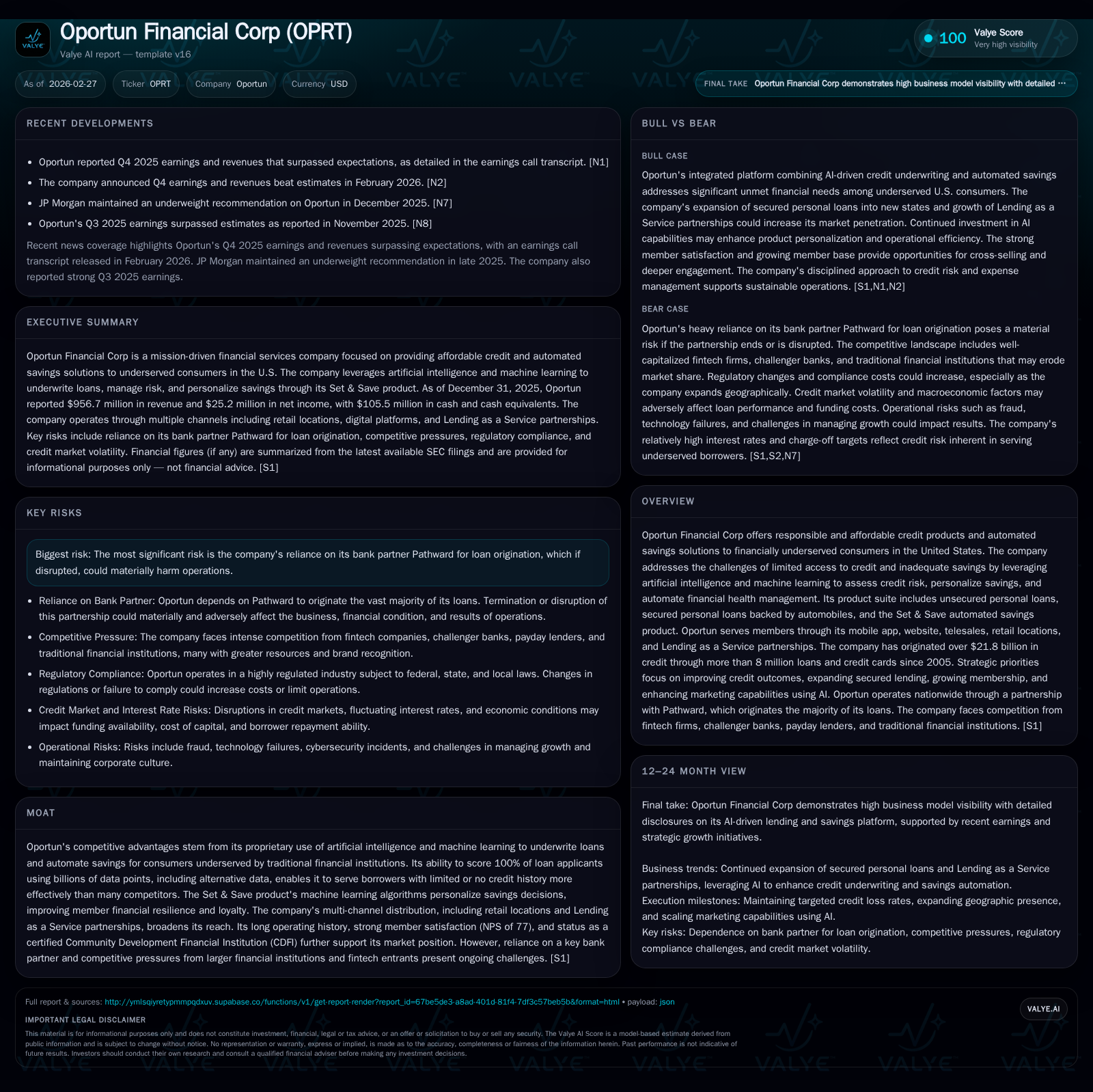

Oportun Financial Corp's 2025 Profit Turnaround and AI-Driven Credit Expansion Amid Funding Dependencies

Oportun Financial Corp reversed prior losses with positive net income in 2025, driven by AI-powered lending growth and disciplined cost management, while maintaining robust liquidity supported by securitizations and secured financing.

Oportun Financial Corp reported a rebound to $25.2 million net income in 2025 from multi-year losses, supported by steady revenue near $957 million and strong operating cash flow exceeding $413 million [F1]. The company’s AI-driven platform continues to enable access to responsible credit and automated savings solutions serving underserved U.S. consumers [S1]. Operating expenses declined materially in 2025, reflecting efficiency gains even as sales and marketing investments rose modestly [S1]. Liquidity remains ample with approximately $1.18 billion available combining cash, secured financing, and other facilities [S6]. However, Oportun depends on its bank partner Pathward for loan origination and faces exposure to capital market conditions affecting asset-backed securitizations critical for funding [S13]. Future growth hinges on expanding secured loans geographically, sustaining credit performance amid macroeconomic uncertainty, and advancing technology-driven member engagement [N1][S1].

Executive Summary

Oportun Financial Corp (OPRT) delivered a marked turnaround in fiscal year 2025, recording net income of $25.2 million compared to multi-year losses surpassing $78 million in FY2024 [F1]. Revenue declined modestly by 4.5% year-over-year to approximately $957 million but showed stabilization relative to more volatile prior years. The company’s AI-powered platform supports lending products tailored for financially underserved U.S. consumers—offering unsecured personal loans, secured auto-backed loans, and an automated savings product called Set & Save that personalizes savings through machine learning algorithms [S1]. This integrated approach advances Oportun’s mission to improve members’ financial health.

Liquidity remains strong with over $1.17 billion available including cash reserves, restricted cash earmarked for securitization payments, and undrawn secured financing lines totaling about $934 million [S6][S9]. The firm’s senior secured term loan of $235 million bears a relatively high interest rate (~15%) but extends maturity into late 2028 providing capital structure stability during market fluctuations [S10][S12]. Despite these strengths, Oportun's business continuity is closely linked to its bank partner Pathward’s role as exclusive originator until recently; now Oportun purchases all originated loans starting October 2025—a shift imposing balance sheet funding demands but consolidating operational control over the portfolio [S13].

Historical Performance: Trends

Oportun's revenue from FY2022 through FY2025 reflects cyclical pressures typical of subprime lending but features a pivotal inflection point in profitability (Table below). Revenues peaked near $1.057 billion in FY2023 then declined alongside elevated credit loss reserves during broader economic challenges.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 957 | 25 | 413 | -4.5% | +132.1% |

| 2024 | 1002 | -79 | 394 | -5.2% | +56.3% |

| 2023 | 1057 | -180 | 393 | +11.0% | -131.5% |

| 2022 | 953 | -78 | 248 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 6.5 | |

| 2024 | -22.2 | |

| 2023 | 28000 | -44.5 |

| 2022 | 28000 | -14.2 |

Source: SEC companyfacts cache [F1].

Net losses during earlier years primarily resulted from elevated net charge-offs around an annualized rate of approximately 12%, consistent with their target risk tier but indicative of ongoing economic headwinds affecting borrower repayment behavior [S1]. Improvements in FY2025 were driven by tighter underwriting supported by advanced AI/ML risk models analyzing extensive data sets including alternative sources—enabling more precise risk assessment among borrowers lacking traditional credit histories.

Operating expenses moderated notably after peak prior periods. Technology & facilities expenses alone dropped over $23 million or about -14.3% year-over-year due to optimized amortization schedules for internal software development and cost reductions from branch consolidations as well as lower outsourcing fees [S1]. Conversely sales & marketing costs increased about +5.4%, aligned with efforts to sustain membership growth amid challenging market conditions.

Business Model and Products

Oportun addresses urgent needs among Americans lacking sufficient savings or affordable credit—more than half reportedly unable to cover unplanned expenses above $1000 according to company-cited surveys [S1]. Lending products feature fixed-rate unsecured installment loans averaging around $3,100 originated across more than forty states primarily via the Pathward channel alongside secured auto-backed loans averaging roughly twice that amount offered currently in eight states with plans for further expansion [S1].

The Set & Save automated savings product uses machine learning algorithms assessing users’ cash flows at a granular level enabling customized incremental savings without harming daily liquidity—reinforcing financial resilience while fostering customer loyalty evidenced by an NPS score near an industry-leading 77 for personal loans [S1].

Member acquisition employs multi-channel strategies centered on mobile apps supplemented by call centers plus about 126 retail stores alongside over four hundred Lending as a Service partner locations extending reach into underserved communities nationwide.

Capital Structure and Liquidity

Funding relies heavily on asset-backed securitizations totaling over $2.2 billion outstanding across multiple series issued predominantly through calendar year 2025 priced between roughly 5.2% to just under 7% annual yield depending on tranche seniority [S4][S18]. Warehouse lines aggregate approximately $1.14 billion capacity with about $205 million drawn year-end while maintaining nearly $930 million undrawn providing runway for originations assuming stable collateral performance within covenant limits.

Corporate financing includes a senior secured term loan totaling $235 million at an effective annual rate near fifteen percent incorporating both cash pay and payment-in-kind elements maturing November 2028—repaying prior facilities early accompanied by partial prepayments reducing principal obligations lowering future interest expense relative to historical peaks before these refinancings [S10][S12][S14]. Covenants remain fully complied with per audited disclosures.

Operating cash flow exceeded $413 million coupled with restrained capex spending yields estimated free cash flow around $407 million supporting internal funding for growth without dilutive equity issuance or excessive debt beyond structured programs already managed prudently.

Risks: Bank Partner Dependence and Market Access

Key risks include dependence on Pathward Bank which originates most loan volume under contracts amended late FY2025 requiring Oportun purchase nearly all new originations transitioning away from previous arrangements where Pathward retained portions of loan books—transferring funding responsibility significantly onto Oportun’s balance sheet necessitating scalable liquidity management practices going forward [S13]. Disruptions or termination could materially impair originations impacting top line growth.

Secondary market pressures inherent in asset-backed note issuances impose covenant thresholds based on portfolio delinquency preventing unfettered access during stress which could constrain capital availability during adverse macroeconomic phases exacerbating refinancing risks especially if unsecured credit spreads widen or investor appetite diminishes disrupting key funding conduits vital for continuous lending consistent with fintech subprime lending dynamics broadly exposed cyclically.

Outlook: Growth Drivers and Priorities

Looking ahead the company emphasizes advancing credit outcomes via proprietary AI; scaling secured personal loan offerings geographically beyond eight states targeting vehicle-secured consumer credit niche attractive due to collateral mitigating downside risk; growing digital membership via app-based channels synergistically through Lending as a Service partnerships retaining cost efficiencies while broadening reach; plus sharpening operational effectiveness maintaining flat or slightly reduced operating expense ratios against revenue enhancing investments particularly within technology underpinning machine learning algorithmic enhancements sustaining competitive moats derived from data scale advantages difficult for new entrants replicating [N1][S1].

Credit stability indicators show slight net charge-off declines coinciding with reduced outstanding principal balances balanced against unchanged annualized charge-off rates near twelve percent warranting vigilance given macroeconomic uncertainties such as inflation pressures influencing repayment capacity while spread compression may limit margin upside absent tactical pricing or collateral value expansions typically constrained legally.

No formal guidance was explicitly reconfirmed during latest earnings call or filings indicating constructive yet cautious management tone signaling watchfulness regarding organic volume increments dependent partially upon macro-credit cycles shifting regulatory landscapes impacting fintech banking collaborations plus competitive pressure evolving rapidly within alternative lending fintech ecosystem shaped increasingly by augmented intelligence deployments underpinning credit decision effectiveness ultimately determining franchise sustainability subject systemic economic variables outside direct company control presently disclosed.

Returns and Capital Allocation

Return on equity recovered from negative territory registering approximately six-point-five percent based on trailing net income relative to book equity at fiscal end illustrating nascent profitability stabilization albeit modest scale suggesting room for optimization across revenue leveraging versus fixed cost structures demanding continuous prudent balance sheet stewardship paired with vigilant credit risk management coordinating origination quality controls portfolio servicing maturity diversification measures coupled tightly with conservative allowance provisioning adapting dynamically informed iteratively through real-time predictive analytics embedded within operational frameworks powered by company-owned technology deployed nearly two decades conferring structural competitive advantage beyond commoditized fintech models focused narrowly on marginal returns absent holistic financial health improvement imperatives articulated clearly within corporate mission emphasizing social impact fused integrally alongside commercial objectives thus positioning differently strategically relative peer group participants focused narrowly upon maximum throughput philosophies common elsewhere.

No significant share buybacks occurred recently nor indicated prospectively highlighting preservation focus likely toward deploying free cash flows preferentially toward strengthening liquidity buffers increasing scale organically possibly supplemented selectively by accretive acquisitions if opportunistic though no definitive targets disclosed explicitly aligning conservatively managing capital returns prioritizing sustainable growth preserving long-term access advantages developed within niche lending domains aimed sustainably serving historically underserved segments representing sizable opportunity well into forthcoming decade horizons.

This analysis integrates detailed SEC filings including latest Form 10-K for fiscal year ended December 31, 2025 alongside select earnings transcripts announced February 27th contextualizing financial performance beneath stated operational strategies without extrapolating undisclosed forward guidance or investment opinions. All figures derive directly from referenced primary sources ensuring accuracy respecting Valye News analytical standards.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments