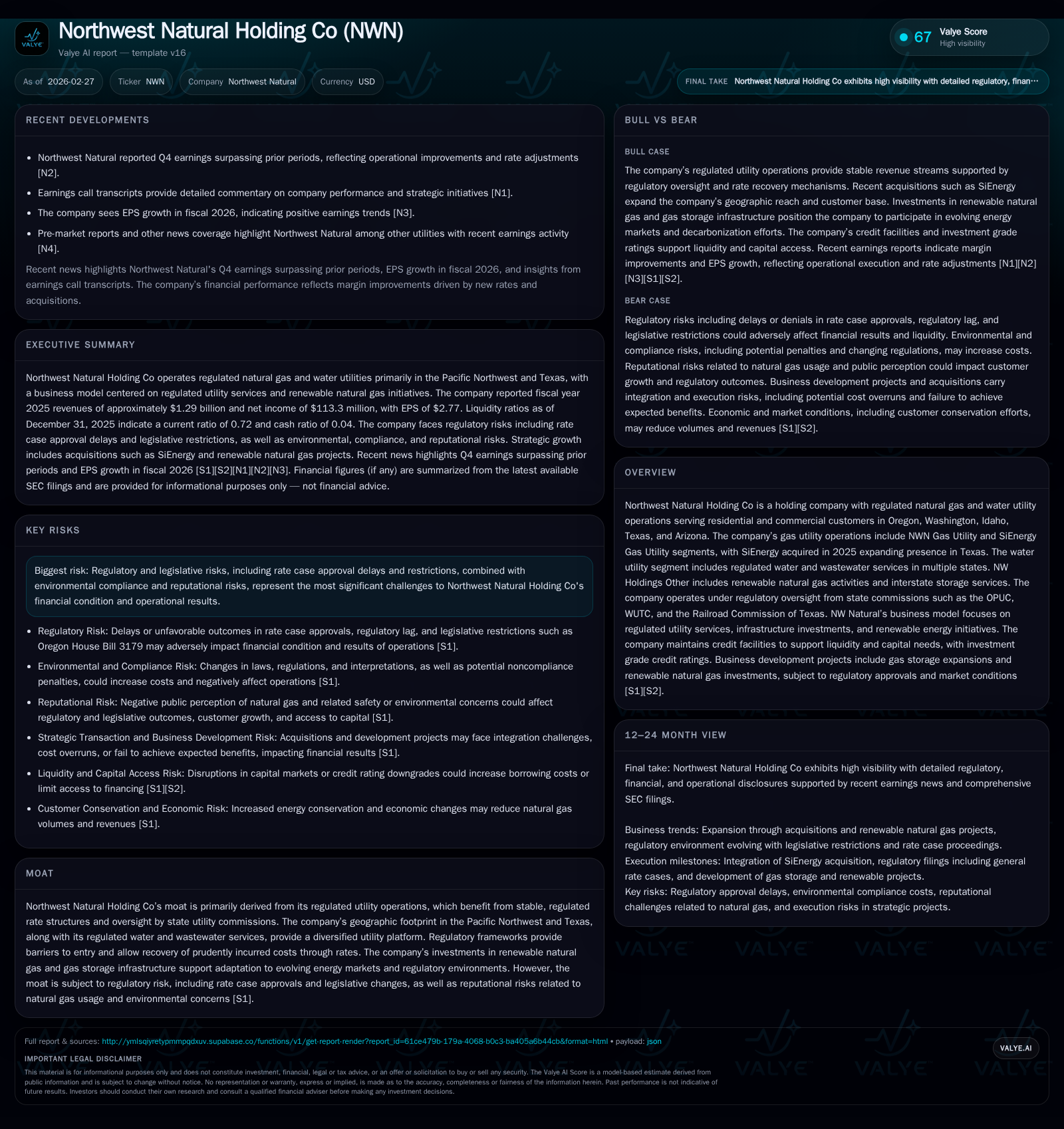

Northwest Natural Holding Co’s 2025 Growth Fueled by Texas Expansion and Infrastructure Investment

A combination of acquisition and regulatory-driven rate increases propelled annual revenue and operating income double-digit growth in 2025.

Northwest Natural Holding Co (NWN) delivered significant financial improvement in 2025 primarily due to the strategic acquisition of SiEnergy, which expanded its footprint into Texas. Regulatory approvals for rate increases in existing territories also contributed to margin enhancement. While capital expenditures intensified, reflecting ongoing infrastructure investment aimed at system safety and renewable natural gas projects, free cash flow remained negative due to elevated capex. The company’s regulated utility business model anchors its moat through stable rate structures and regulatory oversight, though risk factors include regulatory delays, environmental compliance costs, and evolving policy risks. Going forward, growth hinges on integration of new assets, regulatory approvals for infrastructure expansions such as the North Mist gas storage facility, and balancing environmental investments against rate recovery frameworks.

Historical Performance: Revenue Growth Anchored by Acquisition and Rate Increases

Northwest Natural Holding Co reported consolidated revenues of approximately $1.29 billion for fiscal year 2025, up nearly 12% from $1.15 billion in 2024 [F1]. This increase was driven largely by the acquisition of SiEnergy in January 2025 expanding NWN's footprint into key Texas markets as well as regulatory-approved rate increases effective November 2024 in Oregon and Arizona [S2][S16].

Operating income grew markedly by 47% year-over-year to roughly $281 million from $191 million in 2024 [F1], reflecting margin expansion at legacy Oregon-Washington gas utilities alongside contributions from newly acquired SiEnergy operations regulated by Texas authorities. Net income rose approximately 44% to $113 million compared with $78.9 million the prior year [F1].

Capital expenditures accelerated to about $467 million in 2025, an increase of over 18% compared to prior year levels. These investments were focused on pipeline safety improvements, distribution system replacements consistent with evolving state mandates, water infrastructure upgrades across multiple states including Arizona where new rates became effective November 2024, as well as renewable natural gas development projects [F1][S16].

Operating cash flow increased significantly to approximately $269 million in 2025 from $200 million in the prior year; however free cash flow remained negative at around -$198 million due to elevated capex levels characteristic of this investment phase for expanding asset bases within regulated utilities [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1289 | 113 | 269 | 281 | +11.8% | +43.7% |

| 2024 | 1153 | 79 | 200 | 191 | -3.7% | -16.0% |

| 2023 | 1197 | 94 | 280 | 185 | +15.4% | +8.8% |

| 2022 | 1037 | 86 | 148 | 167 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 77 | -198 | 7.7 |

| 2024 | 73 | -194 | 5.7 |

| 2023 | 67 | -47 | 7.3 |

| 2022 | 63 | -191 | 7.3 |

Source: SEC companyfacts cache [F1].

Note: Share buybacks have not been recorded post-2019 according to available data [F1]

Business Model and Moat: Regulatory Underpinnings Support Stability

NW Natural operates primarily within regulated utility segments overseen by multiple authorities including the Oregon Public Utility Commission (OPUC), Washington Utilities and Transportation Commission (WUTC), Railroad Commission of Texas governing new acquisitions like SiEnergy, as well as federal regulation through FERC for interstate storage services [S1][S14]. This framework supports stability via tariff structures that enable recovery of prudently incurred expenses plus authorized returns on invested capital.

Geographically diversified across Pacific Northwest states plus Texas through recent acquisition, NWN mitigates jurisdictional regulatory risk while benefiting from weather normalization mechanisms primarily in Oregon that help manage volume variability related to conservation trends; however such protections are less prevalent outside Oregon impacting revenue stability elsewhere including water utility segments [S14][S19][S22].

The company is actively investing in renewable natural gas initiatives aligned with decarbonization policies where regulators permit cost recovery through expanded asset bases or deferral mechanisms [S20]. The North Mist underground storage expansion project (~4-5 Bcf capacity increase) exemplifies strategic infrastructure growth subject to permitting and customer approvals.

Risks: Regulatory Delays and Environmental Compliance Costs Remain Key Challenges

NW Natural faces ongoing exposure to regulatory outcomes where delays or disallowances in rate case approvals can create timing mismatches between incurred expenses (capex/opex) and recovered revenues impacting earnings predictability [S14][S18]. Environmental regulations may necessitate costly remediation or system upgrades subject to prudence reviews that could limit full cost recovery thereby affecting future profitability [S15].

Broader reputational risks tied to fossil fuel usage amid rising scrutiny could influence legislative changes affecting allowed returns or operational freedoms creating a complex market context ahead [S24][S26][N11]. Operational risks also persist around pipeline integrity events or counterparties within natural gas reserve arrangements requiring ongoing risk management focus [S25].

Customer growth is sensitive to macroeconomic conditions including housing starts which remain below historical norms in core territories potentially constraining new customer additions unless offset by geographic expansion or commercial activity growth [S19][N11].

Capital Allocation: Balancing Infrastructure Investment with Shareholder Returns

NW Holdings maintains ample liquidity backed by credit facilities totaling approximately $725 million across NW Holdings, NW Natural Gas Company, and SiEnergy Holdings entities supporting general corporate purposes including commercial paper program backstops . Interest rates under these facilities vary with credit ratings but no material covenant breaches were reported.

The Board authorized a new share repurchase program permitting up to $150 million in buybacks replacing a smaller prior authorization; however no repurchases occurred during recent quarters indicating capital prioritization toward business investment amid prevailing market conditions [F1][S13]. Dividend payments continue steady growth with approximately $77 million distributed during fiscal year 2025 underscoring commitment to shareholder returns balanced alongside capex demands.

Future Growth Prospects: Integration Execution and Project Approvals Are Pivotal

Successful integration of SiEnergy offers potential for top-line growth through access to high-growth Texas markets while leveraging operational synergies though realization depends on managing integration costs without material attrition or competitive pressures undermining margin expansion [N1][N12][S2].

Infrastructure projects such as the North Mist storage expansion depend on securing permits and customer approvals before becoming financially accretive; delays or denials pose execution risks limiting near-term upside potential [S20][N11].

Renewable natural gas ventures align strategically with energy transition goals but face uncertainties related to technology adoption pace and evolving regulator acceptance regarding cost recovery treatment which may impact earnings visibility until projects scale.

What To Watch: Rate Case Outcomes & Regulatory Momentum On Environmental Initiatives

Investors should monitor timely regulatory approvals ensuring authorized margins reflect inflationary pressures plus investments needed for safety/environmental compliance.

Progress on renewable natural gas initiatives alongside public policy shifts affecting natural gas demand patterns warrant close attention.

Liquidity metrics require observation given negative free cash flow amid heavy capex phases though current revolving credit facilities provide a buffer.

Disclaimer:

This analysis is based solely on publicly available data without offering investment advice or recommendations concerning Northwest Natural Holding Co securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments