins structurally.

Strategic Positioning and Moat Considerations

The lack of explicit information concerning Metallus’s markets or competitive advantages inhibits proper assessment of its economic moat or durability against competitors . The company offers no product or segment breakdown nor any technology leadership claims across regulatory filings or news disclosures [S8], [S4].

While securing multi-year labor stability is beneficial for internal consistency, this factor alone falls short of constituting a defensible market edge given broader unknowns about revenues or innovation strategies.

Future Growth Prospects and Risks

No concrete guidance has been provided regarding upcoming business growth initiatives or revenue targets at the time of the latest reports [N1], [N2], making forecasting speculative. Investors and analysts should track quarterly earnings releases closely for early signs of turnaround efforts or emerging opportunities.

Key risks center on ongoing financial performance volatility compounded by the opacity surrounding corporate strategy and market positioning [S4]. Potential impacts from raw material prices, external demand cycles, technological shifts, or regulatory challenges remain unidentified due to limited disclosure frameworks.

Management Changes and Executive Incentives

In mid-2025, Metallus appointed Kristopher R. Westbrooks as President and COO alongside John M. Zaranec III as Executive VP and CFO, signaling leadership refreshes aimed perhaps at strategic reset or governance strengthening [S20], [S26]. Compensation packages include performance-based components aligning executive incentives with company results moving forward.

Analysis Summary and Key Metrics to Watch

- Profitability: After several profitable years marked notably by strong net income through FY2023-24, Metallus slipped back into losses by FY2025; scanning for margin progression will be critical.

- Liquidity: Ample cash resources soothe concerns about working capital but do not fully offset persistent weak earnings returns.

- Operational Stability: Labor agreement extends cost certainty but underlying production efficiencies are unquantified.

- Disclosure Gaps: Absence of industry/segment commentary restricts understanding of competitive challenges or growth drivers.

- Capital Allocation: Reduced share repurchases point toward cautious use of cash amid uncertain financial prospects.

- Leadership: New executive appointments reflect potential strategic refocus but outcomes remain pending.

Metrics Table Summary (FY2018 – FY2025)

| Metric | Latest Value (FY2025) |

|---|---|

| Net Income | -$1.2M |

| Operating CF | +$16M |

| Capex | $16M |

| Equity | $686M |

| Buybacks | $13M |

| Current Ratio | ~1.76 |

| ROE (approx) | -0.2% |

Conclusion

Metallus Inc.’s recent public financial data underscores notable challenges returning the company back to consistent profitability after prior gains through early-to-mid-2020s periods characterized by large swings in operating income and net results [F1]. The firm’s liquidity posture remains stable enough to support ongoing operations amidst these fluctuations while labor relations benefit from newly inked multi-year contracts enhancing cost predictability [N7].

However, limited transparency on core business activities impairs thorough evaluation of competitive positioning or concrete growth potential—both critical for stakeholders assessing longer-term value creation capacity under current management's direction post its leadership reshuffles [S20], [S26]. Further analytic clarity will depend heavily on upcoming quarterly disclosures providing deeper insight into revenue trends, margin pressures, capital deployment rationale, and operational adjustments addressing these vulnerabilities.

Disclaimer: This report is based solely on publicly available information up to February 20, 2026, including SEC filings and public news articles referenced; it does not constitute investment advice or an endorsement for any securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments