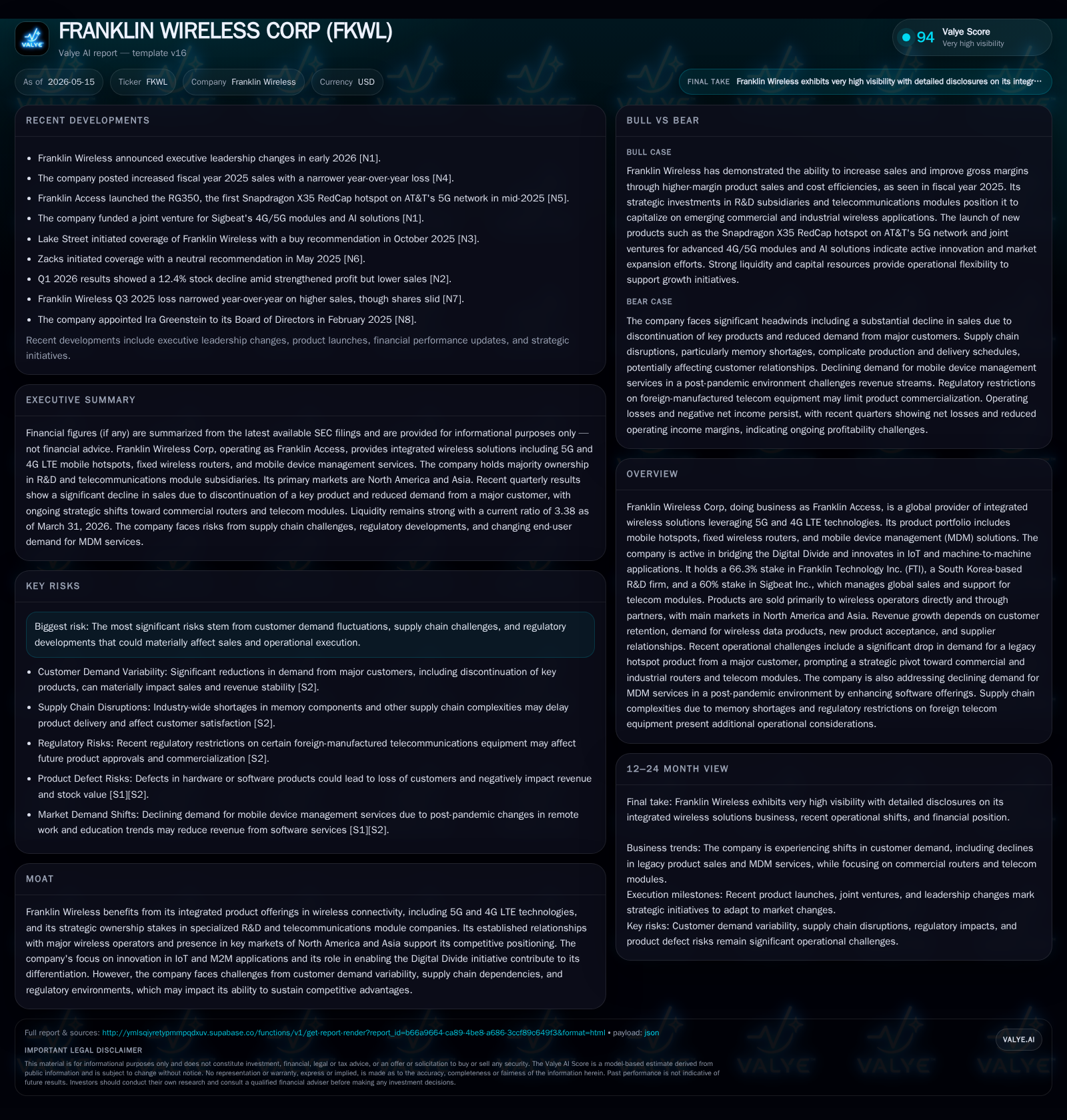

Franklin Wireless Shifts Focus from Legacy Hotspots to Industrial Routers Amid Demand Drop

A sharp decline in legacy hotspot demand prompts Franklin Wireless to accelerate its push into commercial wireless modules and routers.

Franklin Wireless Corp reported a substantial 57% drop in Q3 2026 net sales primarily due to the discontinuation of a legacy hotspot product by a major North American carrier. The company is pivoting toward earlier-stage commercial and industrial wireless routers and telecommunications modules through its subsidiaries. While market demand softness for legacy products is constraining near-term revenue, Franklin benefits from its integrated wireless tech portfolio and strategic R&D ownerships across North America and Asia. Revenue growth now hinges on customer retention, new product adoption, and supply chain stability amid cyclical shifts in customer demand patterns.

Recent Operating Update

Franklin Wireless Corp's latest quarterly filing for Q3 ended March 31, 2026 [S2] shows a significant deterioration in near-term revenues with net sales plunging by 57% YoY to $3.44 million compared to $8.01 million in Q3 2025. This steep decline relates directly to the discontinuation of a key legacy hotspot product by one of its major North American carrier customers, following disputes involving late payments via an intermediary company [S2]. The company does not anticipate material future revenues from this product line moving forward.

Despite the drastic revenue contraction, gross margin percentages remained relatively steady at approximately 16.1% compared to 16.9% last year, though the gross profit dollar amount dropped sharply. This stability suggests that while volume pressure persists, cost controls or a shift towards higher-margin items within other offerings partly offset margin erosion. Operating expenses decreased by approximately 38%, aligning expense structure to correspond with reduced sales activity [S15].

Notably, management has accelerated strategic initiatives focusing on commercial and industrial routers along with telecommunications modules through subsidiaries like Sigbeat Inc., although these segments are still in early commercialization stages with uncertain timing for meaningful revenue contributions [S2]. The recent appointment of Bill Bauer as Chief Operating Officer signals an internal push to strengthen operational capabilities during this transformation [S3].

Business Model

Operating under the brand Franklin Access, Franklin Wireless provides integrated wireless connectivity solutions combining hardware devices such as mobile hotspots and fixed wireless routers with mobile device management (MDM) software services. These products leverage leading-edge cellular technologies including 5G and 4G LTE tailored for both consumer mobility scenarios and expanding enterprise IoT/M2M ecosystems [S1][S2].

Revenue generation primarily comes from contracts directly with large wireless carriers who deploy these devices or indirectly through channel partners and distributors operating largely in North America and Asia. These carriers procure devices under purchase orders specifying quantities and pricing within contract frameworks governed by ASC 606 revenue recognition standards [S1]. Customer retention among these large accounts remains critical since losing or scaling back business can drastically affect top-line performance—as witnessed recently.

Franklin’s strategic ownership stakes—66.3% in Franklin Technology Inc., a Seoul-based R&D entity responsible for product design innovation, and 60% in Sigbeat Inc., charged with worldwide sales/support for telecom modules—provide crucial downstream integration in its value chain [S1][S2]. This collaborative ecosystem enables closer coordination between product development cycles, market feedback channels, distribution logistics, and technical support functions.

The demand dynamics appear increasingly structural: post-pandemic declines in remote work/school have reduced MDM needs while the volatility associated with legacy hotspot models highlights customers’ preference shifts toward more robust industrial router solutions supporting IoT expansions [S1][S2]. This evolution necessitates Franklin’s pivot toward newer commercial products even as it manages shrinking legacy footprints.

Industry Structure and Competitive Position

The wireless connectivity market is segmented broadly among consumer mobile device manufacturers offering hotspots/routers for personal use; telecom equipment providers focusing on fixed network infrastructure; and specialists like Franklin addressing niche commercial IoT/M2M applications bridging cellular technology with edge device management capabilities.

Franklin’s competitive advantage lies in its vertically integrated approach combining hardware innovation (via FTI), embedded module expertise (through Sigbeat), and comprehensive end-customer support backed by longstanding relationships with major North American carriers. This integration creates some switching costs given the bundled nature of offerings across device lifecycle management.

However, competition remains intense due to rapid technology cycles with entrants leveraging commoditized chipsets from giants like Qualcomm alongside cloud-centric software platforms increasingly converging network management layers. Also, supply chain fragility affects component sourcing reliability post-pandemic—a challenge Franklin acknowledges given their reliance on manufacturing partnerships [S1][S2]. Regulatory considerations tied to emerging wireless standards also present regional compliance burdens.

Growth Drivers

Key growth vectors include:

- Commercialization Expansion: The company's renewed emphasis on industrial-grade wireless routers targeting enterprises aiming for secure reliable connectivity supports digital transformation initiatives within logistics, manufacturing automation, smart cities, and energy sectors.

- IoT & M2M Innovation: Leveraging advancements developed at FTI for low-power wide area network compatibility taps into accelerating deployments requiring scalable device fleets under unified asset visibility platforms.

- New Customer Acquisition: Opening additional accounts beyond existing major carriers diversifies revenue sources while reducing concentration risk from individual customers.

- Product Portfolio Evolution: Introducing next-generation modules enabling seamless transitions between cellular generations (4G to 5G) enriches solution relevance amid ongoing network upgrades worldwide.

- Geographic Market Penetration: Deepening presence within Asian markets where wireless infrastructure spending remains robust complements the dominant North American base.

These growth aspects depend heavily on timely execution of R&D projects—to maintain technological parity or superiority—and successful integration of sales/support efforts managed via Sigbeat’s global operations.

Risks / Watchpoints / Growth Constraints

Primary risks include:

- Customer Demand Volatility: Recent loss of legacy hotspot revenue underscores sensitivity to contractual interruptions or inventory adjustments among few large customers.

- Supply Chain Dependencies: Fluctuating component availability could delay product launches or inflate production costs impacting margins.

- Product Quality Issues: Hardware/software defects risk damaging client trust potentially triggering order cancellations or warranty liabilities.

- Regulatory Compliance: Evolving telecom standards across jurisdictions may require continuous adaptation posing cost and timing uncertainties.

- Market Adoption Timing: Early-stage industrial router markets are nascent; uncertain adoption curves may delay anticipated revenue ramp.

- Financial Sustainability: Although current liquidity is healthy ([F1] cash & equivalents >$14 million as of September 2024; no debt), extended operational losses without faster commercialization might pressure resources requiring capital raises or restructuring.

What to Watch Next

Critical milestones include:

- Quarterly updates quantifying early commercial traction for industrial routers and telecom modules beyond pilot phases.

- New customer contract announcements signaling widening acceptance outside traditional large carriers.

- R&D pipeline disclosures detailing breakthroughs aligned with next-gen connectivity standards critical for IoT platforms.

- Operational metrics showing stabilization or growth in mobile device management services amid changing user trends.

- Cash flow developments showing improvement as inventory levels normalize following recent write-offs detailed in filings [S21].

- Further clarity on supply chain normalization affecting production lead times/costs will be instructive.

- Management guidance revisions that may reset expectations reflecting strategic pivots announced recently.

Monitoring these indicators will shed light on the durability of Franklin's repositioning strategy under volatile industry conditions.

Financial Profile (Latest Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $45mm | |

| 2026-03-31 | ||

| Current liabilities | $13mm | |

| 2026-03-31 | ||

| Current ratio | 3.38x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

*No current debt reported implies negligible leverage enabling financial flexibility [F1].

The company maintains strong liquidity with cash reserves sufficient for ongoing operations over at least the near term according to management commentary [S21]. Operating cash flow turned negative by approximately $5.56 million over nine months ended March 31, 2026 due mainly to increasing inventories required for new product lines—highlighting execution investment phase [S21].

Franklin Wireless Corp stands at an inflection point transitioning away from declining legacy hotspots toward future-facing industrial connectivity products crucial for burgeoning digital infrastructure requirements globally. Its integrated business model backed by proprietary R&D capabilities equips it strategically well but execution risks remain elevated amid competitive pressures and volatile customer demand patterns. Vigilant monitoring of emerging commercial revenues alongside cost disciplined operations will be essential to validating sustainable growth prospects going forward.

Disclaimer: This analysis is based solely on disclosed SEC filings and publicly available data as of May 15, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments