Willamette Valley Vineyards Battles Industry Headwinds with Direct-to-Consumer Strategy

The company’s latest quarter highlights margin pressures and volume declines amid ongoing competitive and agricultural challenges.

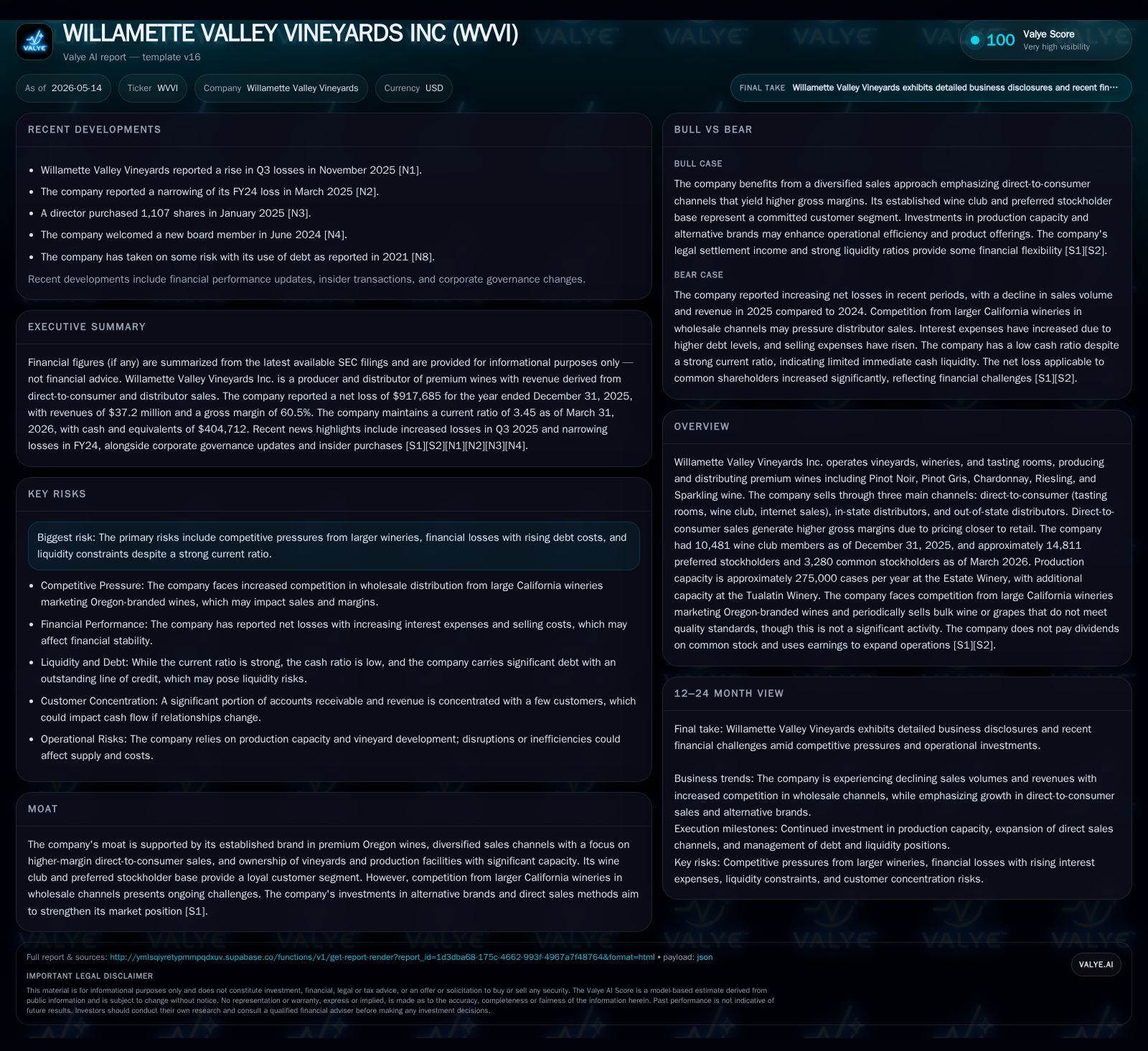

Willamette Valley Vineyards’ 2026 first-quarter operating results reveal continued net losses driven by lower sales volumes and pricing pressure, despite a solid direct-to-consumer (DTC) channel that supports higher margins. The company remains focused on leveraging its premium Oregon AVA branding and scaling wine club membership to offset wholesale market competition, primarily from California producers marketing Oregon-style wines. Agricultural risks like phylloxera infestations and unpredictable weather patterns pose structural constraints, while elevated leverage and covenant waivers underscore near-term financial risks. Monitoring DTC growth metrics, wine club retention, and debt covenant compliance will be critical milestones for assessing the firm’s execution amid these headwinds.

Quarterly Performance and Operational Update

The May 13, 2026 10-Q filing confirms Willamette Valley Vineyards continues to operate under challenging volume and margin conditions. While exact Q1 revenue is not explicitly detailed in the excerpted filings, the company's annual results confirm a net loss of $917,685 in fiscal year 2025 contrasted against modest operating income in previous years [F1], [S2], [S24]. The latest quarter shows ongoing pressure on core sales volumes; the company sold approximately 173,014 cases in 2025 versus 186,419 cases in 2024—a decline of 7.2% attributable to softer demand across both direct sales and distributor channels [S21]. Gross margin compression is evident with a drop from 60.8% to roughly 60.5% year-over-year due primarily to increased discounting [S25]. Despite this environment, the higher-margin direct-to-consumer segment maintains prominence, representing over half of total revenue at about 54.4%, supported by retail tasting room transactions and wine club sales that offer prices closer to full retail [S21]. Seasonal buying behaviors continue to affect quarterly performance cycles with Q1 typically being the slowest in the winery industry which accentuates near-term margin volatility [S1].

Business Model and Product Quality Focus

Willamette Valley Vineyards derives revenues mainly through three channels: direct-to-consumer (DTC), in-state distributors, and out-of-state distributors. The DTC segment comprises tasting rooms, wine clubs, internet sales, on-site event sales, and kitchen/catering services [S16], [S21]. This channel underpins superior unit economics as it captures retail price points with minimal intermediary discounting relative to wholesale distributor sales which command lower margins. Notably, the company boasts a loyal wine club base counting 10,481 members as of December 2025—a slight decline from prior year—but this cohort is vital for recurring revenue streams and customer retention amidst fluctuating retail foot traffic [S21].

Operationally, the business model depends heavily on estate-owned vineyards within Oregon's renowned AVA regions emphasizing terroir-driven Pinot Noir alongside varietals such as Pinot Gris, Chardonnay, Riesling, and Sparkling wines [S16]. Total annual production capacity at the Estate Winery hovers around 275,000 cases with supplementary capacity at the Tualatin Winery facilitating scale flexibility [S1]. The company’s ability to maintain grape quality is critical given consumer expectations within the premium wine segment where small-lot techniques prevail. Bulk wine or grape sales remain an infrequent activity signifying tight quality control standards limiting excess inventory dispositions [S21].

Competitive Landscape and Industry Dynamics

The competitive set pits Willamette Valley Vineyards directly against large California wineries that have aggressively entered Oregon-branded wine categories in wholesale distribution channels [S21]. These competitors benefit from scale advantages that compress pricing power for smaller niche players like WVVI particularly in mass retail grocery environments where shelf space is contested intensely.

Agricultural conditions further complicate the supply side. Phylloxera pest presence at Tualatin Estate Vineyards raises concerns over vineyard health resilience given limited vine rootstock resistance; this risk extends to potential broader vineyard spread necessitating costly mitigation efforts which impact production costs over time [S1]. Moreover, unpredictable Pacific Northwest climate patterns—including excessive rains in harvest seasons or wildfire smoke exposure—pose tangible threats to grape quality affecting vintage reliability and downstream product consistency [S1]. Regulatory measures aimed at pest control or environmental protections could impose additional operational burdens.

Growth Drivers: Expanding Direct Sales and Brand Equity

Willamette Valley Vineyards levers its growth chiefly through intensifying penetration of the direct-to-consumer sales channel characterized by tasting rooms expansion and digital commerce acceleration [S1], [S2]. Wine club membership acts as a strategic growth KPI; although it experienced a minor contraction of about 700 members year-over-year to approximately 10,481 subscribers as of late 2025, management’s focus remains on revitalizing this base through personalized engagement events and incentivized renewals [S21]. Alternative brand introductions diversify product offerings aiming to capture emerging consumer niches within premium segments.

Incremental investment in hospitality centers signals intent to drive experiential customer acquisition funneling into higher-margin DTC volumes. Online platform enhancements also aim to reduce dependence on traditional wholesale channels especially vulnerable to competitor pricing encroachment. These initiatives align with industry trends where wineries globally seek organic growth through owned-channel acceleration leveraging brand authenticity tied closely to Oregon’s terroir narrative.

Risks and Constraints: Agricultural Vulnerabilities and Financial Challenges

Persistent agricultural hazards underline a significant risk vector for Willamette Valley Vineyards’ long-term viability. Phylloxera infestations threaten vine health stability—particularly acute since some rootstocks are non-resistant—and any extension of these pests could lead to yield reductions or forced replanting cycles incurring substantial costs [S1]. Weather variability including frost risk during critical phenological periods coupled with wildfire smoke events distort harvest timing and fruit quality parameters essential in premium winemaking.

Financially, as of March 31, 2026, total debt stood near $14.9 million with net debt approximated at $14.5 million after accounting for cash reserves of about $405k [F1]. This substantial leverage level contrasts with a healthy current ratio of approximately 3.45 indicating good liquidity buffer for near-term obligations but suggesting elevated balance-sheet risk if top-line pressures persist or credit conditions tighten unexpectedly [F1], [S2]. This snapshot underscores an enterprise capable of meeting short-term liabilities comfortably but carrying significant leverage reflective of ongoing capital investment in vineyards and facilities expansions funded through debt issuances secured against key estate properties [F1]. The incremental increase in interest expenses reported underscores rising funding costs linked to incremental borrowings last year [S4]. Management’s ability to optimize capex spending while improving operational cash flow remains crucial for deleveraging prospects.

Key Milestones and Forward-Looking Indicators

Upcoming catalysts for investor monitoring include quarterly updates on wine club membership changes since they serve as leading indicators for DTC revenue momentum. Shipment volume data broken down by channel will clarify whether wholesale declines are stabilizing or worsening under competitive pressure. Pricing trends especially related to discount rates or promotional activity in wholesale distribution could portend margin sustainability issues.

Additional operational markers encompass any vineyard expansion progress or replanting initiatives designed to counteract phylloxera damage timelines. Promotional event rollouts or new tasting room openings will reflect management’s execution capacity on growth strategy fronts.

Notably absent is explicit near-term earnings guidance beyond seasonal commentary stressing Q1 softness; hence market participants should track sequential results closely alongside agricultural reports impacting harvest outcomes.

Latest Financial Position and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $404,712 | |

| 2026-03-31 | ||

| Total debt | $14,935,020 | |

| 2026-03-31 | ||

| Net debt | $14,530,308 | |

| 2026-03-31 | ||

| Current assets | $37,527,230 | |

| 2026-03-31 | ||

| Current liabilities | $10,880,613 | |

| 2026-03-31 | ||

| Current ratio | 3.45x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 404,712 |

| Total Debt | 14,935,020 |

| Current Assets | 37,527,230 |

| Current Liabilities | 10,880,613 |

| Current Ratio | 3.45 |

| Revenue (Annual) | 37,197,122 |

| Net Income (Annual) | -917,685 |

This analysis integrates recent quarterly operating disclosures with longer-term structural assessments derived from annual filings providing a granular perspective on Willamette Valley Vineyards’ complex positioning within premium Oregon viticulture amid competitive pressures. The company’s strategy centres on deepening direct consumer engagement leveraging terroir-driven differentiation; however agricultural risks combined with financial leverage necessitate close monitoring of operational execution milestones.

Disclaimer: This report is an independent analytical summary based solely on publicly available regulatory filings as of May 14th, 2026 and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments