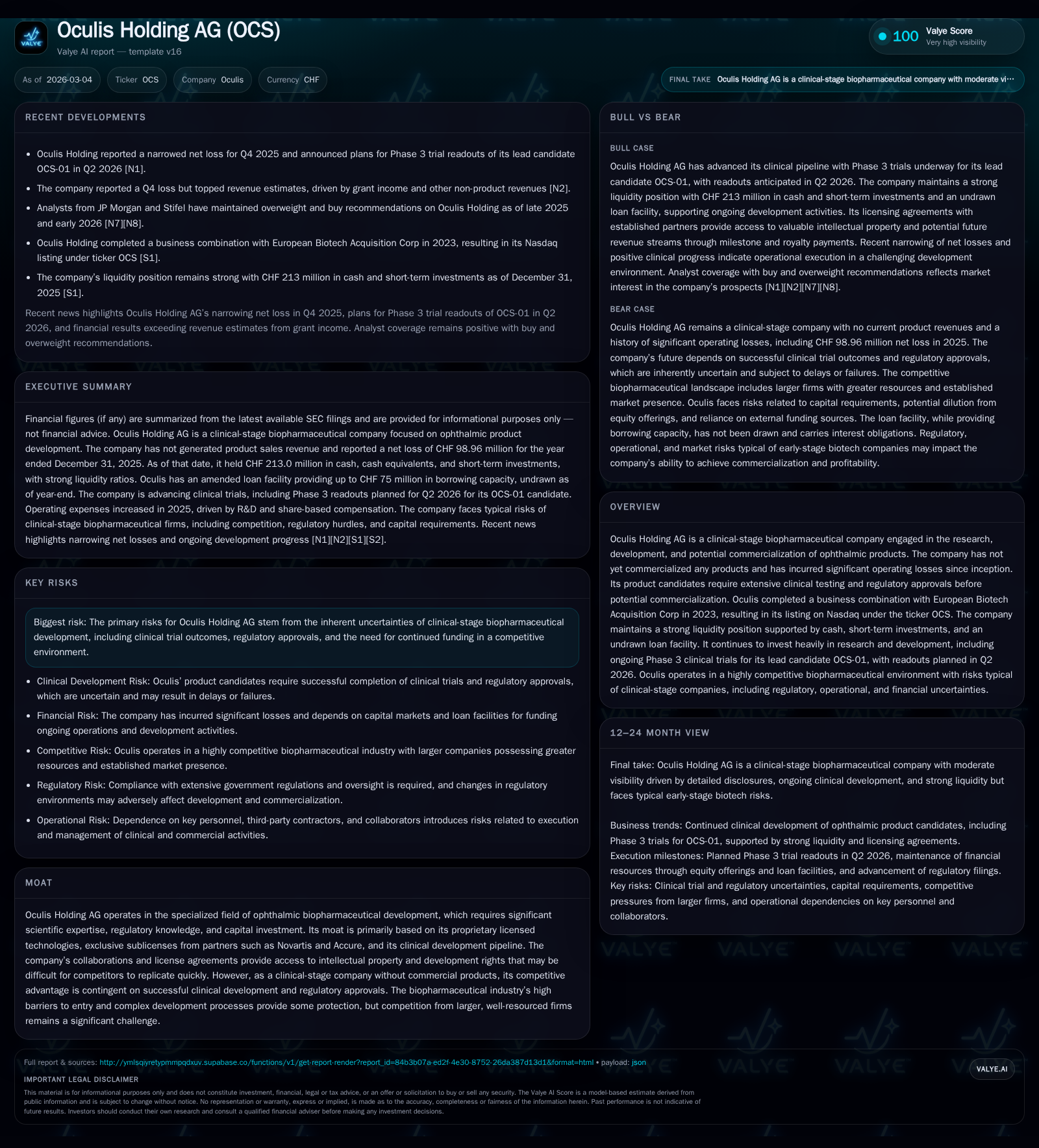

Oculis Holding AG Faces Crucial Clinical Milestones While Managing Rising Costs and Strong Liquidity

Clinical-stage ophthalmic biotech company progresses Phase 3 trials amid heavy R&D spending and a solid balance sheet.

Oculis Holding AG remains a clinical-stage biopharmaceutical entity focused on developing novel ophthalmic treatments with no current commercialized products. The company's historical losses reflect substantial investments in advancing its pipeline, notably OCS-01 in late-stage DME treatment. Cash reserves and undrawn loan facilities provide strong liquidity cushioning near-term operations, with anticipated Phase 3 topline readouts in Q2 2026 serving as key catalysts. Rising R&D expenses, driven by clinical advancements and increased personnel costs, underscore the capital-intensive nature of Oculis’ development path. The firm’s ability to achieve regulatory approvals and subsequent commercialization remains pivotal for future growth.

Company Overview and Historical Performance

Oculis Holding AG is a Swiss-headquartered biopharmaceutical company specializing in ophthalmic therapeutics, particularly neuro-ophthalmic diseases with significant unmet medical needs. Established as a clinical-stage entity, it completed a business combination with European Biotech Acquisition Corp in March 2023, listing shares on Nasdaq under ticker OCS [S1][N1].

Since inception, Oculis has operated without revenue from commercial products and demonstrated consistent net losses due to extensive R&D activities [F1][S9]. For the fiscal year ended December 31, 2025, the company recorded a net loss of approximately CHF -98.96 million [F1], reflecting a deepening of losses by about 15% compared to the prior year. This trend underscores ongoing investments to advance multiple clinical-stage candidates through costly development stages.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | -99 | -15.4% |

| 2024 | -86 | +3.4% |

| 2023 | -89 | -129.5% |

| 2022 | -39 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -50.5 |

| 2024 | -116.9 |

| 2023 | -94.7 |

| 2022 | 39.5 |

Source: SEC companyfacts cache [F1].

Table: Selected financial metrics illustrating loss persistence and strengthening balance sheet liquidity [F1]

Research & Development Focus and Operational Costs

R&D expenses totaled CHF 57.1 million for FY2025, up nearly 10% from CHF 52.1 million in FY2024 [S5][S10]. Growth was primarily propelled by advancing late-stage clinical trials including the Phase 3 DIAMOND program for OCS-01 addressing diabetic macular edema (DME) [S18]. Enrollment completion occurred in April 2025 with topline readouts anticipated in Q2 2026 [N2]. Additionally, Privosegtor – targeting neuroprotection in optic neuropathies – accounted for significant incremental costs due to intensified development activities [S18]. Conversely, costs related to Licaminlimab decreased following the transition from Phase 2 trials into registrational studies employing genotype-based precision medicine for dry eye disease (DED) [S18][S1].

General and administrative expenses rose markedly by approximately 30% year-over-year to CHF ~15 million owing largely to personnel-related costs including salary increases and elevated share-based compensation expenses [S10][N1]. Such cost escalations reflect business scale-up efforts required for regulatory compliance, dual listings on Nasdaq and Nasdaq Iceland, and preparatory commercialization infrastructure.

Pipeline Overview: Clinical Candidates and Market Opportunities

Oculis’ development portfolio centers around three clinical-stage product candidates:

- OCS-01: A topical eye drop intended as a first-in-class non-invasive treatment for DME currently undergoing two Phase 3 trials (DIAMOND-1 & DIAMOND-2). Topline efficacy data are expected Q2 2026 [S1][N2].

- Licaminlimab (OCS-02): Focused on keratoconjunctivitis sicca or DED using a precision medicine approach based on genotyping with ongoing registrational Phase 2/3 PREDICT-1 trial initiated late 2025; results expected late 2026.

- Privosegtor (OCS-05): A neuroprotective agent targeting optic neuritis (ON), non-arteritic anterior ischemic optic neuropathy (NAION), with potential expanded indications in neuro-ophthalmology; initiates registrational PIONEER program post successful FDA interaction [S1][N2].

The broader ophthalmology therapeutics market is estimated to reach over $33 billion globally by 2027, encompassing substantial demand for treatment innovations addressing retinal diseases, inflammation-driven conditions like DED, and neuroprotection beyond intraocular pressure reduction for glaucoma [S1]. This elevates the commercial potential if regulatory milestones can be met.

Capital Structure, Liquidity Position, and Funding Activities

As of December 31, 2025, cash and equivalents stood at CHF 81 million within total current assets of CHF ~219 million against liabilities of CHF ~37 million, yielding a strong current ratio near six times—a healthy liquidity buffer for ongoing operations [F1][S8][S23]. The firm holds an undrawn amended loan facility providing up to EUR ~75 million (CHF75m equivalent) with flexible tranches enabling access subject to covenants such as debt-to-market cap ratios capped below 15% [S4][S6][S11]. Interest rates are fixed between roughly9.5%-9.7%, with interest-only periods extending through late-2027/mid-2028 contingent on milestones.

Equity financing has been a mainstay funding source recently: significant capital raises include a CHF ~53.5 million registered direct offering in April 2024, CHF ~90 million underwritten shares sale in early 2025, followed by an additional $110 million offering via underwritten/direct channels in November 2025 [S14][S23]. These proceeds have materially strengthened shareholders' equity which more than doubled from CHF ~73m at end-2024 to CHF ~196m at end-2025 per company filings and XBRL data [F1].

Returns Profile and Capital Deployment Priorities

With persistent net losses totaling around CHF -99 million in FY2025 against equity near CHF196 million, the approximate ROE hovers at -50%, reflecting the early stage without revenue generation or profitability yet achieved [F1]. No dividends or buybacks are planned given the current focus on reinvesting capital towards pipeline advancement.

Investment priorities remain heavily weighted towards accelerating clinical trial execution, regulatory filings preparations, manufacturing scale-up for pivotal studies, intellectual property protection fees linked to partnerships with Novartis and Accure Therapeutics [S22][S23], as well as expanding commercial capabilities contingent upon successful approvals.

Key Risks and Outlook Considerations

Major risk factors include typical biopharma uncertainties related to clinical trial outcomes—the upcoming mid-year data release from OCS-01's Phase3 studies represents a decisive inflection point that could validate or derail nearer-term commercial aspirations [N2][S7][S29]. Regulatory hurdles remain formidable given demanding approval pathways for novel ophthalmic agents.

Financially sustaining expensive research without product revenues imposes funding risk mitigated presently by cash reserves but requiring continued successful capital markets access or strategic partnerships beyond the medium term [S21]. Competition within ophthalmology drug development is intense featuring large pharmaceutical incumbents with deeper pockets challenging innovation windows even as smaller specialty firms vie aggressively.

Looking forward into calendar year~2026:

- Monitoring OCS-01 Phase3 topline readouts scheduled Q2 will be pivotal,

- Progression of Licaminlimab’s registrational approach based on genotype-targeted therapy,

- Advancement of Privosegtor programs broadening indication scope,

- Management execution on capital use efficiency amid ramping G&A overhead linked to public company compliance, remain crucial variables influencing Oculis’ trajectory.

Conclusion

Oculis Holding AG exemplifies a late-clinical stage biotechnology developer grappling with the capital intensity of translational science while positioning key therapeutic candidates targeting sizable ophthalmology markets burdened by unmet needs. Despite historical losses reflecting developmental investments customary among peers at this juncture, its balanced liquidity position supported by recent equity injections plus loan capacity provides operational runway through critical data milestones approaching within months.

The company's future growth hinges strongly upon successful proof-of-concept verification via pending Phase3 data releases that will guide labeling strategies and potentially catalyze partnerships or early commercialization steps. Continuing investment into pipeline depth alongside prudent capital management will remain focal points reflecting typical risk-return profiles endemic to innovation-driven healthcare sectors advancing towards commercialization.

This analysis is intended solely for informational purposes based on publicly available data as of early March 2026; it does not constitute investment advice or recommendations regarding securities of Oculis Holding AG.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments