Nevada Canyon Gold Corp. Updates Operating Position with Strategic Exploration Focus

The latest quarterly report underscores Nevada Canyon Gold's early-stage royalty portfolio operations and explores the implications of its exploration-centric business model and financing needs.

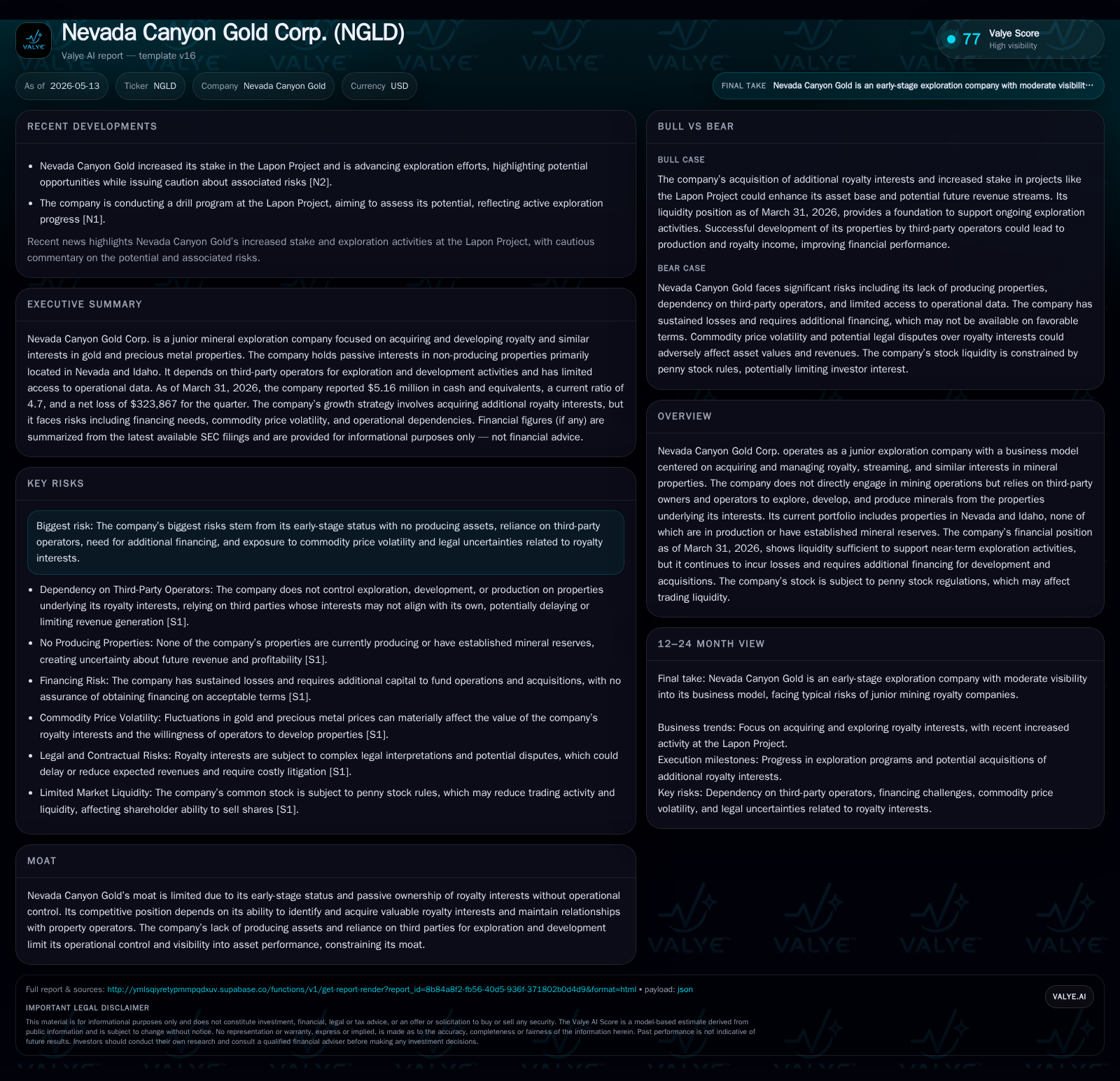

Nevada Canyon Gold Corp.'s May 2026 quarterly filing reveals continued operating losses but sufficient liquidity to sustain near-term exploration. The company's royalty and streaming-focused business model relies on third-party operators without producing assets, presenting challenges in revenue visibility and operational control. Growth hinges on acquiring valuable royalties, advancing exploration through collaboration with operators, and navigating regulatory complexities. Financing requirements and the company's penny stock status temper growth prospects amid commodity price volatility.

Latest Quarterly Operating Update

Nevada Canyon Gold Corp.’s 10-Q filing dated May 13, 2026 paints a picture consistent with a junior exploration company still in the early innings of advancing its royalty portfolio. As of the quarter ending March 31, 2026, the company holds approximately $5.16 million in cash and equivalents, supported by current assets totaling roughly $5.27 million (current ratio ~4.7), sufficient to finance its near-term exploration activities but not enough to support significant development or acquisitions without raising additional capital [S2][F1].

The filing confirms ongoing operating losses in line with its pre-production status—no revenues from producing assets were reported for the quarter, reflecting the company’s lack of operational mines. Nevada Canyon’s financial disclosure reiterates that all mineral property projects remain at the exploration stage with no reserves established yet [S2][F1]. The company continues to manage a portfolio mainly consisting of royalty, streaming, and similar interests across multiple properties located in Nevada and Idaho. These properties are operated by third parties who retain discretion over development timing and scope.

Trading under penny stock rules constrains market liquidity for NGLD shares, which limits financial flexibility and can impact future capital raises via equity issuance — a critical consideration given the company’s reliance on external funding to advance its projects [S2][F1].

Business Model and Asset Quality Overview

Nevada Canyon Gold’s business model hinges on acquiring and managing royalty interests that provide a share of revenue if production occurs on underlying mineral properties, without engaging directly in mining operations itself. This generates a passive income stream contingent upon production volumes realized by third-party operators managing those sites [S1].

This structure reduces operational risk related to mine development but also restricts revenue visibility and timing since Nevada Canyon has no control over operator decisions such as exploration pace or commencement of production that could trigger royalty payments.

Currently, none of the company’s properties produce minerals or hold proven mineral reserves. The early exploration status means that potential returns are speculative and dependent on advancement from discovery through feasibility studies to eventual mine construction — milestones controlled by operators rather than NGLD itself [S1].

This passive investment strategy requires robust due diligence capabilities focused on identifying valuable royalties or streams at attractive terms from resource developers or smaller producers seeking non-dilutive capital via asset monetization.

Competitive Position within the Royalty and Streaming Sector

As a junior royalty holder primarily focused on early-stage assets lacking production or reserve certainty, Nevada Canyon faces intrinsic moat limitations. Its competitive advantage largely derives from sourcing high-quality royalty interests at favorable valuations relative to peers.

However, the company's passive role means it lacks leverage over project economics or timing beyond selecting where to invest or acquire interests. Larger players with broader portfolios or deeper financial capacity can pursue more aggressive acquisitions or negotiate better terms due to scale advantages.

The scarcity of high-potential royalty opportunities combined with competition within the sector presents challenges in expanding NGLD’s portfolio profitably. Without significant operational involvement or barriers to entry in royalty acquisition markets, sustaining differentiation requires persistent deal sourcing acumen alongside strong industry relationships.

Industry Environment: Regulatory and Market Influences

Mining operations connected to Nevada Canyon’s royalties face an evolving regulatory landscape imposing stricter environmental standards, permitting hurdles, and climate-related compliance costs. U.S. Federal statutes such as CERCLA impose liability for environmental damages; state-level regulations add further obligations particularly around water permits (Federal Clean Water Act) and air quality controls.

These regulations increase the cost burden for operators controlling extraction activities underlying NGLD’s royalties — higher compliance expenses can delay project timelines or reduce production scales impacting prospective revenues payable to royalty holders.

Additionally, climate change legislation under discussion or implementation heightens uncertainty around future operational costs for mine operators regionally affecting project economics indirectly impacting Nevada Canyon’s potential income streams [S3][S6].

Commodity pricing volatility remains a significant determinant of operator incentives to explore or produce minerals backing royalties. Fluctuations in gold prices materially affect project feasibility decisions downstream from NGLD’s asset portfolio as well as valuations placed on royalties themselves in acquisition discussions [S19][S23].

Growth Drivers: Opportunities and Milestones

Growth primarily depends on two levers: securing new royalty interests through acquisitions or partnerships enabled by sufficient capital; and witnessing advancement of existing projects operated by third parties progressing toward commercial production.

The company cites an “exploration project accelerator” approach aimed at accelerating discovery drilling programs through selected joint venture arrangements emphasizing faster resource delineation [S1]. Success here elevates probable value realization from properties currently non-productive.

Operator drilling outcomes at flagship projects like Lapon Canyon (in partnership through an Exploration Stream Earn-in Agreement) serve as meaningful KPIs highlighting reservoir potential advances as reported historically via periodic drill result releases issued by Walker River Resources Corp., the project operator [S17][S18][N/A news; item references from SEC filings only].

Higher gold pricing environments would incentivize operators controlling underlying assets to accelerate exploration or ramp up production efforts enhancing royalty revenue prospects while also possibly increasing benchmark valuations for acquiring new royalty properties.

Risks and Constraints Including Financing and Operational Control

A central risk is reliance on third parties over whom Nevada Canyon exerts minimal control regarding development pacing or even continuation of mining activities affecting intermittent or delayed cash flows from royalties—sometimes adverse alignment may exist if operators deprioritize royalty-bearing zones to emphasize non-royalty areas reducing revenue optimism [S1].

Ongoing operating losses necessitate future financing rounds often executed via equity issuances raising dilution concerns for existing shareholders given past capital raises documented in filings. Additionally, turkey share trading under penny stock regulations dampens liquidity complicating timely access to capital at attractive terms [S9][S13].

Legal uncertainties include title disputes over mineral claims underlying royalties; any legal actions required to enforce contractual rights could be expensive with unpredictable outcomes affecting asset values [S5][S14].

Environmental regulation changes imposing higher compliance costs can constrain operator investments thereby impacting associated royalties; delays obtaining permits may also defer revenue realization timelines.

Further competition from larger firms with more financial flexibility limits NGLD's ability to secure premium acquisitions without accepting less favorable terms potentially compromising returns or growth prospects [S10].

Near-Term Watchpoints and Catalysts

Monitoring upcoming quarterly reports remains critical for assessing changes in cash position relative to ongoing losses, progress made on operator-driven drilling programs reflected indirectly through partner disclosures (e.g., Walker River’s updates), new acquisition announcements adding scale or diversification, securing additional financing rounds including debt facilities if any announced under SEC filings [S2][S1].

Regulatory permit approvals clearing pathways for development would be positive signals confirming project advancement feasibility mitigating timing uncertainty risk.

Tracking gold market dynamics is essential given direct impact on operator investment appetite influencing near-to-medium term royalty stream visibility.

Additionally, any shifts in joint venture arrangements altering operator incentives relative to NGLD’s interests would materially affect growth outlooks.

Financial Snapshot: Liquidity, Capital Structure, and Expenses

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5mm | |

| 2026-03-31 | ||

| Current assets | $5mm | |

| 2026-03-31 | ||

| Current ratio | 4.7x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $5.16M | |

| 2026-03-31 | ||

| Total Debt | $0.515K | |

| 2022-12-31 | ||

| Current Ratio | 4.7 | Latest Q |

Nevada Canyon's balance sheet reflects substantial cash buffers relative to negligible debt levels supporting immediate working capital needs for exploration endeavors. However, with operating losses ongoing coupled with absence of producing assets generating revenues, this liquidity suffices only for short-term sustenance of activities without transformational growth initiatives absent fresh capital injections [F1][S2].

Operating expenses align mainly with administration and project evaluation; capital expenditure is modest consistent with no active mining operation expenditures incurred yet but exploratory investments may rise contingent upon financing outcomes.

Disclaimer: This analysis is based solely on information available from SEC filings dated May 13, 2026 ([S2]) plus annual filings ([S1]) and companyfacts data ([F1]). It does not constitute investment advice nor an investment recommendation but aims to provide an informed industry analyst perspective emphasizing facts disclosed by Nevada Canyon Gold Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments