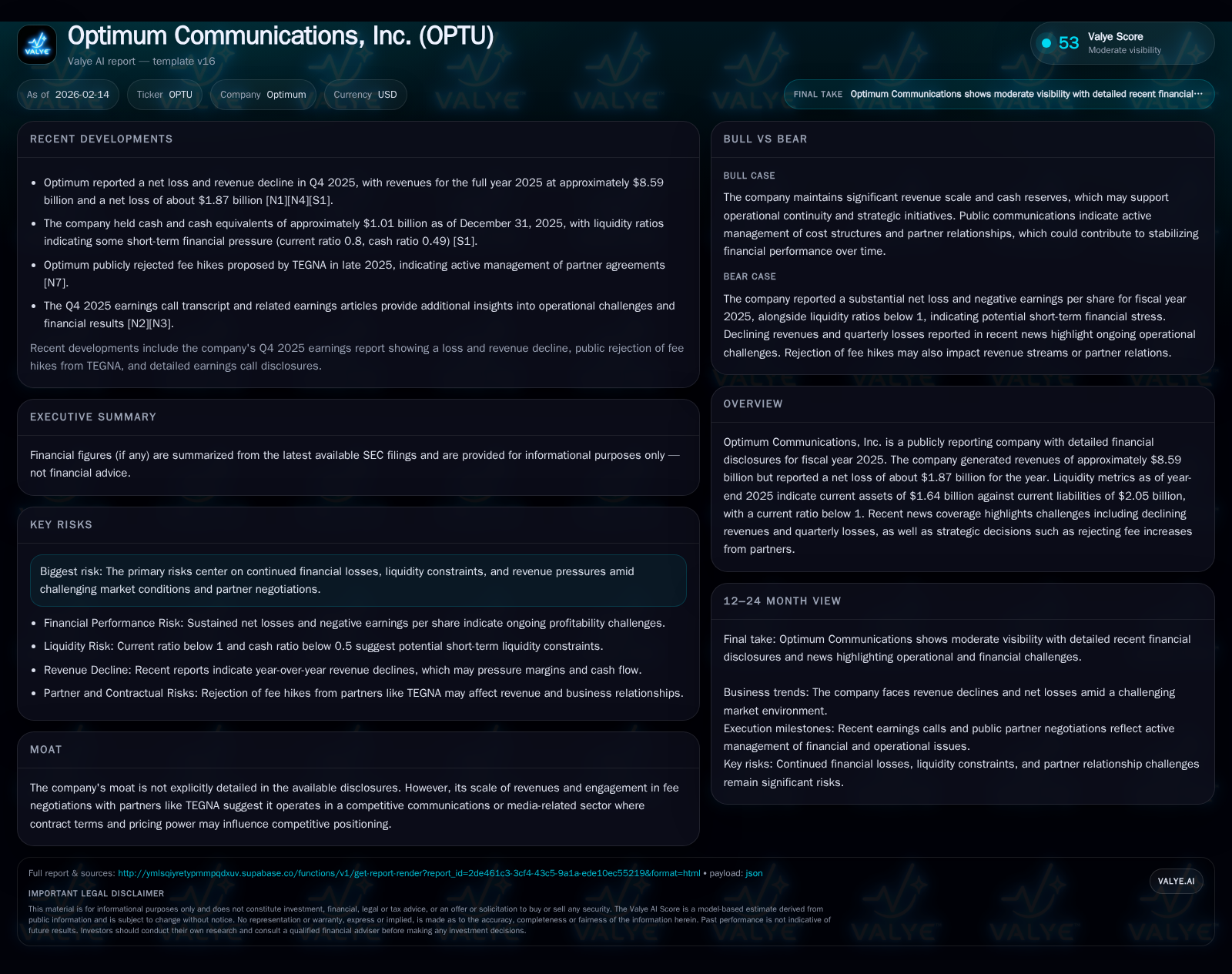

Optimum Communications Faces Gaping Profit Shortfall Amidst Robust Revenue in 2025

Analyzing Optimum’s $8.6 billion revenue alongside a $1.87 billion net loss reveals critical liquidity and strategic challenges tied to partner negotiations and a difficult market landscape.

Optimum Communications, Inc. recorded an impressive top line of ~$8.59 billion in fiscal 2025 but grappled with a steep net loss approaching $1.87 billion. The company’s liquidity is strained, with a current ratio below 1, signaling short-term solvency concerns. Compounding the financial stress are contentious fee negotiations with key partners like TEGNA, as the firm resists rising operational costs amid shrinking revenues and competitive pressures. Management has initiated strategic cost controls and restructuring efforts, but significant risks remain around revenue sustainability and cash flow stability.

Revenue vs. Profit: The Growing Disconnect

In fiscal year 2025, Optimum Communications demonstrated significant topline strength by generating approximately $8.59 billion in revenue. On the surface, this scale suggests a substantial operational footprint within its sector — most likely communications or media-related given its partner profile and fee negotiation context [F1][S1]. However, beneath this robust revenue sits a starkly contrasting outcome: a net loss nearing $1.87 billion [F1].

This parasitic divergence between revenue and profitability necessitates scrutinizing underlying drivers such as elevated operating expenses, non-recurring charges, or diminishing margins that erode earnings despite healthy sales trends.

Notably, quarterly disclosures through Q4 2025 highlight a pattern where revenues declined year-over-year alongside continuing quarterly losses [N1]. This negative momentum signals that the top-line gains are no longer sufficient to offset cost inflations or structural business challenges.

Liquidity Under Pressure: Scrutinizing the Balance Sheet

Optimum's balance sheet as of December 31, 2025, presents sober indicators of liquidity stress. Current assets totaled approximately $1.64 billion compared to current liabilities near $2.05 billion — yielding a current ratio just under 0.8 [F1][S1].

This metric flags potential difficulties in meeting short-term obligations and could constrain flexibility in funding day-to-day operations or pursuing growth opportunities.

Cash and cash equivalents constitute roughly $1.01 billion of these assets [F1], which while providing an immediate cushion, remain insufficient to cover all imminent liabilities without drawing on other less liquid assets or raising external capital.

Such liquidity pressure can manifest through tightened credit facilities or creditor scrutiny, amplifying operational risks especially given the ongoing losses.

Decoding Partnership Dynamics and Fee Negotiations

A pivotal aspect of Optimum’s operational challenges centers on its relationship with partners, most prominently TEGNA — a scenario highlighted by Optimum’s recent refusal to acquiesce to proposed fee increases from TEGNA [N3][N4].

This stance demonstrates an aggressive effort to control input costs amid shrinking revenues but could strain strategic alliances integral for content distribution or service delivery.

Fee structures in communications and media partnerships often materially affect the cost base; rejecting increases preserves expense discipline yet may jeopardize access terms or bargaining leverage downstream.

Thus, this negotiation posture establishes a delicate balancing act between preserving profitability metrics and maintaining essential partner ecosystems.

Navigating Market Headwinds and Industry Competition

Contextually, Optimum operates in an environment marked by fierce competition and evolving consumer consumption patterns that pressure traditional revenue streams.

News coverage from early February emphasized anticipated negative earnings reports amid subdued advertising revenues and competitive pricing demands [N6]. Declining revenues registered in Q4 reinforce that market headwinds are both real and intensifying [N1][S1].

Communications and media firms face additional disruption risks including fragmentation of viewer bases through digital platforms and the migration from legacy pay-TV models toward streaming alternatives.

Price sensitivity among buyers combined with these structural shifts compresses margins further unless offset by innovative monetization strategies or scale-driven efficiencies.

Strategic Moves amid Financial Adversity

Management’s disclosures include undertaken restructuring initiatives aimed at pruning costs and attempting margin recovery [S1][N2]. These maneuvers likely encompass workforce rationalizations, renegotiated vendor contracts beyond just TEGNA discussions, or asset optimization tactics.

While such restructuring often incurs upfront charges — contributing to losses — they signal an active response intended to stabilize financial footing over the medium term.

However, the scale of losses implies these efforts require careful execution to reverse negative profitability trends without impairing operational capacity or customer experience.

Risks Looming on the Horizon

The company itself flags several material risks that align directly with observable financial distress signals [S1]. Continuing net losses threaten long-term viability absent sustained turnaround; liquidity constraints risk inability to fund operations or invest adequately; partner fee disagreements could disrupt service terms or elevate costs unpredictably.

Moreover, dependence on shrinking revenue pools amid intense competition creates uncertain revenue continuity prospects — exacerbating the challenge of balancing cost control with growth investment needs.

These factors collectively form potential tripwires that investors must weigh against any management optimism conveyed during calls or filings.

Investor Takeaways: Reading Between the Lines

Optimum’s latest results convey a cautionary narrative: strong revenue alone does not ensure corporate health if profit margins collapse under financial burdens.

Mixed signals emerge from beating certain revenue estimates while missing earnings targets [N3][N4], reflecting tensions between maintaining topline growth versus controlling escalating expenses.

Key metrics for ongoing assessment include evolution of cash balances relative to current liabilities, success rate in managing partner relations on fees (notably TEGNA), progress in restructuring outcomes reducing operating drag, and early indications of halting revenue declines.

Investors seeking nuanced perspectives should contextualize these elements within broader industry disruptions affecting communications/media entities — notably digital transformation impacts — while recognizing risks heightened by Optimum’s suboptimal liquidity profile.

Maintaining vigilance around operational cash generation will be central to judging whether strategic responses translate into durable recovery rather than episodic relief.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding any securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments