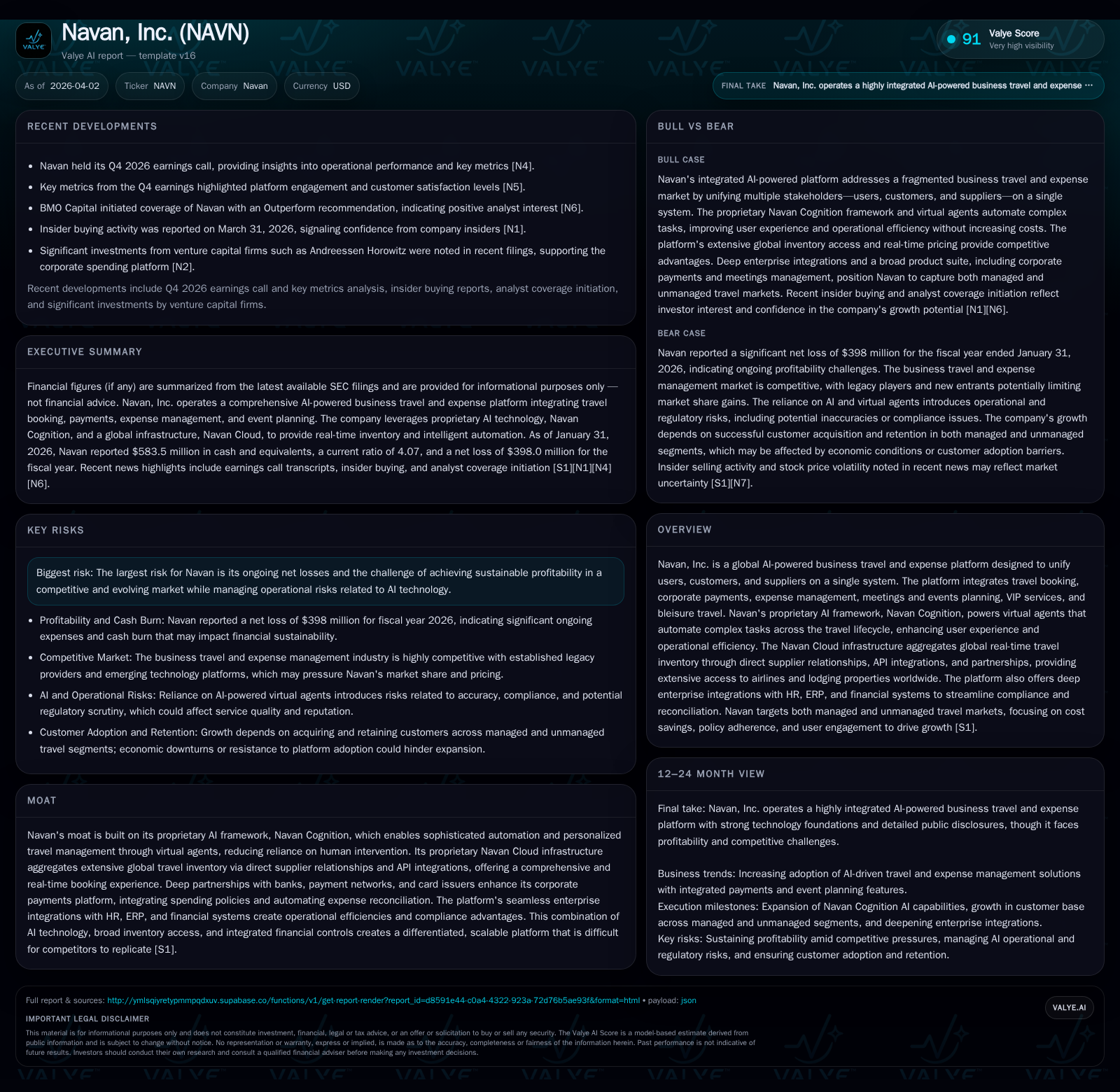

Navan's AI-Driven Platform Faces Profitability Hurdles Despite Robust Growth and Market Expansion

Navan leverages proprietary AI and integrated travel solutions to capture managed and unmanaged business travel spend but continues navigating significant losses and competitive pressures.

Navan, Inc. has established a compelling AI-powered travel and expense platform that integrates booking, payments, and expense management into one system, enabling deep organizational adoption across diverse customers globally. Its proprietary Navan Cognition AI framework and the Navan Cloud infrastructure create scale advantages by aggregating extensive global inventory and automating complex travel lifecycle tasks. The company delivered rapid revenue growth driven by increased customer acquisition in both managed and unmanaged travel markets; however, it remains unprofitable with substantial operating losses and ongoing investments aimed at expanding offerings and improving market penetration. Key risks include maintaining sustainable profitability, managing competition from legacy players and AI-native entrants, and regulatory compliance regarding AI usage. Capital structure shows a solid liquidity position yet reflects the need for disciplined cost control going forward.

Company Overview

Navan, Inc. operates as a global AI-powered business travel platform aiming to unify users, corporate customers, and suppliers on one comprehensive system [S4][S13]. Unlike traditional legacy service-heavy travel providers reliant on fragmented systems, Navan is built on cutting-edge infrastructure combining its proprietary AI framework—Navan Cognition—with a cloud-based platform aggregating extensive travel supplier partnerships. This unique combination enables seamless integration across booking flights, lodging, corporate payments, expense management, meetings/events planning, VIP services, and bleisure travel [S4][S17].

The company's foundational thesis is that harmonizing all stakeholders within the ecosystem—travelers, corporations controlling spend policies, and suppliers—on one scalable platform powered by advanced artificial intelligence unlocks operational efficiencies and improves user experience significantly beyond what legacy vendors provide [S13]. Navan emphasizes a "flywheel" effect whereby increasing user adoption attracts more suppliers through volume incentives; in turn broadening inventory availability enhances traveler choice while embedding compliance tools drives cost control for customers [S13].

Historical Growth and Performance

Navan has experienced rapid top-line growth fueled predominantly by two key sales motions: a traditional sales-led approach targeting mid-sized to large enterprises with existing or legacy T&E solutions seeking modernization; complemented recently by product-led growth targeting smaller firms often categorized as the "unmanaged" segment that historically relied on manual or spreadsheet-based tracking methods [S5][S6][S25]. This diversified go-to-market approach has progressively expanded the customer base across company sizes.

The company’s user satisfaction indicators reinforce operational momentum: for fiscal year ended January 31, 2026 (FY '26), overall customer satisfaction (CSAT) registered at an impressively high 96%, while its virtual agents garnered an 81% CSAT score comparable to humans—underscoring effective automation—and the platform's net promoter score stood at an industry-leading 45 [S13].

From a financial perspective using the latest annual data as of FY '26 from SEC XBRL extracts [F1]:

Historical performance (annual)

| FY |

|---|

| 2026 |

Source: SEC companyfacts cache [F1]. |(a) derived from CFO minus Capex per [F1].

Note: Revenue figures are not disclosed directly in the available tagged data; however operating losses clearly reflect intensive reinvestment during this scaling phase.

Operating losses have been substantial reflecting continued investments in product development especially around AI technologies like Navan Cognition alongside customer acquisition costs related to scaling internationally. Free cash flow turned positive largely due to improved operating cash generation offsetting capital expenditures modestly [F1]. The current ratio above 4x highlights that liquidity is adequate at present though the company must balance growth investments against capital discipline moving forward [F1][S10][S19].

Future Growth Prospects

Navan’s future growth depends heavily on three pillars:

- Expanding penetration within managed customers: With a core portfolio landing clients initially on its Travel offering then cross-selling Corporate Payments and Expense Management modules — expanding functionality encourages deeper wallet share capture over time [S25].

- Capturing unmanaged market share: Addressing smaller firms historically deterred by expensive legacy platforms via streamlined self-service onboarding allows Navan access to approximately 65% of global business travel spend traditionally unmanaged—representing a sizeable greenfield opportunity [S5][S7][S25].

- International expansion: Having built global backend integrations reaching over 600 airlines globally plus two million lodging options via direct APIs augments service breadth for multinational clients venturing beyond U.S.-centric markets [S14][S17]. Ongoing investment aims to broaden geographic reach further.

Strategic initiatives also focus on continually upgrading Navan Cognition’s autonomous virtual agents leveraging advancements in large language models fused with proprietary machine learning algorithms. This strengthens differentiation versus competitors who may lack modular programmable AI architectures tailored for complex policy management workflows inherent in business travel [S13][S15][S17].

Potential headwinds include ongoing macroeconomic uncertainty affecting corporate travel budgets amid inflationary pressures or geopolitical instability which could depress demand unpredictably given usage-based revenue components embedded in packages [S1][S2][S11]. Additionally, evolving remote work norms may dampen traditional business trip frequency though Navan seeks to offset this somewhat via bleisure offerings blending personal leisure bookings incentivized through rewards earned on employer-funded trips [S13][S21].

Forecasts & Milestones

Explicit forward guidance is not published publicly; however key metrics to watch include:

- Growth rates in annual recurring revenue segments split between Travel versus Payments/Expense modules.

- Expansion within existing client accounts measured by multi-product adoption rates indicating success in cross-selling.

- Market share gains in targeted unmanaged customer cohorts gauged through self-service conversion metrics.

- Progression of AI automation coverage reducing per-interaction human agent load monitored via virtual agent CSAT trends.

- International revenues as percent total indicating execution of geographic diversification plans.

- Gross margin improvement signaling operating leverage as scale efficiencies materialize.

Investors should stay alert for quarterly updates detailing above metrics as well as commentary around regulatory compliance relating to AI usage given emerging legal frameworks expected globally [S22].

Returns & Capital Allocation

According to available FY '26 data:

- Return on Equity sits negative at approximately -33% reflecting reported net losses relative to shareholder equity amid steep scaling costs [F1].

- Free cash flow turned positive at roughly $33 million after deducting capex (

$3.2 million) from cash flow from operations ($36.5 million), suggesting improving operational cash generation despite losses [F1]. - Cash & equivalents hold steady near $584 million supporting runway commitments with conservative current liabilities totaling ~$321 million giving comfortable short-term liquidity cushions reflected by ~4x current ratio [F1][S10].

- There is no indication of dividend distribution or share repurchases during this period aligning with reinvestment priorities for growth phases rather than capital returns [F1].

The company carries meaningful debt obligations requiring careful service management but benefits from existing credit facilities subject to covenant monitoring which if violated could accelerate repayment requirements—a risk amplified by volatile macroeconomic conditions demanding prudent capital structure stewardship [S10][S19].

Competitive Environment & Moat Considerations

Navan competes against entrenched incumbents like BCD Travel and SAP Concur while contending with newer digital-native entrants harnessing AI-enabled tools. Differentiation stems from:

- Proprietary Navan Cognition which orchestrates programmable autonomous virtual agents delivering personalized policy adherence automation at scale—a step above static rules engines common in traditional platforms [S12][S15].

- Integrated end-to-end platform unifying booking through post-trip expense reconciliation improves user experience reducing friction points encountered when stitching together multiple vendors manually.

- Broad supplier network established through direct API integrations supplemented with GDS connectivity ensures expansive inventory access critical to global travelers [S8][S9]

- Deep financial ecosystem partnerships including card issuers such as Brex & Citi extend payment functionality amplifying value proposition relative to standalone T&E vendors [S9].

However risk factors loom large: competitive pressure might compel increased spending on marketing & R&D eroding margins further; regulatory shifts tied to data privacy or AI transparency could impose additional costs or constrain innovation paths; persistent net losses question timing of sustainable profitability milestone achievement—all warrant vigilant monitoring by stakeholders [S11][S16][S18][S20][S23].

Regulatory & Litigation Risks

Legal landscape evolves rapidly especially regarding personal data protection laws like CCPA alongside emerging statutes regulating GenAI use impacting operational flexibility. Compliance failures entail fines plus reputational damage complicating growth trajectory [S16][S22][S24]. Ongoing securities litigation alleges misleading disclosures adding financial strain potential along with distraction from core execution priorities [S23].

Conclusion & Watch Points

Navan stands out architecturally as a next-generation AI-powered corporate travel platform integrating expansive inventory access with sophisticated automation technology delivering tangible user satisfaction improvements demonstrated by high CSAT scores. The dual-pronged approach into managed enterprise clients plus broad untapped unmanaged SMB markets positions it well for continued top-line momentum.

Nonetheless substantial losses coupled with intense competition and regulatory uncertainties cast shadows over near-term profitability expectations necessitating careful scrutiny of upcoming quarterly trends particularly regarding:

- Revenue segmentation growth,

- Customer retention/cross-sell ratios,

- Virtual agent deployment effectiveness,

- Operating leverage progression,

- Capital expenditure discipline,

- Regulatory developments impacting AI usage criteria. Investors must balance enthusiasm for innovation-fueled expansion against pragmatic recognition of the execution complexities large-scale technology platforms face moving toward sustainable profitability.

Disclaimer: This report is intended solely for informational purposes without providing investment recommendations or advice. All facts cited originate from official SEC filings or reputable news sources referenced herein; no speculative assumptions have been made beyond disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments