OriginClear Accelerates Water On Demand Growth While Managing Profitability and Liquidity Challenges

The latest quarter highlights significant revenue gains in engineered water treatment amid ongoing development of a novel pay-per-gallon wastewater service.

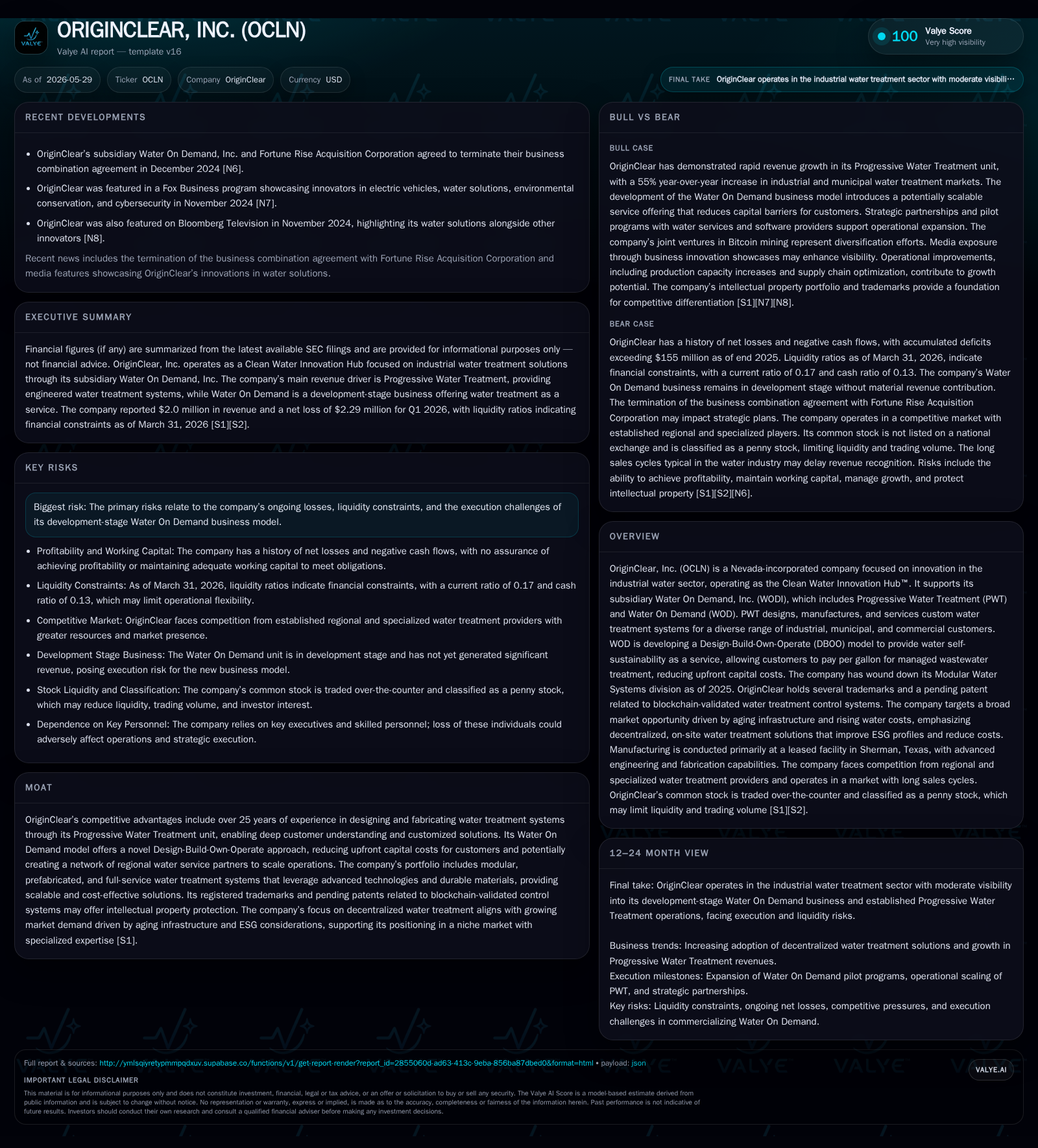

OriginClear, Inc. reported strong operational momentum in its Progressive Water Treatment unit, with a notable 55% year-over-year revenue increase driven by industrial and municipal water system projects. Concurrently, the company advances its development-stage Water On Demand platform, which offers Design-Build-Own-Operate services that reduce customer capital expenditures through per-gallon payment models. Despite this progress, OriginClear continues to face liquidity constraints and a persistent history of net losses, underscoring execution risks as it seeks to scale its innovative service offerings and sustain operations. The company’s wind-down of its Modular Water Systems division and recent leadership transition add complexity to near-term strategy execution.

Recent Operating Update

OriginClear’s latest quarterly filing dated May 29, 2026 [S2] details ongoing operational developments that bear directly on its business trajectory. Progressive Water Treatment (PWT), the company's largest revenue contributor, continues to demonstrate robust sales execution in industrial and municipal water treatment projects. This group achieved a substantial 55% increase in revenue year-over-year as noted in the prior annual report [S1], with growth poised to continue as projects initiated in 2025 complete during the current fiscal year.

Concurrently, OriginClear is actively advancing its Water On Demand (WOD) business unit—a nascent initiative offering an innovative Design-Build-Own-Operate (DBOO) solution. This platform enables private businesses to outsource water treatment capacity with financing structures that shift costs from upfront CapEx to predictable per-gallon service payments [S9,S23]. The company is preparing pilot programs supported by strategic partners Enviromaintenance and Klir, aimed at proving commercial viability while building a regional network of service providers

Notably, the Modular Water Systems (MWS) division was fully wound down during 2025 [S10], marking a pivot away from competing directly in modular equipment manufacturing toward integrated service models embodied by WOD.

In a recent corporate event disclosed on May 13, 2026 [S3], OriginClear announced the unfortunate passing of CEO Riggs Eckelberry who also held a controlling voting interest. This change introduces potential uncertainty amidst ongoing execution challenges.

Business Model

OriginClear operates primarily through its subsidiary Water On Demand, Inc. (WODI) which integrates two main operating units:

Progressive Water Treatment (PWT): Focuses on design, manufacture, and servicing of custom-engineered water treatment systems spanning industrial process water, municipal potable stations, food & beverage effluent management, energy sector produced water treatment, and environmental remediation [S8]. PWT leverages over 25 years of technical expertise across multiple purification technologies including membrane filtration, chemical injection, ion exchange, and SCADA system integration.

Water On Demand (WOD): A development-stage business model delivering outsourced water treatment solutions via a DBOO approach that reduces customer capital intensity while providing predictable operational expenses tied to actual usage metrics. WOD aims to create a scalable ecosystem by delegating system build and operation to regional partners under performance contracts [S13].

Revenue for PWT derives from turnkey system sales including installment contracts with maintenance agreements and equipment rentals. Pricing factors are influenced by system volume/complexity mix and aftermarket servicing terms. Margins can improve through scale standardization efforts introduced in recent years.

WOD's revenue mechanics revolve around recurring service fees based on gallons treated or flat fees under managed contracts rather than large upfront equipment purchases. This model potentially fosters longer-term customer relationships but requires scaling capital deployment alongside operational reliability.

Intellectual property assets include trademarks such as ORIGINCLEAR® and $H2O®, alongside pending patents concerning blockchain verification technology purportedly designed for enhanced control system security—though blockchain is not critical for current operations [S11]

Industry Structure and Competitive Position

OriginClear situates itself within the fragmented industrial water treatment ecosystem characterized by an increasing shift towards decentralized solutions due to aging centralized infrastructure cost pressures [S9]. This market includes competitors delivering prefabricated modular systems and various forms of outsourced water management services.

Its competitive strengths derive from PWT’s engineering depth accumulated over decades supporting diverse regulated industries—providing highly customized systems tailored to complex client requirements. This contrasts with commodity modular platforms that emphasize rapid deployment but may lack bespoke engineering customization.

Meanwhile, WOD’s emerging DBOO model aims to introduce greater financial flexibility for commercial users historically deterred by large capital expenditures for wastewater systems—a segment increasingly attractive given tighter ESG-driven mandates on water sustainability [S9]. The planned partner network strategy may create barriers to entry if successful but remains pre-commercial and execution-dependent.

Industry participants often contend with significant channel partnerships or direct sales forces; OriginClear has augmented sales pipelines materially while pursuing supply chain optimization to improve production scalability [S1]. However, existing players with deeper financial resources or longer market tenure pose continuous threats.

Growth Drivers

Growth momentum is currently led by the following factors:

- Expanding Market Reach: Strengthened regional sales channels have broadened the customer base especially in sectors requiring mid-scale municipal or industrial water treatment upgrades.

- Operational Efficiency Improvements: Standardization of modular designs coupled with supply chain enhancements allow faster manufacturing cycles supporting higher volumes at improved gross margins.

- Water On Demand Pilot Programs: Early-stage agreements with service companies signal potential for growing managed contract revenues instead of one-time system sells.

- Environmental Regulation Trends: Increasing regulation toward reducing wastewater discharge contamination compels firms toward improved onsite treatment solutions compliant with evolving standards.

- Shift Toward Decentralized Systems: Customer preference for localized water cycling aligns with OriginClear’s technology stack designed for compactness and automation allowing easier installation near points of generation.

KPIs relevant here include backlog visibility within PWT projects slated for recognition through 2026 completion schedules along with pilot contract milestones reached by WOD’s joint ventures [S1,S23]

Risks / Watchpoints / Growth Constraints

Several risk factors merit close monitoring:

- Liquidity Constraints: As evidenced by a current ratio near 0.17 and working capital deficits over $19 million [F1], OriginClear faces ongoing funding requirements posing existential risk if capital markets access tightens.

- Profitability Challenges: Persistent net losses exceeding $18 million in recent years demonstrate operating leverage limitations versus planned sales ramp-up; failure to attain economies of scale will imperil sustainability [F1,S1].

- Execution Uncertainty: Business model innovation within WOD requires reliable regional partnerships; partner commitment or operational misalignments could impair rollout and cash flow forecasts [S26].

- Leadership Transition: The death of CEO Riggs Eckelberry removes both principal executive leadership and majority voting power control which may impact strategic consistency or investor confidence near term [S3,S15].

- Competitive Pressures: Larger incumbents benefit from financial firepower and established engineering teams; they may accelerate product innovation or price competition affecting market share gains.[S15]

- Customer Adoption Risks: Transitioning clients from CapEx-heavy procurements to DBOO contracting demands behavioral shifts that may be gradual or met with resistance among traditional buyers.

- Regulatory Dependencies: Reduction or withdrawal of government subsidies affecting certain end markets can lower demand; emergent compliance costs may also increase system ownership cost burdens.[S26]

- Intellectual Property Protection: Reliance on trade secrets plus external patent rights leaves OriginClear vulnerable relative to firms supported predominantly by a portfolio of enforceable patents.[S20]

What to Watch Next

Key milestones likely influencing OriginClear’s progress include:

- Completion rates and revenue recognition updates for backlog projects within PWT throughout remainder of 2026 [S1].

- Commercialization outcomes from WOD pilot programs involving Enviromaintenance JV activity and expansion into additional regional partners.[S23]

- Capital raising success or any material changes in liquidity position disclosed in subsequent quarterly releases given ongoing deficits.[F1,S2]

- Appointment announcements regarding new executive leadership post-Eckelberry’s demise that clarify strategic continuity.[S3]

- Developments in intellectual property filings or licensing agreements related to blockchain-enhanced control technologies.[S11]

- Partnerships expansion announcements facilitating accelerated DBOO network growth potentially assembling protective moats against competitive incursions.[S13]

Monitoring these operational KPIs alongside cash flow trends will be critical to gauge whether OriginClear moves beyond development-stage investment toward scalable profitability.

Financial Profile Summary (Latest Quarter Context)

As of March 31, 2026, OriginClear held approximately $3.3 million in cash & equivalents against current liabilities nearing $26.4 million resulting in a current ratio of roughly 0.17—a signal of short-term liquidity strain [F1]. Total debt remains minimal relative to cash balances per available data indicating limited external borrowings currently accessible [F1].

Revenue recorded through calendar year-end 2025 amounted to about $6.8 million while incurring an operating loss exceeding $3.3 million reflective of elevated operating costs associated with growth initiatives and R&D efforts linked primarily to WOD development [F1,S1]. The net loss was substantially larger due principally to non-operating items including convertible debt discounts impacting equity dilution metrics adversely

Continued reliance on capital injections remains apparent without clear paths yet demonstrated toward stable positive cash flow generation absent improved operating efficiencies or breakthrough contract wins that secure recurrent income streams.

Disclaimer

Financial position in context

As of 2026-03-31, companyfacts shows $3mm in cash and equivalents [F1]. Current assets of $4mm and current liabilities of $26mm imply a current ratio near 0.17x for 2026-03-31 [F1].

This analysis is provided solely for informational purposes based on public filings as of May 29, 2026. It does not constitute investment advice or research views. Readers should perform their own due diligence before making any investment decisions related to ORIGINCLEAR, INC.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments