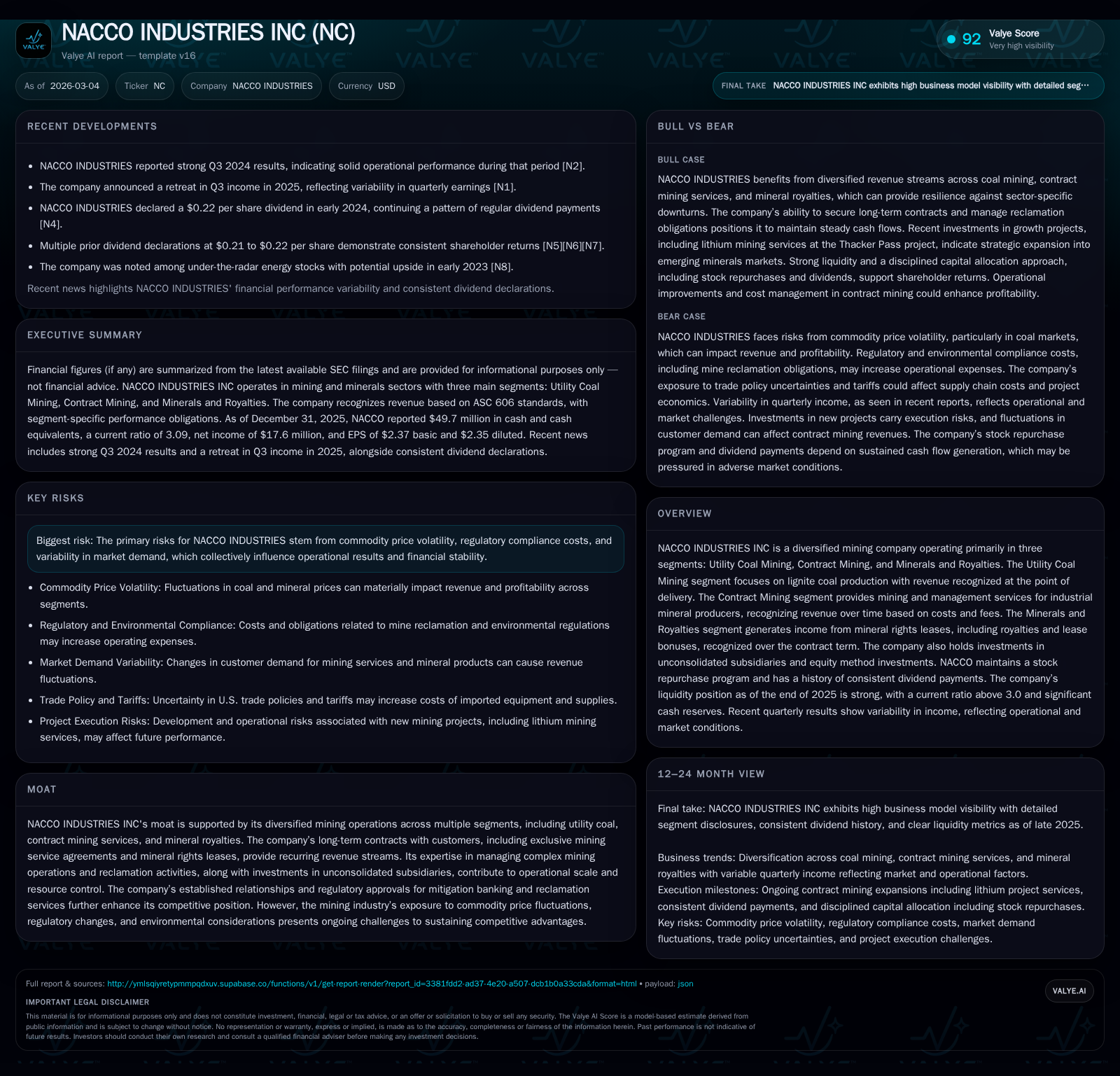

NACCO Industries’ Revenue Rebound and Capital Strategy Under Pressure

A sharp revenue decline contrasts with robust operating cash flows as NACCO balances capital deployment amid enduring mining sector pressures.

In 2025, NACCO Industries Inc experienced a pronounced 63.1% drop in revenue year-over-year, driven by shifts across its Utility Coal Mining, Contract Mining, and Minerals and Royalties segments. Despite top-line challenges, the company recorded a strong rebound in operating cash flow (+128.4% YoY), reflecting operational efficiencies and cost management amidst volatile commodity dynamics. Capital allocation remained disciplined with lower capital expenditures and ongoing dividends and buybacks, all supported by a solid liquidity position entering 2026. Key risks include commodity price volatility and regulatory compliance costs affecting long-term growth sustainability.

Segment Dynamics Behind Historical Financial Trends

NACCO Industries operates three core segments: Utility Coal Mining, Contract Mining, and Minerals and Royalties. The company experienced a dramatic top-line reversal in 2025 with total revenue plummeting to approximately $104.8 million from nearly $284.2 million in the prior comparable period — a staggering 63.1% decline [F1]. This sharp contraction largely stems from diminished volumes and demand within the Utility Coal segment where lignite production feeds exclusively contracted thermal power plants operating under long-term agreements [S5].

Contract Mining, providing outsourced mining services to industrial mineral producers, demonstrated relative resilience with incremental gains but did not offset the steep drop in coal revenue fully. Meanwhile, the Minerals and Royalties segment benefits from stable royalties and lease bonuses but is inherently sensitive to mineral market prices and production variability [S15].

Operating income followed the downward trajectory slumping by 38.4% to $21.9 million in 2025 [F1], reflective of margin compression amid lower revenue but nonetheless sustaining profitability due to contract structures that shift operating costs largely onto customers.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 18 | 51 | 22 | 49 | -47.9% |

| 2024 | 34 | 22 | 36 | 55 | +185.2% |

| 2023 | -40 | 54 | -70 | 45 | -153.4% |

| 2022 | 74 | 68 | 70 | 43 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 3 | 2 |

| 2024 | 7 | 10 | -32 |

| 2023 | 6 | 3 | 9 |

| 2022 | 6 | 25 |

Source: SEC companyfacts cache [F1].

Table summarizes NACCO’s recent financial performance highlighting the sharp revenue drop but contrasting CFO strength [F1].

Drivers of NACCO’s 2025 Operating Income and Cash Flow Patterns

Despite top-line weakness, NACCO demonstrated a strong turnaround in operating cash flows which doubled year-over-year to roughly $50.9 million [F1]. This divergence is attributable partly to working capital management improvements alongside reduced non-cash inventory impairments that appeared elevated in prior periods [S13].

Profit margins have been pressured owing to legacy dragline operations management costs within Contract Mining alongside fluctuating reimbursable expense structures wherein cost reimbursements lag revenue recognition timing [S15]. The application of ASC 606 accounting principles distinctly affects the timing patterns — with Utility Coal revenues recognized at 'point-in-time' on lignite delivery while Contract Mining recognizes fees 'over time' based on input methods calibrated to incurred costs plus fees [S10].

A notable component includes earnings from unconsolidated subsidiaries operating as variable interest entities (VIEs) financed predominantly by customers without recourse to NACCO — these arrangements stabilize income but limit upside exposure or losses beyond equity stakes [S7][S11].

Revenue Pressures and Operational Adaptations Across Mining Segments

The Utility Coal Mining segment suffered significant volume contractions largely due to early retirements or operational shifts of customer plants requiring lignite fuel provision under exclusive contracts — for instance, the Sabine Mine ceased deliveries following early plant retirements and commenced final reclamation funded by customers through September 2026 [S17]. This contract structure insulates NACCO from commodity spot price volatility but reduces scale.

Contract Mining has grown moderately through operating quarries across multiple U.S states and exclusive service contracts such as Sawtooth Mining LLC’s role at the Thacker Pass lithium project in Nevada — targeting initial lithium production phases that deliver diversified base revenues beyond traditional coal exposure [S7][S25]. This segment utilizes dragline equipment whose construction progress provides long lead-time visibility into operational ramp-ups.

Minerals and Royalties revenues arise from leasing mineral rights on fixed or variable royalty bases; these contracts include an upfront lease bonus recognized over contractual terms typically three to five years plus ongoing sales-based royalties subject to production volumes exceeding forecasted thresholds [S15]. This staggered recognition introduces variability tied closely to macro commodity pricing trends.

Contract Mining Growth Prospects and Strategic Positioning

Contract Mining emerges as NACCO’s strategic diversification vector amidst coal market headwinds [S25]. The exclusive management services agreement for Thacker Pass lithium mining demonstrates entry into higher-growth industrial minerals applications critical for battery supply chains supporting electric vehicles.

Mitigation banking operations provide complementary environmental credit sales regulated by federal agencies such as the U.S Army Corps of Engineers — these credits represent distinct performance obligations with phased release schedules contributing additional recurring service revenues alongside reclamation contracting engagements [S15].

Nevertheless, regulatory complexities tied to reclamation liabilities pose ongoing execution risks; contractual frameworks obligate customers for final reclamation funding though some joint ventures retain responsibility for mine permits requiring coordinated mitigation efforts [S7]. Emerging federal tariff policies may influence supply chain costs for imported equipment used in mining operations adding external cost pressures [S16].

Capital Allocation Priorities: Dividends, Buybacks, and Investment Levels

Despite earnings pressure, NACCO sustained dividend payments totaling approximately $7.3 million in 2025 [F1], underscoring shareholder return consistency since inception of payouts.

Share repurchases slowed markedly compared to prior years — total buyback expenditure dropped to roughly $2.5 million versus near $10 million in the previous year — signaling management caution on deploying capital amid top-line uncertainties and preserving liquidity buffers [F1][S26].

Capital expenditures declined by around 11%, standing at $48.6 million as investments refocused on maintenance capex supporting core mining assets plus selective enhancements such as dragline construction projects supporting Contract Mining growth [F1][S8][S26]. Return on equity approximated a moderate 4.1%, reflective of earnings contraction tempered by sizeable equity base built over decades and reinvestment policies [F1].

Liquidity Strength and Balance Sheet Composition Entering 2026

At December-end 2025, NACCO reported a robust current ratio exceeding 3x driven by substantial cash holdings near $49.7 million alongside current assets totaling roughly $214.9 million versus current liabilities near $69.6 million [F1][S6][S14][S29]. This liquidity profile supports operational flexibility amid ongoing commodity pricing volatility.

Long-term debt levels remained manageable at approximately $25.9 million complemented by revolving credit facilities around $65 million available for working capital needs or tactical investments [S6][S7][S14].

Asset retirement obligations related principally to mine reclamation amounted around $50 million split between current and long-term liabilities reflecting estimated future remediation commitments per regulatory mandates with liability reimbursement provisions secured via customer-funded contracts thus limiting direct balance sheet risk concentration for NACCO [S18][S29]. Unconsolidated subsidiary investments totaled roughly $16 million reinforcing diversified asset backing outside consolidated entities [S7][S11][S27].

Regulatory and Market Risk Factors Impacting Forward Outlook

NACCO faces intrinsic risks from fluctuations in coal demand compounded by tightening environmental legislation increasing compliance cost burdens including mine reclamation obligations governed under multi-state frameworks monitored federally [S4][S12]. These factors impose operational cost volatility despite contract structures designed to pass such expenses onto customers where feasible.

Commodity price swings continue as principal uncertainty determinants impacting royalty streams along with potential delays or reductions in industrial mineral projects reliant on global supply chain conditions and geopolitical developments affecting trade policies including tariffs potentially raising equipment input costs [S16]. Litigation contingencies exist but remain judged unlikely to materially affect financial outcomes per disclosures.

Key Metrics to Monitor: Forecasts, Margins, and Contract Developments

Absent explicit forward guidance or disclosed milestones beyond contract highlights noted within filings, sector watchers should prioritize metrics such as segment profit margins particularly shifts related to dragline equipment utilization efficiency in Contract Mining alongside updated throughput rates at key long-term coal contracts approaching final reclamation phases.

Monitoring renewal or extension outcomes of exclusive mining service agreements including emerging lithium sector engagements will be critical given their role in diversifying earnings streams away from diminishing thermal coal operations.

Capital expenditure realization against planned dragline commissioning schedules will offer visibility into near-term operational scaling potential while observing deferred recognition timing embedded within ASC606 compliance frameworks associated with milestone-linked fee recognition are also advisable for comprehensive financial outlook interpretation.

This report is prepared solely for informational purposes based on NACCO Industries Inc.’s public SEC filings as of March 4, 2026 ([F1],[S#]) without any investment advice or recommendation provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments