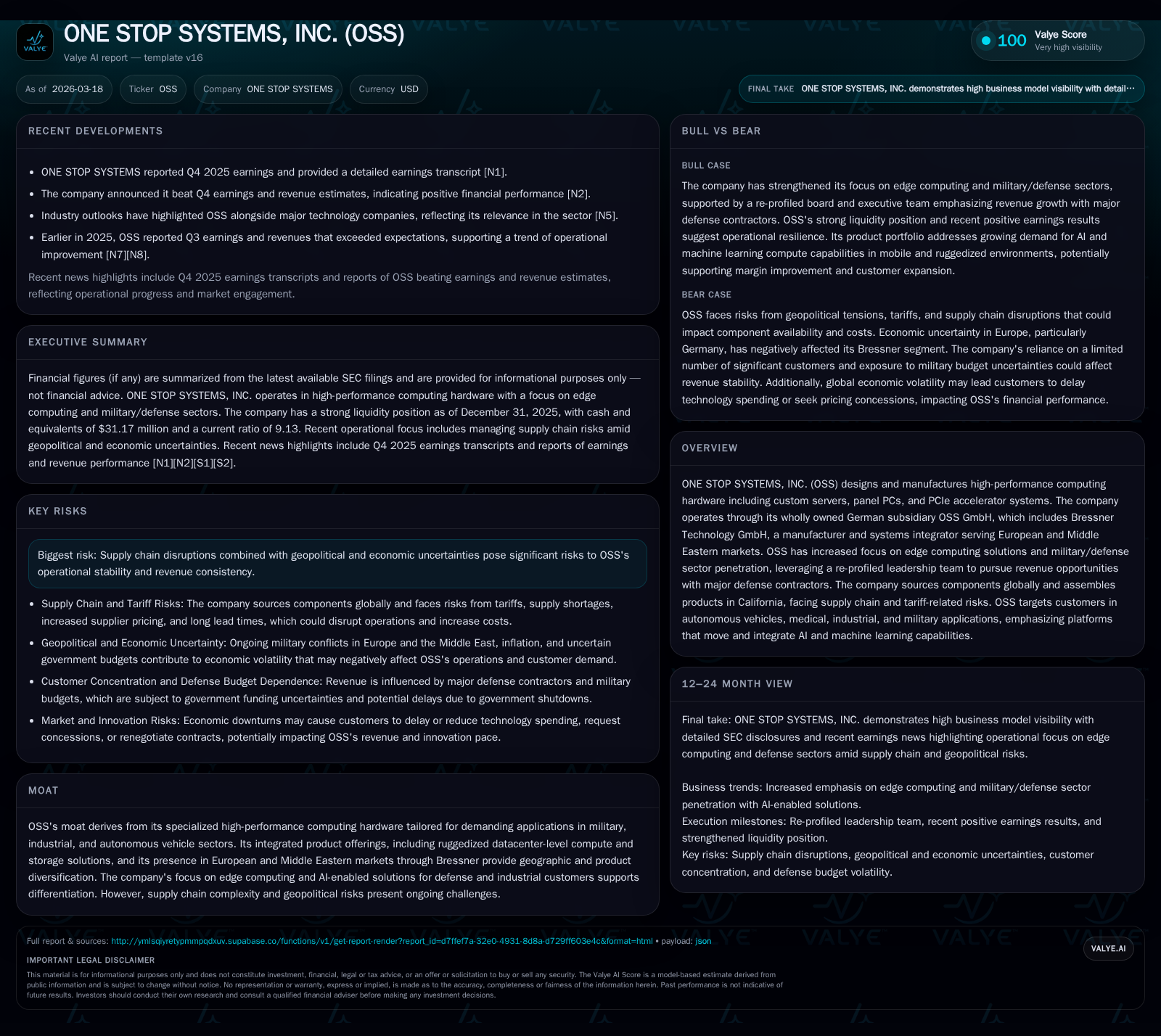

ONE STOP SYSTEMS Reverses Operating Losses with Defense Sector Focus and Edge Computing Expansion

OSS advances in customized high-performance computing hardware amid supply chain and geopolitical pressures.

ONE STOP SYSTEMS, INC. (OSS) designs and manufactures specialized high-performance computing solutions tailored for demanding industrial, military, and autonomous vehicle markets. After several years of operating losses, the company reported a sizable net income turnaround in fiscal 2025 supported by restructuring efforts, defensive sector penetration, and product innovation focused on edge AI compute platforms. OSS faces ongoing supply chain complexity and tariff uncertainties but leverages its geographic diversification through its German subsidiary Bressner Technology GmbH to serve European and Middle Eastern clients. Capital allocation remains conservative with low capex and no material debt drawn on U.S. revolving credit lines as of late 2025.

Company Overview

One Stop Systems, Inc. (OSS) engineers and manufactures high-performance computing hardware solutions centered on custom servers, rugged panel PCs, and PCIe accelerator systems optimized for computationally intensive applications. Its clientele spans industries such as military/defense, autonomous vehicles, medical devices, and industrial automation sectors where durability and cutting-edge compute capabilities are mission critical [S1][S5].

A key structural element is OSS's wholly owned German subsidiary OSS GmbH, which includes Bressner Technology GmbH—a manufacturer of standard and bespoke compute hardware serving Europe's defense and industrial markets as well as broader Middle Eastern territories. Bressner acts as a strategic channel to market for OSS's rugged datacenter-level storage and computing products beyond North America [S13][S15].

Since 2023-24, OSS has intensified its emphasis on edge computing platforms integrating artificial intelligence (AI) and machine learning (ML) processing functions aimed at military-grade applications. This focus coincides with leadership refreshes at the board and executive levels designed to heighten engagement with major defense contractors seeking embedded tactical compute systems [N1][S5].

Historical Performance Trends

OSS experienced a challenging operational landscape over recent years characterized by persistent losses largely resulting from higher costs linked to supply-chain issues, inflationary pressures, tariff impacts, and slower recovery in European economies especially affecting Bressner's segment [F1][S7]. The table below summarizes relevant financial metrics from fiscal year ends 2022 through 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 5 | -3 | 114596 | +137.3% | |

| 2024 | -14 | 0 | -13 | 362748 | -103.0% |

| 2023 | -7 | 0 | -8 | 821753 | -201.3% |

| 2022 | -2 | -8 | 2 | 529908 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 11.1 | |

| 2024 | 0 | -50.2 |

| 2023 | -1 | -17.0 |

| 2022 | -8 | -5.0 |

Source: SEC companyfacts cache [F1].

Revenue figures over this period are not captured here explicitly but internal sources indicate steady activity disrupted by supply constraints [F1][S11]. Although operating income remained negative through these years—peaking at a loss exceeding $13 million in FY24—operating loss shrank materially in FY25 alongside a positive net income swing of approximately $5 million[F1]. This reflects operational improvements possibly driven by cost control measures and an increased product mix contribution from higher-margin defense contracts.

Operating cash flows showed significant improvement from deep negative outflows in prior years moving closer to breakeven by FY24 but did not fully turn positive by end FY25 [F1]. Capital expenditures declined sharply in FY25 indicating cautious reinvestment aligned with tightened cost discipline.

Growth Drivers & Strategic Focus

OCI's future growth prospects hinge upon several pivotal initiatives:

- Edge Computing with AI/ML Integration: OSS targets emerging demands where AI-enabled sensor fusion capabilities at the network edge are critical—such as unmanned vehicles or mobile command centers—leveraging its expertise in ruggedized high-performance hardware [N1][S5].

- Defense & Military Sector Penetration: A repositioned leadership team has prioritized revenue pursuits with major defense contractors who require robust compute platforms able to operate under austere conditions. This sector focus provides differentiation versus commodity server markets [N1][S5].

- Geographic Diversification via Bressner: Serving Europe and the Middle East offers access to key governmental contracts but also exposes OSS to macroeconomic volatility in these regions including geopolitical instability impacting budgets [S7][S14].

- Supply Chain Optimization: Although supply chain disruptions have somewhat eased recently after lengthy component shortages and price escalations they remain a risk factor due to global trade policy uncertainties including ongoing U.S.-China tensions affecting tariffs on imported components [S4][S12].

Potential caps on growth include sustained adverse tariff environments limiting pricing flexibility; prolonged recessionary conditions curtailing defense spending or OEM demand; and competitive pressure from larger system integrators increasing R&D costs.

Forecasts & Operational Milestones

OSS has not issued explicit revenue or earnings guidance within the latest disclosures but outlines optimistic views around order pipelines relating to defense contracts expected to manifest into near-term revenue increases consistent with their strategic realignment [N1][S5]. Milestones include expanding deployment of edge AI compute platforms validated by engineering wins within military programs although timelines remain subject to funding uncertainties inherent in governmental procurement cycles [N1][S7].

From an operational perspective,the trajectory toward margin expansion will be closely tied to successfully scaling production efficiency while maintaining technology leadership for ruggedized customized systems adapted for mission-critical applications.

Returns & Capital Allocation

The company reported an estimated return on equity of approximately 11% for FY25 driven by the swing into net profitability despite operating losses persisting at roughly -$3.4 million indicating non-operating gains or tax benefits contribute positively [F1].

Cash flow management remains prudent:

- Year-end cash & equivalents total roughly $31.2 million providing significant liquidity buffer.

- The current ratio stands above nine times current liabilities signaling strong short-term financial health [F1].

- Capital expenditures fell sharply in FY25 (down nearly 70% year-over-year), aligning with cash conservation strategies amid uncertain demand cycles.

- No dividends or buyback programs have been declared recently; capital allocation appears focused on bolstering product development investments balanced against strict cost controls [S23].

OSS carries limited debt principally through two German term loans held by Bressner totaling approximately $1.17 million USD equivalent maturing mid-2026 along with access to $2 million domestic revolving credit line currently drawn minimally [S18][S22]. Interest rates on these borrowings vary between Euribor + spread (~3.7%-6.5%) reflecting standard commercial lending terms in Europe.

Market & Industry Context Analysis

The high-performance computing hardware sector servicing edge AI/machine learning workloads is becoming increasingly specialized especially for defense applications where ruggedness combined with computational density is paramount. While large hyperscale cloud providers dominate general-purpose server markets commoditized by volume economics two distinct niches foster continued opportunities for small-cap specialized players like OSS:

- Embedded systems requiring certification compliance for military/aviation standards,

- Edge compute modules that must operate reliably under extreme environmental stress.

Competitors typically include established embedded system vendors plus newer entrants focusing on accelerated computing cards leveraging latest GPUs or FPGAs tailored for inference workloads.

Global supply chain dynamics remain volatile with constraints on semiconductor availability having shifted buyer strategies toward longer lead times or dual sourcing — both adding inventory carrying risks plus complexity that favor smaller firms adept at customization over scaled volumes.

Trade policy uncertainties—especially tariff regimes associated with U.S.-EU-China interactions—heighten component cost pressure forcing further R&D investments just to maintain competitive positioning.

Finally,the defense sector remains cyclically dependent on government budget appropriations influenced by geopolitical developments such as ongoing conflicts in Eastern Europe or Middle East that directly impact contract awards timing.

Conclusion

ONE STOP SYSTEMS has navigated several challenging years marked by heavy operating losses under macroeconomic headwinds yet achieved a meaningful turnaround in profitability during FY25 attributable to tighter management focus on defense-related edge computing offerings supported by its European footprint via Bressner GmbH. The company sustains strong liquidity reserves while pursuing incremental revenue growth through embedded AI compute solutions specifically designed for demanding environments across military and industrial domains.

Key risks persist due to ongoing volatility in component supply chains combined with shifting tariffs and geopolitical uncertainty risking capital expenditure deferment among customers as well as procurement delays particularly within government contracts. Monitoring upcoming contract awards along with macroeconomic indicators will be critical gauges of OSS's ability to sustain its improved earnings trajectory going forward.

This report is based solely on publicly available information including regulatory filings filed up through March 18th, 2026 ([F1], [N1]-[N4], [S1]-[S29]) without any projection or investment advice offered herein. Care was taken to cite facts verbatim where possible rather than infer speculative financial assumptions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments