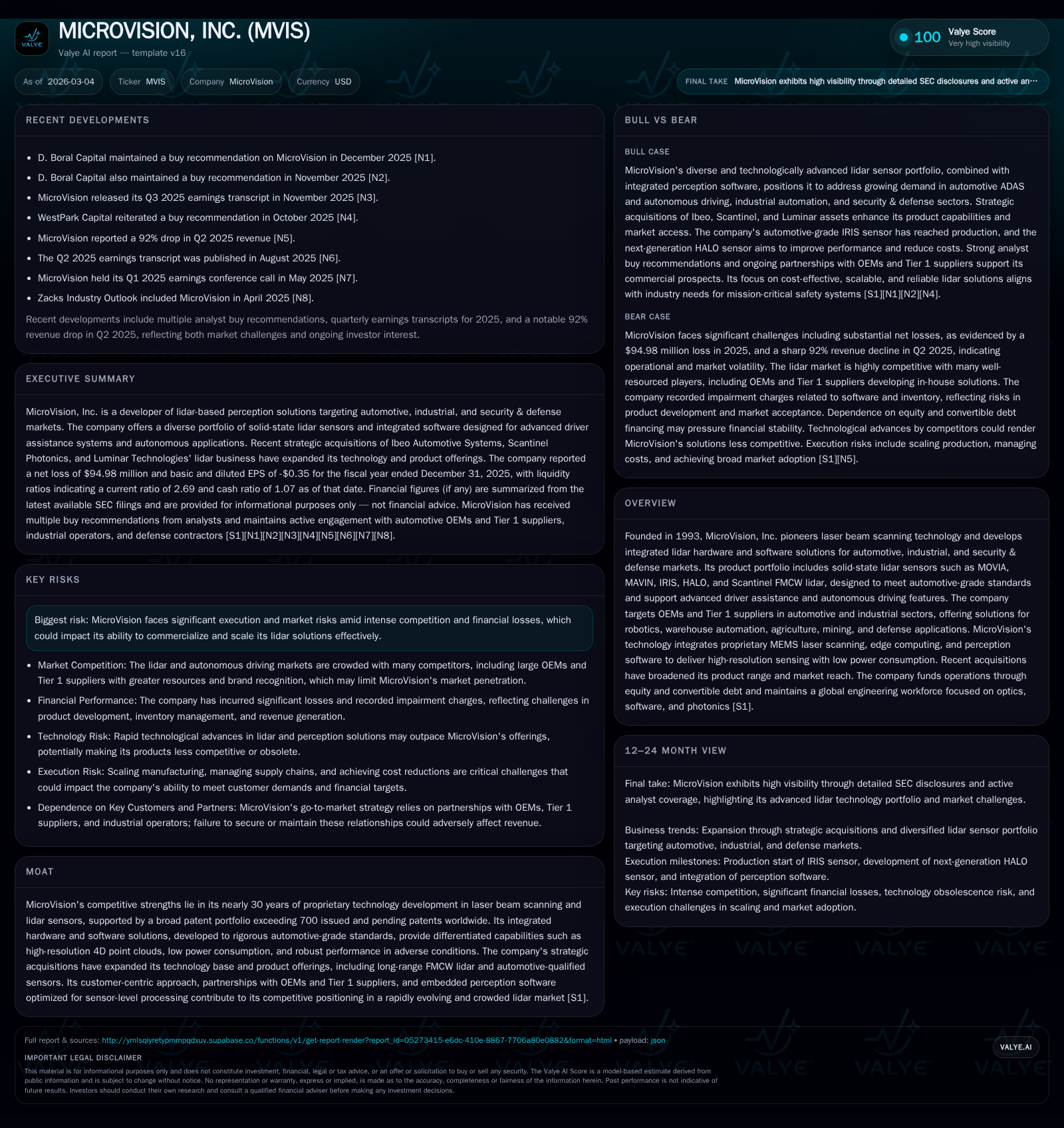

MicroVision Expands Lidar Portfolio Through Strategic Acquisitions While Managing Persistent Operating Losses

MicroVision integrates advanced lidar technologies targeting automotive and industrial markets amid significant financial challenges.

MicroVision, Inc., a pioneer in laser beam scanning and lidar solutions, has grown its technology base notably through recent acquisitions of Ibeo Automotive Systems, Scantinel Photonics, and Luminar Technologies’ lidar assets. Founded in 1993, the company focuses on automotive-grade lidar sensors and integrated perception software for automotive ADAS, industrial automation, and defense sectors. Despite these strategic moves to broaden product offerings and deepen capabilities, MicroVision continues to report substantial net losses and negative operating cash flows, reflecting ongoing execution risks. The company's future growth hinges on scaling production with OEMs and Tier 1 suppliers while navigating a competitive market landscape.

Company Overview and Historical Growth

MicroVision, Inc., established over three decades ago in 1993, has carved out a unique technological niche centered on laser beam scanning (LBS) technology leveraging micro-electromechanical systems (MEMS). Initially known for applications including augmented reality microdisplay engines and interactive displays, MicroVision pivoted strategically into the development of advanced lidar hardware and integrated software solutions targeting automotive, industrial automation, and security & defense markets [S1][S12][S13].

The company’s growth trajectory includes notable inorganic expansion through three key acquisitions: the strategic assets of Ibeo Automotive Systems GmbH in January 2023—which pioneered automotive qualified lidar sensors used by premium OEMs—Scantinel Photonics GmbH's assets for their unique FMCW lidar-on-chip technology acquired in January 2026, and luminary IP including IRIS and HALO long-range sensors plus the SENTINEL software platform from Luminar Technologies’ global lidar business finalized in early 2026 [S7][S8][S13]. These moves substantially broaden MicroVision’s product portfolio to encompass both short- to mid-range flash lidar (MOVIA series) and long-range time-of-flight plus FMCW sensors spanning different wavelengths (905nm to 1550nm), thus addressing a wider spectrum of use cases from ADAS to commercial vehicle autonomy [S13][S14].

The acquisitions also enhance software capabilities notably around perception stacks capable of small object detection, lane boundary recognition, dynamic object tracking/classification, sensor-level fusion for lower power consumption via edge processing SoC designs, which underscore MicroVision’s integrated systems approach rather than pure hardware play [S4][S12][S14]. This integrated offering is critical given OEMs' demands for scalable automotive-grade reliability combined with economic feasibility.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -95 | -59 | -83 | +2.0% | ||

| 2024 | 2 | -97 | -69 | -86 | -17.0% | |

| 2023 | -83 | -67 | -89 | -514.8% | ||

| 2022 | 0 | -13 | -38 | -54 | -100.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -59 | -171.0 |

| 2024 | -69 | -198.7 |

| 2023 | -69 | -86.5 |

| 2022 | -42 | -15.0 |

Source: SEC companyfacts cache [F1].

Source: MicroVision Annual Reports [F1]

Despite incremental revenue growth from minimal bases (zero revenue reported in FY2022), operating losses have deepened consistently reflecting scale-up costs, R&D investments especially tied to new acquisitions’ integration or impairment charges related to legacy inventories such as MOVIA L sensor write-downs recorded in FY2025 [S13]. While revenues remain nascent relative to expenses incurred for engineering talent (~190 employees mainly focused on optics/software/electronics across US/Germany), sales agreements at the OEM/Tier-1 level including volume supply contracts plus royalty streams represent foundational milestones yet largely unmaterialized financially.

Market Position and Future Growth Drivers

MicroVision positions itself squarely within several converging macro trends: increasing adoption of advanced driver assistance systems (ADAS) progressing towards autonomous driving capabilities (L2+ / L3 levels); accelerated automation within industrial sectors encompassing robotics-driven warehouses, agriculture machinery automation, mining vehicles; plus security & defense applications leveraging drone/UAV surveillance enhancements [S11][S12]. Their technology claims several distinguishing features appreciated by customers: robust performance in adverse weather due to high resolution point clouds across multiple wavelengths; remarkably low power consumption achieved via embedding perception algorithms optimized for sensor-edge computing platforms; automated calibration reducing integration costs; automotive qualification processes through premium OEM working relationships underpinning trustworthiness standards compliance [S4][S14].

The immediate availability of MOVIA and IRIS sensors supports a dual revenue stream from production royalties linked to automotive OEM deliveries alongside direct hardware sales into industrial use cases featuring automated guided vehicles (AGVs), autonomous mobile robots (AMRs), collaborative robots (cobots), etc., where ruggedness and size constraints apply [S5][S15]. Additionally,

- The HALO sensor is expected to deliver substantial performance improvements—including a potential fourfold increase in sensing capability—while reducing size/cost/power consumption compared with IRIS (its predecessor), further bolstering prospects for mass-market adoption within the passenger vehicle segment [S14].

- The Scantinel FMCW solution unlocks longer range detection critical for commercial truck autonomy requiring enhanced road data collection fidelity over extended distances [S7].

- SENTINEL full-stack safety/autonomy software acquisition introduces new end-to-end safety validation capabilities important for certification-heavy automotive regulatory environment.

However, the roadmap toward commercial scale involves penetrating a crowded landscape featuring both large incumbents investing heavily in their own vertically integrated ADAS/lidar tech stacks as well as numerous specialized startups targeting niche sensing or perception layers simultaneously [S9]. Hence MicroVision’s strategy emphasizes leveraging its broad patent portfolio (>700 patents/pending worldwide covering systems controls, miniaturization patterns, scan locking tech immune from sunlight/interference) alongside co-development partnerships with Tier-1 suppliers to embed its products early into automotive platforms where changing component designs or reliability shifts could generate switching costs advantageous to incumbents otherwise [S9][S15].

Financial Performance Analysis

Over the last three fiscal years ending FY2025:

- Revenue grew nominally but remains under $3 million annually.

- Operating losses hover near $80–90 million yearly.

- Net losses approximate $95 million by FY2025 end.

- Operating cash flows are deeply negative ranging from -$38 million in calendar year 2022 worsening to nearly -$59 million by FY2025.

- Capex is relatively low given heavy focus on R&D/service model (~$0.7 million in last reported year).

- Equity shrank from nearly $96 million after FY2023 following impairments but stabilized around $55 million by end-FY25 aided by fresh financing rounds.

These figures reflect an early-stage high R&D investment cycle typical among deep tech hardware companies aiming for breakthrough product-market fit coupled with commercialization ramping phase that requires going beyond proof-of-concept deployments toward scalable manufacturing agreements.

Cash position stood at about $32 million entering calendar year-end 2025 providing runway into at least early-to-mid 2026 before additional capital needed absent rapid revenue inflection [F1]. In response to liquidity requirements:

- The company completed two senior secured convertible note financings totaling approximately $43 million maturing March 2028 with zero coupons but conversion rights at strike prices around $0.88/share designed to preserve cash flow while extending debt maturity profile [S16][S22][S23].

- Convertible notes come with customary covenants limiting further indebtedness without lender consent plus maintaining minimum liquidity thresholds enabling cautious balance sheet management amid operating deficits.

Capital allocation clearly prioritizes technology advancement as evidenced by steady engineering headcount retention despite restructuring actions taken in late prior years that reduced dedicated resources on peripheral programs such as MOSAIK validation tools while refocusing priorities towards MAVIN/MOVIA/HALO sensor lines essential for near-term commercialization efforts [S13][S17]. MicroVision currently does not pay dividends nor engage substantially in share repurchases reflecting reinvestment needs characteristic of its development stage business model.

Risks and Challenges

A number of risk vectors warrant close monitoring:

- Execution risk dominates given ongoing lack of profitability despite more than three decades since founding implying persistent hurdles scaling high-volume sensor production still unresolved.

- Competitive risk is acute as many well-capitalized rivals have deeper customer penetration or exclusive contractual relationships potentially marginalizing MicroVision’s offerings despite technological merits [S9].

- Technological obsolescence risk stems from fast-evolving autonomy sensing modalities whereby incremental R&D investments that fail to keep pace could render existing patents or products less valuable.

- Dependence on a relatively small number of customers (automotive OEMs/Tier-1 suppliers) means order delays or cancellations could materially impact top-line visibility especially when revenue base is modest currently.

- Supply chain constraints affecting specialty semiconductor sourcing for ASICs/MEMS components also pose risk given industry-wide chip shortages experienced broadly over recent years.

- Regulatory environment changes particularly regarding data security/privacy or safety certifications may require costly adaptation efforts impacting margins/change timelines [S10][S20].

- Cybersecurity remains an enterprise focus area given complex embedded computing elements inside sensors; management oversight includes quarterly audit committee reporting supplemented by external consulting support tasked with strengthening defenses amidst evolving threat landscape [S1][S20].

What To Watch Going Forward — Analysis

Absent explicit forward guidance details publicly disclosed currently, key milestones pertinent for assessing progress will include:

- Evidence of scaled serial production shipments with automotive OEMs or Tier-1 suppliers anchoring royalty or volume-based sales ramping beyond pilot stages.

- Validation of new generation HALO sensor attributes meeting promised performance/size/cost targets enabling broader adoption especially if it becomes standard building block inside next-gen passenger vehicle platforms.

- Expansion traction within industrial markets demonstrating wins amongst robotics automators or warehouse operators utilizing MAVIN/MOVIA lines standalone or combined with perception stacks customized per vertical needs.

- Success integrating FMCW Scantinel-derived technologies addressing niche long-range requirements especially commercial trucking fleet deployments seeking higher autonomy levels.

- Improvements narrowing operating loss margins demonstrating scaling benefits commensurate with higher manufacturing volumes/operational leverage.

- Timely completion of SEC required registration statements relating to convertible note share issuances along with stable shareholder-approved capital structure facilitating future financing flexibility without disruptive dilution events seen historically.

Finally, technology leadership evidenced by execution on next-generation chipsets underpinning HALO's enhancements coupled with sustained patent portfolio filings will be critical indicators that MicroVision can maintain differentiation against competitors who leverage silicon photonics innovations or alternative sensing architectures like solid-state flash LiDAR arrays without moving parts but often constrained by cost/performance tradeoffs.

Conclusion

MicroVision embodies a classic deep-tech innovation enterprise aiming at delivering groundbreaking integrated lidar solutions tailored specifically for automotive ADAS/autonomy alongside industrial automation applications supported by solid-state MEMS scanning technology perfected over nearly thirty years supported by wide patent coverage exceeding seven hundred active filings globally. The company’s recent aggressive acquisition strategy enriching its portfolio with differentiated FMCW lidar modules and proprietary safety software reflects intent to become a comprehensive supplier addressing multiple autonomy market segments requiring stringent safety certifications combined with cost-sensitive mass production scalability.

Nonetheless, the financial profile reveals continuing high operating losses approaching $95 million annually paired with deeply negative operating cash outflows underscoring significant execution challenges remain before profitability can be realized at scale. Liquidity is supported moderately through convertible debt arrangements although dependency on capital markets remains intact until sustainable positive cash flow emerges backed by validated customer ramps.

Investors analyzing MicroVision should track ongoing customer program developments tied directly to their core sensor products MOVIA/IRIS/HALO/MAVIN alongside software stack SENTINEL rollout timelines while carefully weighing competitive threat evolution from dominant incumbent OEM suppliers developing internal solutions versus emerging rival pureplays aggressively expanding their foothold across ADAS/autonomy segments globally.

This analysis synthesizes disclosed financial data and business descriptions as reported by MicroVision in SEC filings up to March 4, 2026 ([F1],[S1]-[S29]). It does not offer investment advice but aims to objectively present operational context, financial trends, market strategies, risks identified therein along with interpretive commentary to aid understanding within the evolving lidar/autonomy industry landscape.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments