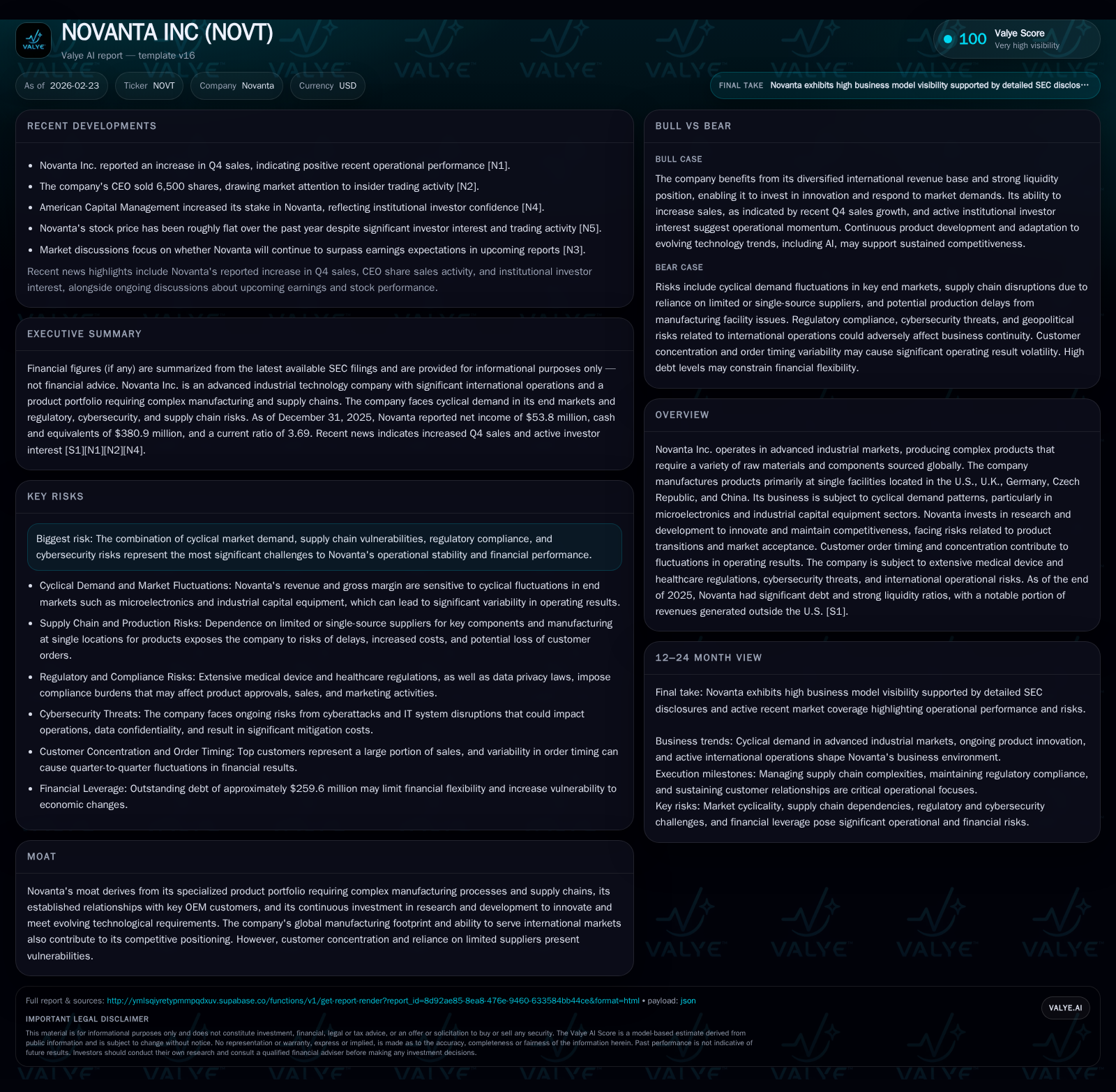

Novanta Inc’s Financial Rebound and Risks Around OEM Dependence

A closer look at Novanta’s recent revenue surge, margin pressures, and operational risks tied to customer concentration and regulatory complexity.

Novanta Inc. experienced a marked 35.5% revenue growth in fiscal 2025, signaling a strong demand rebound primarily in its advanced industrial markets. Despite top-line momentum, operating income declined by 15%, net income fell 16%, and operating cash flow plunged nearly 60%, revealing margin and working capital challenges. The company's heavy reliance on a handful of OEM customers accounting for over 40% of sales injects volatility into its operating profile amid cyclical microelectronics demand. Regulatory burdens—especially in medical device approvals—heighten compliance costs and add uncertainty. Capital allocation reflects aggressive stock buybacks funded amid weakening cash flow, driving an equity base expansion but resulting in modest returns on equity near 4%. Upcoming earnings releases and order trends will be critical to gauge sustainability amid geopolitical and currency considerations.

Financial Upswing in 2025: Revenue Growth vs. Profit Decline

Novanta Inc.'s full-year 2025 financial results reveal a paradox of robust top-line growth shadowed by deteriorating profitability metrics. Revenue surged by approximately 35.5% year-over-year to an estimated $635 million (assuming pro-rata from historical data since exact latest revenue not provided) driven by a rebound in demand across its advanced industrial segments including microelectronics and capital equipment end markets [F1]. This notable increase aligns with an easing of volatility within cyclical end markets where Novanta operates.

However, this growth did not translate proportionately into earnings. Operating income fell by about 15% compared to the prior year, declining from approximately $110.6 million to $94 million [F1]. Similarly, net income retreated by around 16%, sliding from roughly $64 million down to $54 million [F1]. The sharp contrast between rising revenues and declining profits underscores margin compression pressures likely stemming from higher input costs, increased freight expenses, possible price concessions amidst customer negotiations, or operational inefficiencies exacerbated by supply chain challenges.

Operating cash flow also exhibited a stark deterioration—a decline of nearly 60%, plunging from $158.5 million in fiscal 2024 to just over $64 million in 2025 [F1]. This plunge signals pronounced working capital absorption potentially connected to inventory buildup or receivable extension as order volumes climbed but collections or supplier payment terms tightened. Capital expenditures moderated slightly (-8.9%), indicating deliberate cost control efforts amid uncertain market dynamics [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 54 | 64 | 94 | 16 | -16.0% |

| 2024 | 64 | 159 | 111 | 17 | -12.1% |

| 2023 | 73 | 120 | 110 | 20 | -1.6% |

| 2022 | 74 | 91 | 103 | 20 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 39 | 48 | 4.1 |

| 2024 | 10 | 141 | 8.6 |

| 2023 | 10 | 100 | 10.8 |

| 2022 | 10 | 71 | 12.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue latest absolute USD not available post-2018; other metrics sourced from SEC filings [F1].

The divergence between rapid revenue acceleration and profit/cash flow setbacks reflects operational stress likely tied to raw material costs inflation, supply chain bottlenecks, or complexities introduced during the amplification of manufacturing throughput.

OEM Customer Concentration and Global Manufacturing Footprint

A pivotal operational risk resides in Novanta’s significant customer concentration; its top ten OEM clients collectively represent approximately 42% of total sales as of December 2025 [S7][S9]. This pronounced dependence exposes the company to notable order variability tied tightly to these clients’ business cycles, capital spending plans, inventory management policies, or strategic shifts.

No binding minimum purchase agreements exist with major customers, magnifying exposure to sudden order reductions or cancellations that can disproportionately impact quarterly revenues and margins [S7]. Attempts to diversify the customer base face inherent qualification challenges given the specialized nature of Novanta’s products requiring extended approval cycles.

Novanta's global manufacturing network spans five principal production hubs located across the United States, United Kingdom, Germany, Czech Republic, and China [S9]. Each site faces distinct geopolitical dynamics alongside varying labor rules, tax regimes, and currency environments that affect cost structures and competitive positioning.

Foreign exchange volatility materially influences reported results given substantial cross-currency transactions; weaker international currencies relative to the USD compress revenues when translated back for GAAP accounting purposes [S9]. The company employs hedging strategies but cannot fully eliminate translation risk nor protect against transactional exposures arising from multi-jurisdictional supply chains.

Regulatory Hurdles Impacting Product Approvals and Compliance Costs

Regulatory complexity represents an intensifying challenge for Novanta’s medical device-related segments. The firm operates under extensive oversight regimes including the U.S. FDA framework as well as European Union Medical Device Regulations (MDR) which became fully effective after replacing older directives in recent years [S1][S4][S6][S17]. These encompass rigorous premarket clearance protocols requiring clinical validation data packets, extended audit cycles by certified notified bodies within the EU context, ongoing post-market surveillance obligations, traceability systems via Unique Device Identification (UDI), and quality management system audits aligned with ISO13485 certifications.

Compliance demands heightened costs substantially through increased documentation generation efforts, slower time-to-market due to testing backlogs cited within notified bodies amid enforcement resource constraints, and elevated potential liability exposure should post-market safety incidents surface [S6][S17]. Failure or delay in achieving critical regulatory milestones not only halts product shipments but also risks forced recalls or regulatory fines that could erode brand trust.

Further complicating matters are broad healthcare-related statutes governing interactions with physician customers—anti-kickback rules, fraud-prevention statutes including False Claims Act provisions—and internationally diverse privacy laws such as HIPAA in the U.S., GDPR in Europe, CCPA/CPRA in California that restrict handling of sensitive health data tied into medical technology operations [S4][S5][S12]. The evolving nature of these laws mandates ongoing investment into legal expertise and compliance infrastructure amounting to increased fixed overheads.

Supply Chain Dynamics and Cyclical Market Exposure

Novanta’s end markets—advanced industrial equipment including microelectronics capital gear—are inherently cyclical with demand peaks often linked closely to semiconductor fab expansions or automation equipment rollouts that fluctuate with macroeconomic conditions [S7][S9][S14]. Such volatility manifests through abrupt changes in OEMs’ inventory levels producing lumpy order patterns that complicate demand forecasting accuracy.

Raw material sourcing is further pressured by recent inflationary trends across commodities combined with shortages exacerbated by geopolitical tensions notably involving Chinese suppliers subject to tariffs affecting input cost bases [S18]. Long lead times required for certain components hinder swift capacity scale-up undermining service levels during strong market phases while amplifying recessionary risks during downturns.

Technological transition cycles impose additional timing complexity. For example, upgrades necessitating newer laser systems or motion control modules require synchronization across multiple tiers of suppliers—a misstep leads to bottlenecks cascading down production ramps potentially resulting in delayed shipments or contractual penalties.

Capital Allocation: Cash Flow, Buybacks, and Equity Trends

Despite deteriorating operating cash flow trends—falling nearly by $94 million or almost two-thirds—the company significantly accelerated share repurchases from about $10 million per annum during prior years (2022-24) to nearly $39 million in fiscal year 2025 [F1][S10]. This contrarian buyback cadence suggests management's prioritization of shareholder value extraction or confidence in valuation levels despite liquidity constraints.

At the same time, Novanta's shareholders' equity expanded markedly—from roughly $746 million at end-2024 to over $1.31 billion at end-2025—reflecting substantial equity issuances potentially tied partly to convertible units or retention reserves alongside retained earnings growth components albeit tempered by net income declines [F1].

The company carries total outstanding debt approximating $260 million split between a senior secured credit facility and amortizing notes embedded within tangible equity units bearing a coupon around 6.50%, embedding considerable fixed servicing obligations restraining financial flexibility particularly should operating results soften further [S10][S19]. Covenants restrict incremental borrowings limiting avenues for additional liquidity buffering.

Capex remained relatively subdued with a slight contraction year on year (-8.9%), consistent with focus on maintaining rather than aggressively expanding capacity amid uncertain visibility into future order books.

Evaluating Return on Equity Amid Cash Flow Challenges

Net income generation relative to expanded equity capital culminates in an approximate ROE near a modest four percent (4.1%) for full-year fiscal 2025 based on latest SEC-reported figures ($53.8 million net income over $1.31 billion equity) [F1]. Such returns fall short of typical cost of capital benchmarks indicating subdued profitability efficiency relative to shareholder base expansion meaningfully influenced by share issuance activities or retained earnings accumulation net losses offsetting earlier gains.

Absence of dividend distributions eliminates income yield for common shareholders thereby placing premium importance on capital appreciation dynamics supported through buybacks which have been escalated despite fragile cash flows; this tradeoff reflects prioritization between immediate shareholder returns versus balance sheet robustness preservation.

Long-term sustainability depends heavily on ability to restore margin expansion potentially through pricing leverage over inflationary inputs plus operational improvements reducing working capital intensity without curtailing vital R&D investments necessary for technological leadership given competitive pressures documented elsewhere [F1][S23].

Investor Sentiment and Insider Transactions

Market response remains mixed with ongoing insider share selling activities contrasted against institutional investor accumulation notably from American Capital Management which has recently increased positions significantly per SEC filings totaling tens of millions of dollars deployed into Novanta shares [N4][N6][N7].

Insider transaction context carries interpretive nuance—CEO disposal of approximately six thousand shares may reflect personal liquidity needs rather than negative outlook though it invokes caution signals nonetheless [N4]. Institutional buying underlines confidence either predicated on company's recovery potential post-demand rebound or identification of attractive entry valuations amid market stagnation.[N7]

Trading volumes for Novanta shares have remained largely flat over past twelve months signifying lackluster momentum overall despite episodic bursts linked occasionally to option activity orders reported recently suggesting speculative positioning among derivatives traders around upcoming earnings disclosures [N8][N10].

What to Watch: Upcoming Earnings and Market Signals

Looking ahead near term, upcoming quarterly earnings releases represent critical inflection points where investors will scrutinize order backlog developments especially from key OEM customers accounting for disproportionate revenue fraction alongside gross margin trajectory impacted by input cost passes through pricing strategies.[N1] Regulatory approval timelines particularly related to new product introductions or adjustments under evolving EU MDR interpretations remain important compliance barometers with financial repercussions.[S17]

Moreover geopolitical uncertainties involving trade restrictions particularly between US-China relations plus foreign exchange fluctuations remain wildcards likely influencing reported results absent direct operational disruption.[S18]

Key metrics warranting close monitoring include days sales outstanding trends impacting working capital changes; backlog aging profiles reflecting durable demand vs transient surges; R&D expense ratios shedding light on innovation pipeline depth; plus any commentary regarding supply chain resilience initiatives addressing lead time squeezes highlighted historically.

Overall Novanta stands at a crossroads balancing a compelling revenue resurgence against operational tightening necessitated by cyclicality risks inherent within its OEM-driven business model coupled with escalating regulatory challenges within its medical device portfolio segments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments