NEPHROS INC Expands FDA-Cleared Water Filtration Amid Supply and Market Risks

Nephros focuses on specialized medical-grade water filtration with growing commercial applications while managing supplier concentration and installation risks.

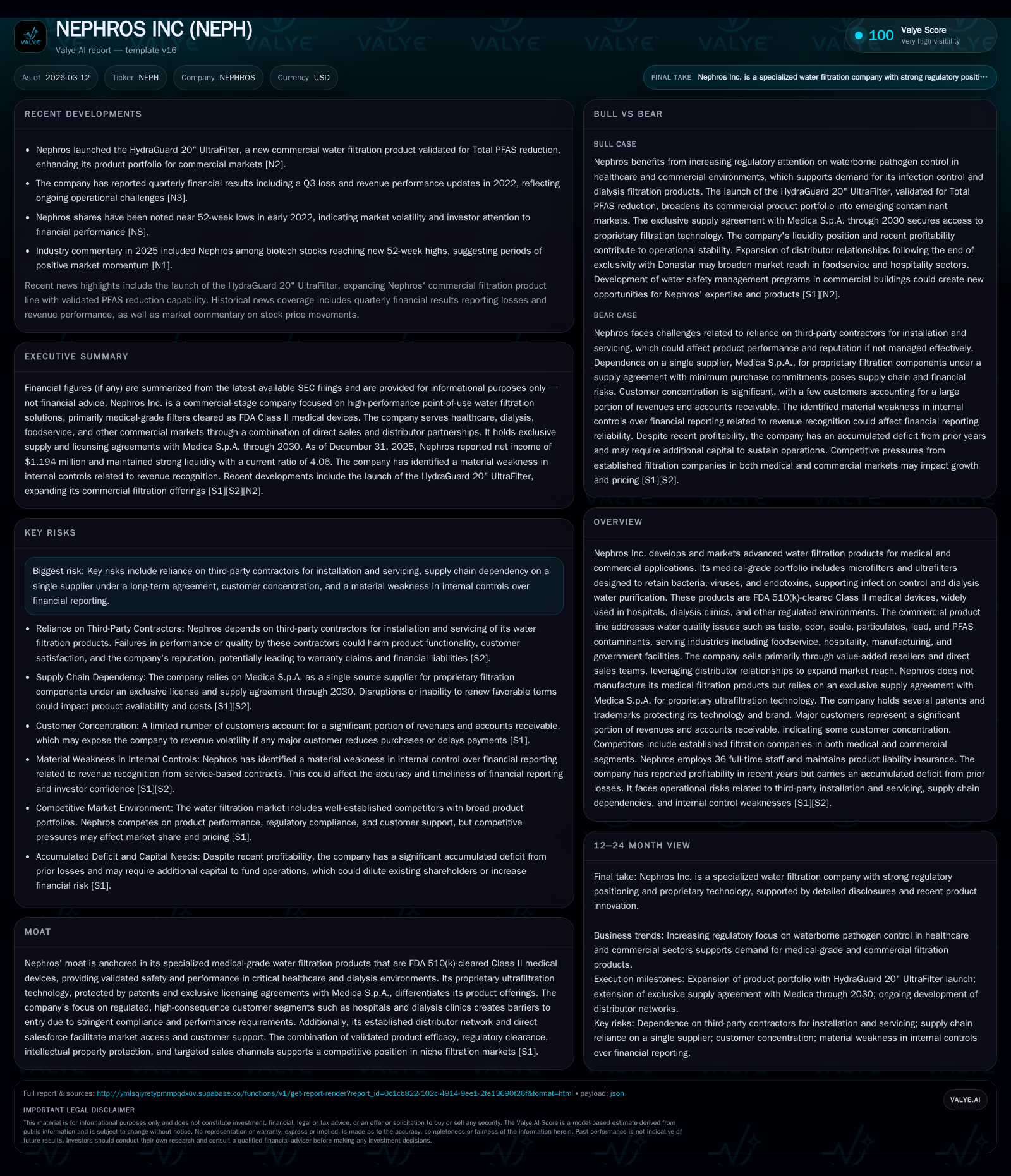

Nephros Inc., a niche player in medical-grade water filtration, has demonstrated a sharp turnaround with profitability in 2024 and 2025 after years of losses, driven by expanded sales and product acceptance in healthcare and commercial sectors. Its proprietary FDA-cleared ultrafiltration technology serves critical healthcare environments but faces growth constraints from reliance on a single European supplier and third-party installers. While new product introductions, including filters validated against PFAS contaminants, signal potential for revenue expansion, risks around supply chain, regulatory compliance, and customer concentration persist. Strong operating cash flow generation alongside modest capital expenditure characterizes its recent financial profile.

Overview and Historical Performance

Nephros Inc. is a specialized developer and marketer of advanced point-of-use water filtration systems focusing primarily on medical-grade applications. Their product line consists mainly of ultrafilters and microfilters that are FDA-cleared Class II medical devices designed to physically remove bacteria, viruses, endotoxins, and other pathogens from water used in healthcare settings like hospitals and dialysis clinics [S1][S5]. The commercial segment addresses broader water quality issues such as taste, odor, scale buildup, particulates including lead and cysts, and recently expanded to include Total PFAS reduction capabilities [S12][S17].

Financially, Nephros has only recently achieved consistent profitability after many years of net losses. Revenue grew from approximately $1.7 million in 2014 to about $3.8 million in 2017 (last available detailed annual data). More significantly, after fluctuating results with a revenue dip around 2023-24 followed by a strong rebound in 2025 (64% revenue increase), the company reported operating income of about $1.15 million and net income close to $1.2 million in 2025—a marked improvement from previous loss-making years [F1]. This operational turnaround was supported by an expansion of their sales team and increasing market acceptance.

Historical performance (annual)

| FY | Net ($) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1194000 | 2 | 1 | 55000 | +1513.5% |

| 2024 | 74000 | 0 | 0 | 55000 | |

| 2023 | 1 | -2 | 75000 | ||

| 2022 | -3 | -4 | 137000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 2 |

| 2024 | -1 |

| 2023 | 1 |

| 2022 | -3 |

Source: SEC companyfacts cache [F1].

(Data for annual revenue not fully available post-2017; operating figures from filings ending Dec each year) [F1]

Product Portfolio and Market Positioning

Nephros’ moat lies heavily in its medically focused product lines cleared by the FDA under the stringent Class II designation that ensures rigorous safety and efficacy standards are met [S1]. Their ultrafilters feature a proprietary polysulfone hollow fiber membrane technology with extremely small pore sizes (down to 0.005 microns) that retain not just bacteria but also viruses and endotoxins—critical for high-risk healthcare environments such as dialysis water systems where ultrapure water is imperative [S5][S17].

The medical segment supports two main use cases: infection control within hospitals to combat pathogens like Legionella or Pseudomonas found in premise plumbing systems; and dialysis water ultrafiltration to remove contaminants from treatment fluids exceeding international ISO standards for dialysate purity [S17][S10].

On the commercial side, Nephros develops filters addressing common water quality issues encountered across foodservice venues (restaurants, convenience stores), hospitality operations (hotels), manufacturing facilities, laboratories, aviation environments, government buildings, and other federal facilities concerned with compliance under regulations such as ASHRAE-188 or the Safe Drinking Water Act [S12][S25]. The recent validation for multi-compound PFAS reduction extends their addressable market into emerging contaminant concerns that are increasingly prioritized by regulators [S17].

Sales are conducted through value-added resellers (VARs), direct sales teams focusing on geographically targeted hospital/dialysis markets, and selective non-exclusive partnerships aimed at commercial sectors previously served under terminated exclusive distribution agreements [S5][S8][S16]. This channel diversity supports scaling opportunities but also introduces execution complexity.

Growth Drivers and Constraints

Future growth depends on several company-specific levers:

- Continued sales expansion within U.S. hospitals embracing water management plans amid rising awareness of healthcare-associated infections linked to waterborne pathogens [S17]. Approximately 6,093 U.S. hospitals with over 900k beds represent a substantial installed base.

- Increasing adoption of ultrafiltration technology integrating Nephros’ filters as standard infection control tools during outbreak responses or proactive installations.

- Geographic expansion into international markets leveraging existing regulatory approvals in Canada and Brazil; however further global rollout requires meeting diverse regulatory regimes which may slow pace [S19][S21].

- Upselling complementary commercial filtration solutions targeting aesthetic contaminants alongside medical grade products expands cross-selling potential.

- Product innovation including enhanced PFAS filtration validated products broadening relevance to schools and federally regulated venues adds incremental market opportunities.

Conversely:

- Reliance on a single Italian manufacturer Medica S.p.A., governed by minimum annual purchase commitments through at least end-2030 creates supply risk if production or contractual terms falter; switching suppliers could be difficult or costly [S22][S21].

- Installation/servicing depend heavily on third-party contractors over whom Nephros holds limited direct control; any lapses could harm reputation via quality failures or increase warranty claims [S2][S4].

- Customer concentration is pronounced with top three customers accounting for nearly half of revenues (44% in 2025), exposing the company to significant demand volatility if key relationships weaken [S7].

- Regulatory compliance remains demanding; failure to maintain FDA clearances or meet evolving quality system regulations poses a risk to market access [S4][S11][S19].

- Tariff uncertainty affecting import costs given materials sourced from the EU adds margin pressure potential [S26][S16].

Financial Forecasts and Milestones to Watch

While no explicit future guidance exists in current disclosures [N#], the key milestones will revolve around sustaining double-digit revenue growth beyond recent gains witnessed through increased market penetration.

In particular:

- Monitoring quarterly revenue trends will reveal if prior gains from salesforce expansions translate into durable customer base increases.

- Maintaining or improving profitability margins hinges on managing manufacturing costs amid inflationary pressures tied to overseas tariffs.

- Success in commercial segment growth beyond legacy medical markets would diversify revenue streams reducing customer concentration risk.

- Progress towards expanding production capacity via Medica or alternate suppliers remains critical given minimum purchase commitments escalating yearly (€4.98M+ range for upcoming years) [S13][S21].

- R&D efforts targeting new filter patents or enhancements contribute both competitively and regulatory-wise.

Returns Profile & Capital Allocation

Nephros’ return metrics reflect its evolving profitability dynamic:

- Approximate Return on Equity for FY2025 stands around 14%, rising strongly due to profitable bottom-line improvement over reduced equity base caused by past accumulated deficits of $143 million at end-2025 [F1][S1].

- Operating cash flow jumped notably to $1.65 million in FY2025 from negative $492k prior year – indicating robust underlying cash generation now supporting operations without liquidity strains.

- Capital expenditures remain minimal ($55k annually), reflecting asset-light model consistent with outsourcing manufacturing primarily overseas save for some local commercial filter production [F1][S22].

- No reported dividends or buyback programs; capital is presumably reinvested for growth initiatives including sales expansion and product development.

Strategic Considerations & Risks

Nephros operates at the intersection of medical device regulation, industrial water quality standards, and proprietary filtration technology protected by a limited portfolio of patents expiring variably till mid-century [S9][S14]. The breadth yet specificity of its patent estate underpin competitive positioning but vulnerabilities exist given patent challenges prevalent within medical device sectors.

Supply continuity facilitated by exclusive licensing with Medica is pivotal yet concentrated – termination or breach scenarios carry outsized consequences including potentially halting product availability impacting reputation and revenues materially [S21]. Investment in supply chain diversification or inventory buffering could be strategic priorities going forward.

Third-party installation service quality remains a latent vulnerability due to indirect control mechanisms; any public incident related to improper installation could degrade customer perception impacting repeat business despite efficacy of the products themselves [S2][S4].

Customer concentration heightens dependency risks: one top customer contributed over one-fifth (~22%) of revenues in both FY24–25 periods while three accounted collectively for nearly half total sales; diversification efforts appear necessary for longer-term resilience [S7].

Regulatory landscape fluctuations domestically within FDA enforcement zones or globally through ISO-compliant certifications will continue requiring resource allocation towards compliance systems maintaining premium market standing especially given Class II device sensitivity [S19].

Finally geopolitical trade tensions focusing on tariff impositions could drive cost escalations sourced from European suppliers threatening margin sustainability absent successful cost-pass-through measures or alternate sourcing alternatives [S16][S26].

Conclusion

Nephros Inc.’s fortified position in medical-grade water filtration is grounded in highly validated ultrafiltration technology meeting rigorous regulatory clearance serving critical healthcare applications alongside expanding commercial usage targeting emerging contaminants such as PFAS. Its fiscal recovery culminating in positive operating results contrasts earlier deficit burdens though concentrated supplier reliance paired with dependence on third-party service providers pose tangible operational challenges. Sustained revenue growth will hinge upon deepening penetration within hospital networks augmented by diversified commercial adoption while safeguarding supply chain integrity under long-term exclusive contracts. Cash flow strength paired with cautious capex deployments indicates financial discipline amidst scaling efforts though customer concentration demands strategic broadening efforts for stable recurring income trajectories.

This analysis is based solely on publicly available information as of March 2026 including SEC filings without projecting unconfirmed data or offering investment opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments