NextEra Energy's Q4 2025: Navigating Regulated Utility Stability Amid Renewable Growth and Regulatory Risks

A detailed analysis of NextEra Energy’s recent earnings, regulatory moat, green transition efforts, financial health, and the emerging AI narrative shaping its outlook.

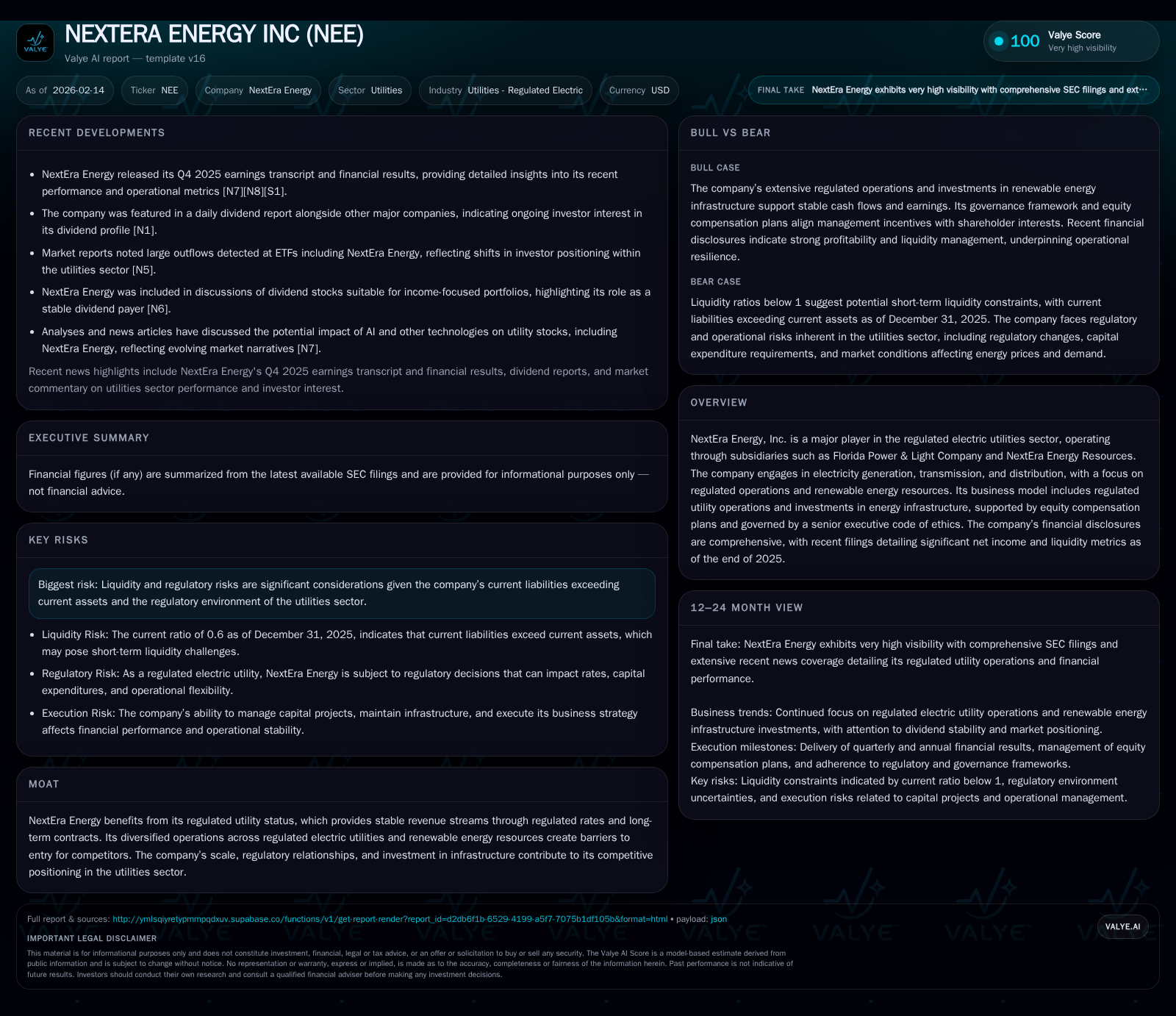

NextEra Energy reported a strong net income of $6.835 billion for 2025, reflecting resilience amid continued regulatory complexity. The company’s regulated utility operations underpin stable cash flows but face regulatory headwinds that could constrain returns. Its ambitious renewables push drives growth potential yet invites legislative scrutiny and market challenges. Liquidity metrics signal caution given current liabilities outpacing current assets, while AI-related innovation remains a speculative opportunity rather than a core business driver. Comparisons with industry peers highlight NextEra’s scale advantage, though valuation debates persist. Governance frameworks align management incentives with shareholder interests, fortifying long-term strategy execution.

Q4 2025 Earnings: Triumphs and Concerns

NextEra Energy closed 2025 with a commanding net income figure of approximately $6.835 billion [F1], exceeding analyst expectations as noted in recent earnings transcripts [N4][N5]. This performance reinforced confidence among investors, buoyed further by dividend yield discussions highlighting the company's commitment to returning capital to shareholders even amid sector volatility [N10]. The quarterly financial release demonstrated robust earnings growth across both regulated utility segments and non-regulated renewable operations [N6][N7]. However, underlying this success are nuanced concerns about liquidity positions and regulatory exposures that tempers enthusiasm.

Regulatory Moat: Stability’s Blessing with Caveats

NextEra’s foundational competitive advantage derives from its status as a heavily regulated electric utility operating principally through Florida Power & Light Company (FPL) and its subsidiaries [S1]. Regulation ensures predictable revenue via rate-setting mechanisms overseen primarily by the Florida Public Service Commission (FPSC), which governs retail rates, cost recovery clauses, capital investment approvals, and return on equity determinations [S1]. This framework provides stability essential to infrastructure-intensive utilities but introduces risk if regulators deny or delay recovery of costs deemed excessive or investments considered imprudent. Political dynamics in Florida add complexity; volatile environments can reverberate through rate cases affecting permitted earnings levels [S1]. Hence, while the moat supports steady cash flows insulated from open market competition, it also imposes constraints on profitability upside and agility.

Renewables Drive: Fueling Growth or Regulatory Tug-of-War?

NextEra’s strategic emphasis on renewable energy—through its NextEra Energy Resources segment—represents both a growth engine and a battleground for regulatory navigation [S1]. The company benefits from federal production tax credits (PTCs) incentivizing wind and solar projects, facilitating expansion at scale [S1]. Its renewables portfolio complements the regulated monopoly utilities by diversifying generation sources aligned with broader decarbonization trends. Nonetheless, transitioning legacy generation assets faces permitting hurdles, community opposition risks, and potential legislative uncertainties which could delay pipeline development or increase capital costs [S1]. Balancing rapid renewables build-out while maintaining stable rate recovery adds layers of complexity. The interplay between evolving policy landscapes and market demand influences NextEra's ability to capitalize fully on green energy investments.

Leverage and Liquidity: The Double-Edged Sword

Financial disclosures expose next-level liquidity scrutiny for NextEra. Despite robust net income, the company reported a current ratio of approximately 0.6 at year-end 2025, reflecting current liabilities roughly $22.8 billion versus current assets near $13.6 billion [F1]. While cash and equivalents totaled about $2.8 billion providing some short-term buffer, the gap suggests ongoing reliance on capital markets or asset management to fund operational needs [F1][S1]. Management acknowledges these liquidity challenges in MD&A commentary stressing strategic capital planning but warns of inherent risks if access tightens or costs escalate unexpectedly [S1]. Such financial structure nuances raise potential pressure points on credit profiles or investment capacity that investors should monitor closely despite strong underlying earnings.

AI and Technological Innovation: A Utility’s New Frontier

The conversation around artificial intelligence (AI) integration into utilities has gained momentum recently with NextEra occasionally referenced as a candidate beneficiary of AI-driven operational efficiencies or new digital revenue streams [N8][N9]. Market narratives speculate that AI could enhance grid management, predictive maintenance, demand forecasting, and customer engagement within regulated frameworks. However, given the nature of entrenched regulation paired with capital-intensive infrastructure assets, tangible AI impacts for NextEra remain in nascent stages more emblematic of long-term optionality than immediate transformation [N9]. Prudence dictates framing AI as a speculative upside overlay rather than material near-term contributor at present.

Comparative Landscape: NextEra Among Peers

Placing NextEra alongside publicly traded peers such as AES Corporation (AES), Ameren Corporation (AEE), Exelon Corporation (EXC), reveals strengths in scale of renewable assets coupled with diversified regulated electric operations [N1][N2][N3]. Comparisons reveal differing valuation approaches reflective of distinctive risk tolerances around regulatory exposure versus growth initiatives. For example, recent analyses debate AES versus NEE stock value propositions emphasizing NextEra's premium multiple justified by Integrated transmission plus renewables platforms against AES's opportunistic growth approach [N12]. Exelon’s Q4 results iterate heightened capex plans showing peer intentions within clean energy transition frameworks [N1]. These comparisons paint an industry grappling between legacy regulation certainty and aggressive green investment ambitions where NextEra often occupies leadership yet contested ground.

Executive Ethics and Incentives: Aligning Management and Shareholders

Governance disclosures articulate rigorous oversight through the Senior Executive Code of Ethics binding top executives including CEO and CFO under standards requiring integrity in financial reporting and decision-making processes [S1]. Equity compensation plans disclosed reveal substantial participation incentives aligning management payoffs with long-term stockholder value creation via awards tied to performance shares and restricted stock units totaling millions of shares available under approved incentive schemes [S1]. This structured alignment aims to foster stewardship conducive to navigating complex regulatory environments while executing ambitious capital projects responsibly.

Stock Outlook: Valuation, Risks, and Catalysts

Synthesizing financial data with qualitative factors presents a balanced forward view. Articles citing "3 Reasons NEE Shares Could Soar" emphasize factors such as green asset momentum, dividend attractiveness amidst low interest rates, and technology adoption potentials as primary catalytic drivers [N11]. Conversely, documented SEC risk disclosures highlight perpetual regulatory clearance uncertainty for cost recovery alongside liquidity strains due to notable short-term obligation volumes as critical downside considerations [S1]. Market participants thus confront juxtaposed narratives: a stable utility franchise advancing renewables versus an evolving macro-political landscape capable of injecting episodic volatility into returns. Investors attentive to these dynamics should weigh dividend sustainability against upcoming regulatory proceedings while monitoring enhancements in financial flexibility.

This analysis incorporates publicly available information from company filings including the Form 10-K for fiscal year ended December 31, 2025 [S1], alongside relevant news reports capturing recent earnings reflections and sector developments [N4]-[N14], supplemented by refreshed companyfacts data snapshots [F1]. It is intended solely for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments