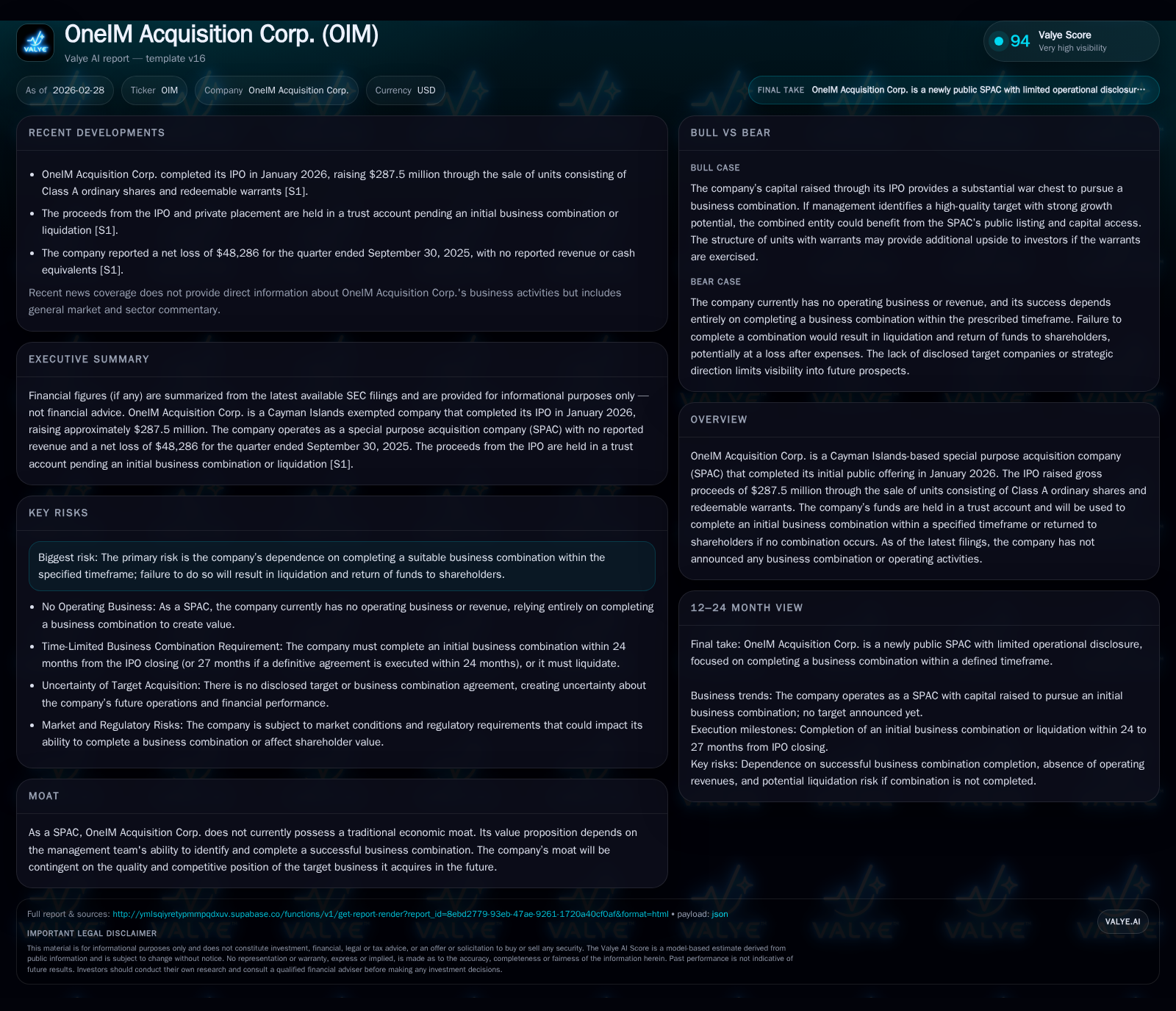

OneIM Acquisition Corp.: Evaluating the SPAC’s IPO Momentum and Acquisition Outlook

An analysis of OneIM Acquisition Corp.’s recent IPO, capital structure, and strategic positioning ahead of its initial business combination.

OneIM Acquisition Corp. launched its SPAC with a January 2026 IPO that raised approximately $287.5 million, anchoring its capital in a trust account until a business combination is secured. The entity currently operates as a shell company with no operational revenues or disclosed deal targets, relying on management's acquisition expertise and the typical SPAC timeline to create value. Key risks include the imperative to complete an acquisition within the prescribed timeframe or risk liquidation, while capital preservation through the trust account and warrant structures positions investors for potential upside upon deal execution.

Foundation Laid: IPO Timing, Capital Raised, and Initial Structure

OneIM Acquisition Corp. launched its initial public offering (IPO) on January 15, 2026, successfully raising gross proceeds of around $287.5 million by selling 28.75 million units priced at $10 each. Included in this offering was the exercise of the underwriters’ over-allotment option amounting to 3.75 million units, underscoring robust demand at launch [S3],[S5]. Concurrently, a private placement contributed an additional $2 million via the sale of 200,000 units to the sponsor at the same price point [S6],[S10]. Each unit comprises one Class A ordinary share paired with one-sixth of a redeemable warrant — each full warrant granting rights to purchase a share at $11.50 per share [S3],[S9].

The capital raised is deposited into a U.S.-based trust account managed by Continental Stock Transfer & Trust Company as trustee, designed with strict safeguards preventing premature use of funds beyond permitted administrative expenses. This architecture aims to shield investors' funds from operational contingencies until the company consummates an initial business combination [S8],[S9],[S14]. Notably, approximately $15.8 million deducted from gross proceeds represents deferred underwriting discounts payable to Deutsche Bank Securities acting as lead underwriter [S10].

Crucially, OneIM's Articles of Association mandate completing a qualifying business combination within 24 months post-IPO — extendable by three additional months pending shareholder approval — else triggering automatic liquidation and refunding of trust balances to public shareholders [S4],[S14]. Redemption rights embedded within unit holders’ warrants and shares further anchor investor protections against adverse deal outcomes.

Operational Activity Since Launch: Performance Metrics and Activity

Reflective of its SPAC status and nascent lifecycle, OneIM exhibits no revenues or substantive operating activity since inception. Financial disclosures reveal net losses totaling approximately $48,286 for the latest quarter ended September 30, 2025, primarily attributable to administrative expenses typical before any acquisition or operational deployment occurs [F1],[S2],[S4]. This underscores its role as a capital pool rather than an operating business at present.

In industry parlance, OneIM functions as a pure 'SPAC float' — holding cash earmarked strictly for future acquisition rather than generating active cash flow streams. The opportunity cost inherent in this static capital allocation model underscores the necessity for swift selection and closing of suitable business combinations to justify investor entries relative to other deployment vehicles. Until then, pricing volatility often relates more strongly to anticipated transactions than fundamental earnings metrics.

Strategic Outlook: Assessing Business Combination Prospects and Deal Pipeline

As of late February 2026, there have been no public disclosures regarding candidate targets or definitive agreements towards an initial business combination [N3]. Typical SPAC sponsor dynamics anticipate leveraging management networks and market intelligence to source attractive entrepreneurial ventures fitting strategic investment theses. Investors commonly monitor indicators such as market rumors, management commentary during earnings calls (if applicable), and notable PIPE (Private Investment in Public Equity) financing commitments accompanying announced deals.

Within such frameworks, closure prerequisites will involve due diligence rigor, negotiation on valuation terms, shareholder vote authorizations adhering to regulatory stipulations, and aligning warrants exercise conditions conducive for funding gaps arising post-transaction closure. While OneIM's sponsor credentials have yet to be scrutinized through transaction execution performance metrics publicly, their stewardship capacity will pivotally determine realized value capture.

Critical Constraints: Timeline Pressure and Risk Considerations in SPAC IPOs

A central tension defining OneIM’s viability stems from the finite window mandated for deal completion—24 months following IPO closing (January 2028 deadline), extendable only under specific shareholder-approved amendments [S4],[S14]. This enforced 'time arbitrage' drives urgency among sponsors balancing exhaustive target vetting against accelerating deployment to avoid forced liquidation scenarios depriving markets of deal flow continuity.

Investor risk exposure thus concentrates on deal sourcing effectiveness compounded by varying market conditions influencing asset valuations during this horizon. Failure to consummate an initial business combination within stipulated dates compels trust fund reconveyance minus operational overheads back to shareholders—yielding essentially break-even outcomes devoid of post-deal upside participation.

Capital Allocation Prerogatives: Trust Funds, Warrants, and Sponsor Agreements

Capital stewardship remains firmly conservative given fiduciary obligations vested in trust account governance protocols [S8],[S9]. No dividends or share repurchases have been authorized or executed since IPO closure given absence of distributable earnings or excess liquidity outside escrowed funds [S5],[S6],[S13].

Warrants attached to units furnish asymmetric leverage potential upon successful acquisitions: exercisable at $11.50 per share—above initial unit pricing—warrant holders gain conversion optionality enhancing equity stakes if post-merger valuations exceed strike prices markedly. Sponsor agreements typically incorporate indemnities protecting new directors/officers while committing them to backstop certain underwriting discounts evidenced by deferred fee arrangements totaling ~$15.8 million thereby impacting net cash initially available [S11],[S12].

The blending of these elements sustains disciplined capital deployment while pacing incentive alignment across management and public investors ahead of deal closure.

Expected Milestones and Watchpoints: What Investors Should Monitor Next

Absent explicit forecasts or scheduled deal announcements at present, key sentinel events for OneIM’s trajectory will concentrate on:

- Public declarations of identified acquisition candidates or signed definitive agreements,

- Timing convening shareholder meetings for vote ratification of proposed business combinations,

- Execution progress related to PIPE financing rounds supplementing transaction funding,

- Market sentiment shifts reflected through warrant exercise trends,

- Potential amendments adjusting transaction deadlines subject to shareholder approval mechanisms.

Surveillance around these inflection points informs reevaluation prospects underpinning valuation reactions typical within SPAC investment cycles.

Historical Summary Table: Capital Raised, Net Income, ROE Trend Post-IPO

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

*Note: Capital Raised includes IPO gross proceeds plus private placement; ROE unusually high due to nominal equity base combined with small net loss; Trust balance approximates total proceeds held in escrow excluding nominal interest earned.

This analysis synthesizes OneIM Acquisition Corp.'s inception phase parameters buttressed by detailed SEC filings reflecting foundational transaction structures customary among newly formed SPACs in early 2026. The company's ultimate value realization hinges on management's ability to orchestrate timely business combination(s) that resonate with shareholder interests amid prevailing market dynamics characteristic of post-pandemic capital markets activity levels.

Disclaimer: This report presents analytical observations based solely on publicly available filings without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments