Lafayette Digital Acquisition Corp. I Executing SPAC Mandate with Focus on Financial and Tech Sectors

The company's latest quarter underscores progress in capital deployment readiness as it pursues a transformative acquisition within its 24-month mandate.

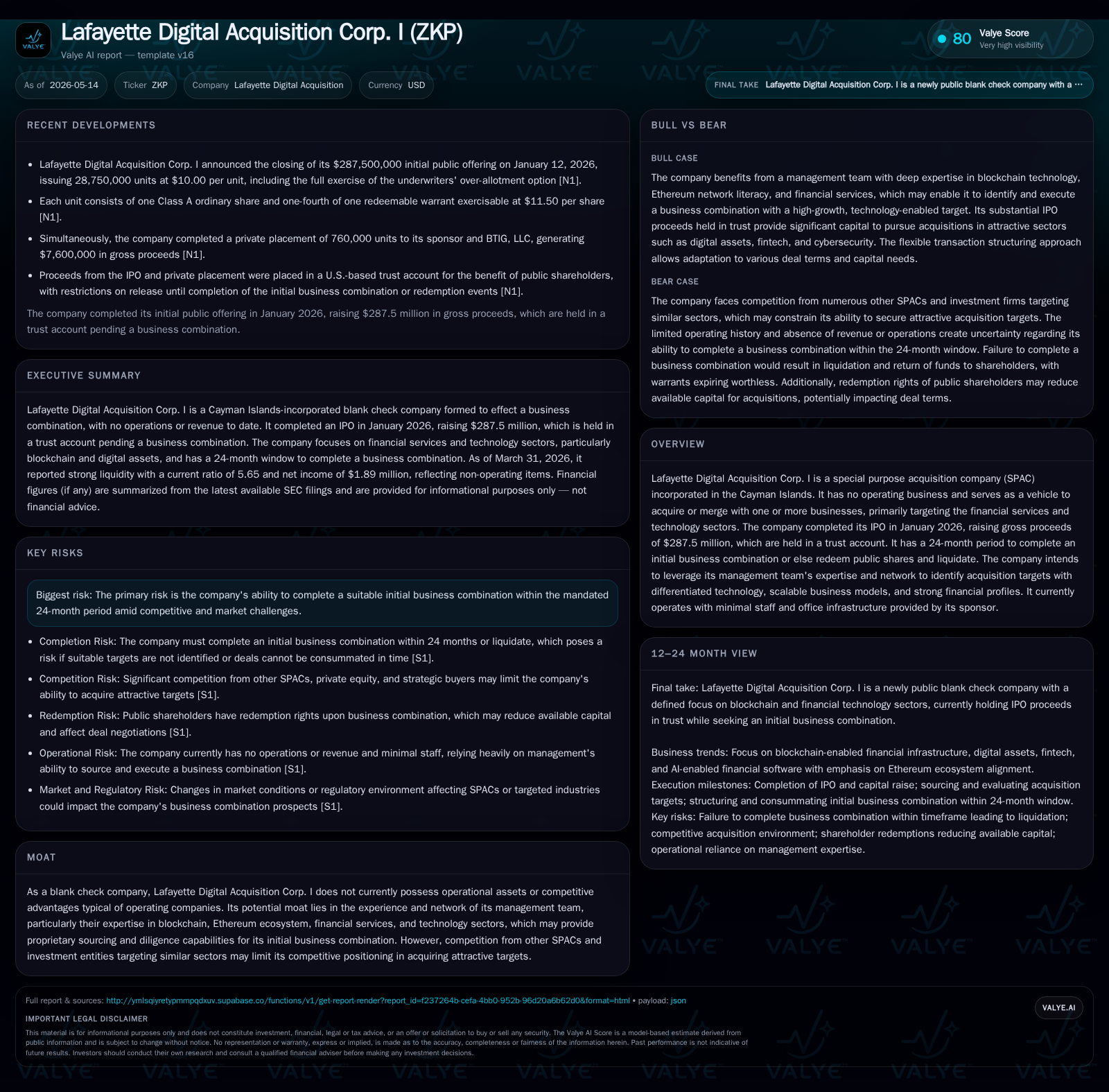

Lafayette Digital Acquisition Corp. I (ZKP) remains a classic SPAC entity with no operating history but solid financial resources following its January 2026 IPO. The May 2026 quarterly update confirms steady strategic positioning, holding over $1 billion in liquid assets awaiting an initial business combination. Its management leverages deep Ethereum and financial services expertise to target tech-enabled, scalable businesses primarily in blockchain-related finance and technology sectors. While competition among SPACs intensifies, Lafayette's niche focus on Ethereum ecosystem opportunities may provide differentiated deal flow and diligence advantages.

Recent Operating Update

Lafayette Digital Acquisition Corp. I’s latest quarterly report filed May 13, 2026 ([S2]) reiterates its status as an operatingly dormant special purpose acquisition company (SPAC). It holds approximately $1.03 billion in current assets against $183 million of current liabilities ([F1]), yielding a very strong current ratio of 5.65—highlighting ample liquidity to fund an initial business combination without immediate financial pressures.

Operating income remains negative due to corporate expenses totaling about $305,000 this quarter ([F1]), consistent with pre-acquisition activity typical of SPACs. The firm recorded a small net loss of around $58,000 as of end-2025 ([F1]), reflecting ongoing overhead and administrative costs prior to any acquisition revenue generation.

There were no material changes compared to the prior filing period; Lafayette continues to maintain minimal headcount—two officers dedicating varying time toward sourcing deals and managing operations—while office space expenses are provided by an affiliate sponsor for about $20,000/month and reimbursed accordingly ([S13]).

This timeline adds strategic urgency to sourcing and completing a value-accretive transaction.

Business Model

Lafayette Digital Acquisition Corp. I operates as a Cayman Islands–incorporated blank check company with no revenue-generating operations or product offerings ([S5]). Its sole purpose is to raise capital through an IPO and private placements (completed in January 2026 for gross proceeds of approximately $295 million combined) that are placed in trust accounts reserved for executing at least one transformative business combination ([S5][S8]). The trust funds are invested conservatively in U.S. government securities or qualifying money-market funds to preserve principal until deployment.

The company makes money only if it successfully completes a merger or acquisition involving entities primarily focused on the financial services technology sector, especially targeting blockchain-based infrastructure, Ethereum ecosystem participants, payment technologies, AI-enabled finance software, cybersecurity encryption products, or related compute hardware ([S3][S7]).

Revenue generation post-merger will depend entirely on the operational performance of the acquired entity rather than Lafayette itself. Meanwhile, investor returns hinge on identification of a high-quality candidate where scaling opportunities align with public market liquidity.

The company plans to generate deal flow through leveraging the management team's extensive network encompassing founders, venture investors, corporate development teams, banks, and strategic partners ([S7]). Their domain expertise particularly emphasizes Ethereum protocol developments—including scalability solutions like sequencing and cryptographic validation—potentially conferring selective advantage in due diligence depth and quality relative to generalist SPAC sponsors.

In exchange for pursuing such transactions, shareholders have redemption rights enabling them to redeem shares at roughly $10 per share plus accrued interest upon deal approval or tender offer scenarios ([S9]). The sponsor holds founder shares and private units that do not participate in redemption value but do incur dilution risk.

Industry Structure and Competitive Position

Operating within the burgeoning yet crowded SPAC ecosystem focusing on financial technology adoption trends poses structural challenges. Several competing SPAC sponsors alongside traditional private equity groups aggressively pursue fintech disruptions including digital asset infrastructure, payments modernization, AI-fintech convergence, and cybersecurity enhancements ([S10]).

Unlike larger financial sponsors with multibillion-dollar war chests, Lafayette’s initial capital pool (~$295 million gross from IPO plus private placement) imposes scale constraints on target size selection ([S10]). This may limit participation in larger transaction processes or compel co-investment arrangements.

Nevertheless, Lafayette’s differentiator lies in its niche focus on blockchain-enabled financial services anchored around Ethereum’s open-source platform developments. Management’s active involvement in Ethereum community discussions and development forums provides intellectual capital assets that can unlock proprietary deal flow or spot technically sound ventures others might overlook ([S7]).

Their capacity to rigorously underwrite complex tech-market intersection scenarios theoretically elevates post-combination operational resiliency which aligns well with mission-critical enterprise requirements common among regulated tech-finance companies ([S3]).

However, competitive forces include redemption rights exercised by shareholders which reduce available cash after IPO proceeds are depleted toward acquisitions—diluting bargaining power vis-à-vis sellers who may prefer more cash-intensive offers from better-capitalized bidders ([S9][S10]).

Growth Drivers

Growth potential exclusively depends on completing an initial business combination signing within the regulatory window followed by successful operation scaling:

- Capital availability: Trust account funds exceed $1 billion providing substantial dry powder for sizable transactions despite anticipated redemptions [F1].

- Niche expertise leverage: Deep Ethereum knowledge allows tapping nascent protocol-driven opportunities across decentralized finance platforms needing scalable infrastructure [S7].

- Network access: Relationships spanning venture investors to corporate strategics enhance access to timely deal pipeline introductions versus cold outreach alone [S7].

- Flexible deal structuring: Willingness to entertain earn-outs, equity rollovers, PIPEs (private investments in public equity), or debt financing enables tailored capital stack solutions accommodating target preferences [S3].

- Public market re-entry: Combining with Lafayette offers private tech-forward financial firms transparent KPIs and governance standards suited for U.S. public capital markets facilitating growth capital access post-business combination [S3].

Risks / Watchpoints / Growth Constraints

Key risks impacting Lafayette’s trajectory include:

- Timing pressure: A finite two-year deadline mandates urgency—failure triggers forced share redemptions draining trust funds pushing toward liquidation [S12][S14].

- Competitive auction dynamics: Overlapping investor syndicates chasing similar fintech-blockchain targets amplify bidding contests and compress margins leaving fewer attractively priced deals available [S10].

- Redemption dilution effect: Shareholder redemptions upon merger approval can significantly reduce available cash for acquisition consideration limiting negotiation bandwidth [S9][S10].

- No internal operations/profits: Entire strategic value rests on securing one stellar transaction — operational execution risk post-combination cannot be wholly mitigated pre-deal.

- Regulatory shifts: Blockchain landscape subject to evolving regulatory oversight globally potentially constraining addressable market sizes or operational freedom post-merger.

- Sponsor incentives alignment: Sponsor holds founder shares not subject to redemptions but potential misalignment arises if shareholder interests diverge especially if valuation benchmarks become contested during merger talks.

What To Watch Next

Upcoming milestones pivotal for Lafayette’s evolution include:

- Identification & announcement of target business: An official announcement followed by detailed disclosure enabling shareholder review marks key progress towards closing completion window deadlines.

- Shareholder approval vs tender offer decision: The company controls whether the combination requires formal meeting votes or opts for tender offer style redemptions affecting timing and shareholder engagement levels [S9].

- Negotiation & structure details: Terms including cash vs stock consideration splits; earn-out provisions; PIPE involvement; equity rollovers indicating sponsor alignment should emerge publicly once transactions firm up.

- Redemption rates upon deal announcement: High redemption levels can impair funding size influencing deal feasibility or requiring additional backstop financing to fill gaps.

- Closing within mandated window: Clock runs out roughly January 2028 unless extensions obtained—failure elicits automatic wind-down diminishing shareholder returns materially [Compliance outlined in filings S12/S14].

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $135,369 | |

| 2025-12-31 | ||

| Net debt | $135,369 | |

| 2025-12-31 | ||

| Current assets | $1,034,323 | |

| 2026-03-31 | ||

| Current liabilities | $183,223 | |

| 2026-03-31 | ||

| Current ratio | 5.65x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Current Assets | $1,034M | |

| 2026-03-31 | ||

| Current Liabilities | $183M | |

| 2026-03-31 | ||

| Current Ratio | 5.65 | |

| 2026-03-31 | ||

| Total Debt | $135K | |

| 2025-12-31 | ||

| Operating Income | -$305K | |

| 2026-03-31 |

The balance sheet exhibits robust liquidity maintained largely from IPO proceeds held in trust accounts invested conservatively. Remaining overhead costs reflect normal pre-acquisition SPAC administrative expenses.

Disclaimer

This analysis is provided solely for informational purposes based on publicly available filings as of May 2026. It does not constitute investment advice or recommendations regarding Lafayette Digital Acquisition Corp. I or any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments