Orchestra BioMed Advances Novel Hypertension and Artery Disease Therapies with Strategic Partnerships

The latest quarterly report highlights clinical trial milestones and partnership-enabled development progress for Orchestra BioMed’s cardiovascular innovation pipeline.

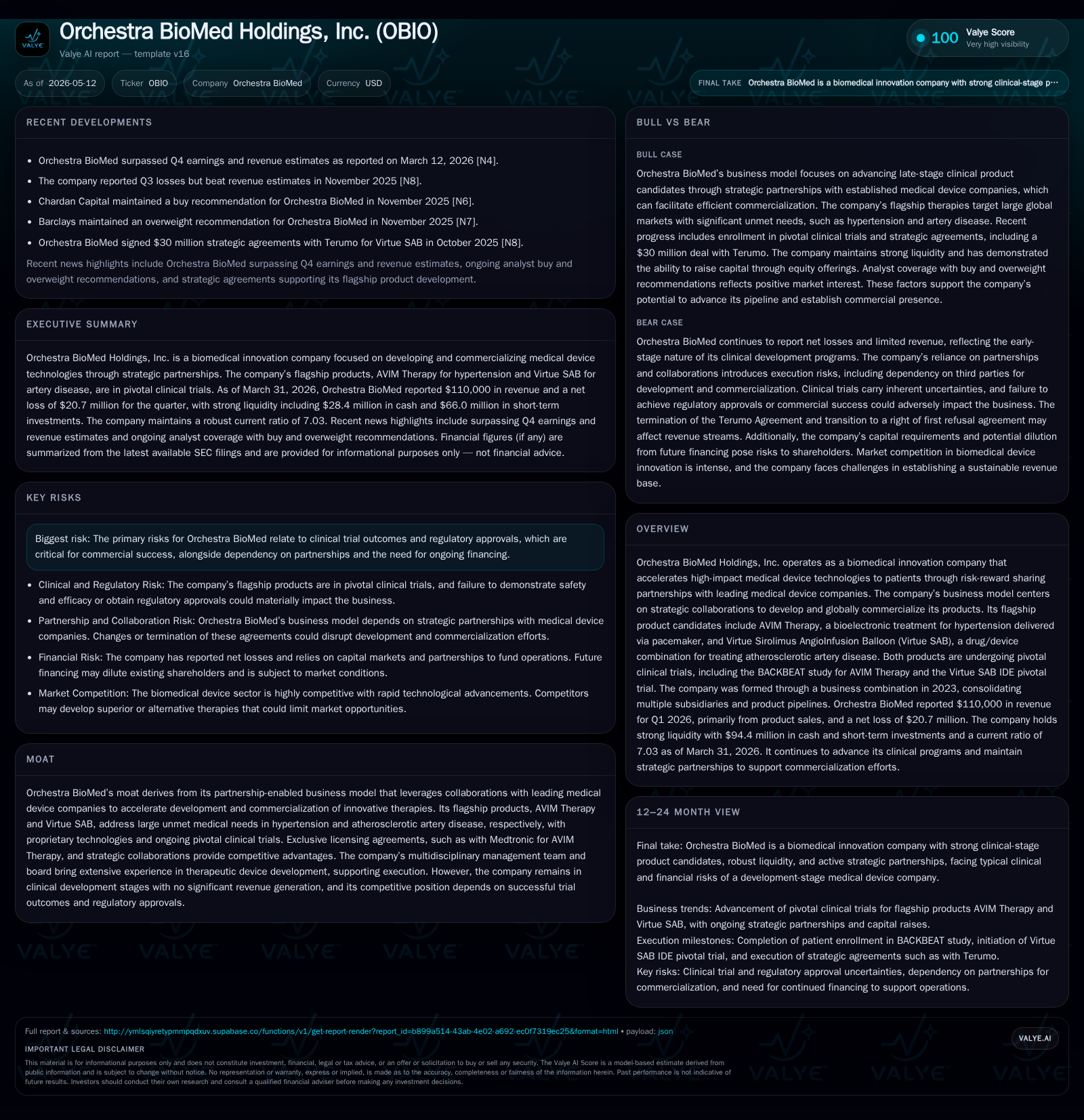

Orchestra BioMed’s Q1 2026 update evidences ongoing enrollment in pivotal trials for two flagship therapies addressing hypertension and coronary artery disease. The company’s risk-sharing business model with leading device partners underpins its development and commercialization strategy. Near-term growth catalysts center on BACKBEAT trial completion mid-2026 and Virtue SAB enrollment through mid-2027. While financial resources remain sufficient for the short term, clinical outcomes and regulatory approvals present key uncertainties for future success.

Latest Quarterly Operating Update and Clinical Progress

Orchestra BioMed's most recent quarterly filing dated May 12, 2026 [S2] reveals measured operational advancement anchored on ongoing clinical development. The company is progressing enrollment in its pivotal studies critical for key product approvals. Specifically, the BACKBEAT study — a global double-blind, randomized pivotal trial assessing AVIM Therapy in patients indicated for Medtronic dual-chamber pacemakers with uncontrolled hypertension — aims to enroll up to 500 patients with mid-2026 anticipated enrollment completion [S1]. Concurrently, the Virtue SAB IDE pivotal trial has initiated U.S.-based enrollment comparing the company's patented drug/device combination balloon against Boston Scientific's AGENT™ drug-coated balloon in roughly 740 patients suffering coronary in-stent restenosis, targeting mid-2027 enrollment completion [S1].

Financially, Orchestra BioMed reported around $33.5 million in revenue during 2025 [F1], driven mainly by product sales from its subsidiary FreeHold Surgical rather than its investigational cardiovascular devices which remain pre-commercial. Operating expenses reflect substantial investments into late-stage clinical trials: R&D costs escalated consistent with larger trials' size and complexity, alongside increased selling, general & administrative expenses linked to public company operations [S10], [S9]. Notably, net interest expense rose relative to prior periods due to loan interest offsetting marketable securities income [S10].

Business Model and Therapeutic Portfolio

Orchestra BioMed employs a partnership-centric business model that accelerates medical device innovation via strategic risk-reward sharing agreements with established medical device firms [S1]. This approach spreads development risk while accessing partners' commercialization capabilities. The company's foundation rests on consolidating several subsidiaries since formation in 2018, assembling a suite of late-stage clinical candidates focused on large unmet cardiovascular needs.

Its two flagship candidates exemplify this strategy:

AVIM Therapy delivers bioelectronic treatment for hypertension through firmware integrated into standard dual-chamber pacemakers—targeting the >70% hypertensive subset among pacemaker-indicated patients. This method potentially offers immediate and sustained blood pressure reduction without implanting additional hardware [S1]. Exclusive licensing with Medtronic secures rights for development/commercialization in pacemaker-indicated uncontrolled hypertension cases [S1].

Virtue Sirolimus AngioInfusion Balloon (Virtue SAB) combines a drug-device platform that administers an extended-release sirolimus formulation directly to arterial walls during angioplasty without permanent implants like stents. It's designed to treat atherosclerotic artery disease by reducing restenosis risk more effectively than existing coated balloons [S1], representing a novel delivery modality amid competitive interventional cardiology solutions.

Such proprietary therapeutics are distinct from traditonal pharmaceuticals or existing devices by leveraging integration with electrophysiology hardware (AVIM) or proprietary drug delivery fabrics (Virtue SAB), enhancing potential efficacy and adoption barriers for competitors.

Competitive Environment and Industry Dynamics

In the hypertension space targeted by AVIM Therapy, incumbent standards rely heavily on pharmacotherapy supplemented by device-based neuromodulation treatments in limited subsets. Orchestra's partner exclusivity through Medtronic enhances technological moat against direct competition given Medtronic's entrenched position in cardiac implantable electronic devices (CIEDs) [S1]. However, widespread adoption hinges upon favorable data from BACKBEAT evidencing superior blood pressure control alongside acceptable safety profiles.

In coronary artery disease interventions where Virtue SAB competes, established agents like Boston Scientific’s AGENT™ drug-coated balloon dominate market share [S1]. Orchestra challenges this incumbency via differentiated sirolimus delivery without polymer coatings or implants potentially improving vessel healing while minimizing long-term foreign body risks. Regulatory hurdles remain significant as FDA approval demands robust randomized clinical evidence amidst a crowded interventional cardiology device ecosystem.

The industry broadly faces capital intensity driven by long development cycles averaging multiple years per device indication, coupled with intricate FDA pathways requiring expansive safety/efficacy data sets. Orchestra’s alliance-based model mitigates some commercial execution risks but maintains dependency on partner collaboration quality and timelines.

Growth Catalysts and Clinical Milestones

Principal growth drivers revolve around near-to-medium term clinical execution:

- BACKBEAT Study Enrollment Completion: Achieving the full cohort of approximately 500 patients expected by mid-2026 represents a gating milestone toward primary endpoint analyses critical for FDA submissions [S2]. Positive outcomes could unlock broader use cases beyond pacemaker-indicated cohorts.

- Virtue SAB Pivotal Trial Enrollment: Initiated recently with target completion of about 740 U.S. patients slated for mid-2027 [S1], this study’s performance against Boston Scientific's standard will define regulatory trajectories and shape market entry strategies.

- Regulatory Submissions: Success in these pivotal trials would precipitate FDA submission timelines likely stretching into late 2020s depending on interim data outcomes.

- Expansion of Partnerships: Further strategic collaborations or licensing agreements could augment geographic reach or portfolio breadth, accelerating commercialization prospects.

Enhancements to underlying technology platforms or additional indications extensions represent longer horizon blockbuster potential contingent on initial trial successes.

Risk Factors and Development Constraints

By nature of clinical-stage biomedical innovation companies, Orchestra BioMed confronts pronounced risks:

Clinical Trial Outcomes: Efficacy/safety results remain uncertain until final analyses; adverse findings delay or negate approvals threatening revenue generation capability [S1].

Regulatory Approval Uncertainty: Complex FDA requirements necessitate substantial evidentiary demonstrations; delays or requests for additional data can extend time-to-market significantly.

Partnership Reliance: The collaboration model inherently depends on active engagement from partners such as Medtronic; misalignments could slow development or restrict market opportunities.

Financial Burn Rate: Persistent net losses totaling an accumulated deficit exceeding $383 million as of Q1 2026 highlight ongoing financing needs; continued capital raises depend on investor confidence tied closely to clinical milestones [S2], [F1].

Market Adoption Risks: Even post-regulatory success, competitive pressures including entrenched reimbursement frameworks, physician preference, pricing challenges, and payer acceptance constrain rapid uptake.

Mitigation efforts include diversified pipeline strategies but ultimate success hinges on navigating these inherent industry constraints.

Upcoming Operational Milestones to Monitor

Key future events warrant close observation:

Confirmation of full patient recruitment completion in BACKBEAT study within projected mid-2026 timeframe as primary signal of operational execution capability [S2].

Interim efficacy/safety data releases from BACKBEAT potentially initiating regulatory dialogue or accelerated review discussions.

Progression metrics from Virtue SAB IDE trial including enrollment pace vis-à-vis mid-2027 goal benchmarks.

Announcements concerning further partnership developments or capital market activity reflecting confidence in developmental trajectory.

These milestones provide quantifiable KPIs reflecting transition from clinical research stage toward potential commercialization inflection points.

Financial Position and Capital Adequacy Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $28.4mm | |

| 2026-03-31 | ||

| Total debt | $15.0mm | |

| 2026-03-31 | ||

| Net debt | -$13.4mm | |

| 2026-03-31 | ||

| Current assets | $96.2mm | |

| 2026-03-31 | ||

| Current liabilities | $13.7mm | |

| 2026-03-31 | ||

| Current ratio | 7.03x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As supported by March 31, 2026 companyfacts data [F1], Orchestra BioMed holds approximately $28.4 million in cash & equivalents complemented by $66.0 million in marketable securities summing to nearly $94.4 million of liquid assets enabling funding through prioritized programs over the next year as affirmed by management disclosures [S3]. Current assets total $96.2 million compared against modest current liabilities approximating $13.7 million yielding a robust current ratio of roughly 7x indicative of sound near-term liquidity.[F1]

Total debt stands at $15.0 million reflecting secured term loan facilities accessed principally to support R&D ramp-ups; net debt is effectively negative at approximately -$13.4 million underscoring available cash buffers surpassing outstanding borrowings[F1]. Despite favorable balance sheet liquidity metrics, net loss rates remain substantial—over $20 million recorded within Q1 2026 alone driven largely by clinical trial investments plus SG&A expenses[S10],[F1].

| Metric | Value (USD '000) | Date |

|---|---|---|

| Cash & Equivalents | 28,367 | |

| 2026-03-31 | ||

| Marketable Securities | 66,033 | |

| 2026-03-31 | ||

| Current Assets | 96,209 | |

| 2026-03-31 | ||

| Current Liabilities | 13,692 | |

| 2026-03-31 | ||

| Total Debt | 15,000 | |

| 2026-03-31 | ||

| Net Debt (Debt - Cash) | -13,367 | |

| 2026-03-31 |

This analysis is based exclusively on publicly filed SEC documents up to May 12, 2026 and validated company facts data as cited. It does not constitute investment advice but seeks to provide a detailed operating understanding grounded in fundamental disclosures specific to Orchestra BioMed Holdings Inc.'s latest developments and industry positioning.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments