Perceptive Capital Solutions’ De-SPAC Path Faces Liquidity and Redemption Challenges

Focused on healthcare, Perceptive Capital Solutions aims to complete its initial business combination while navigating shareholder redemptions and trade policy risks.

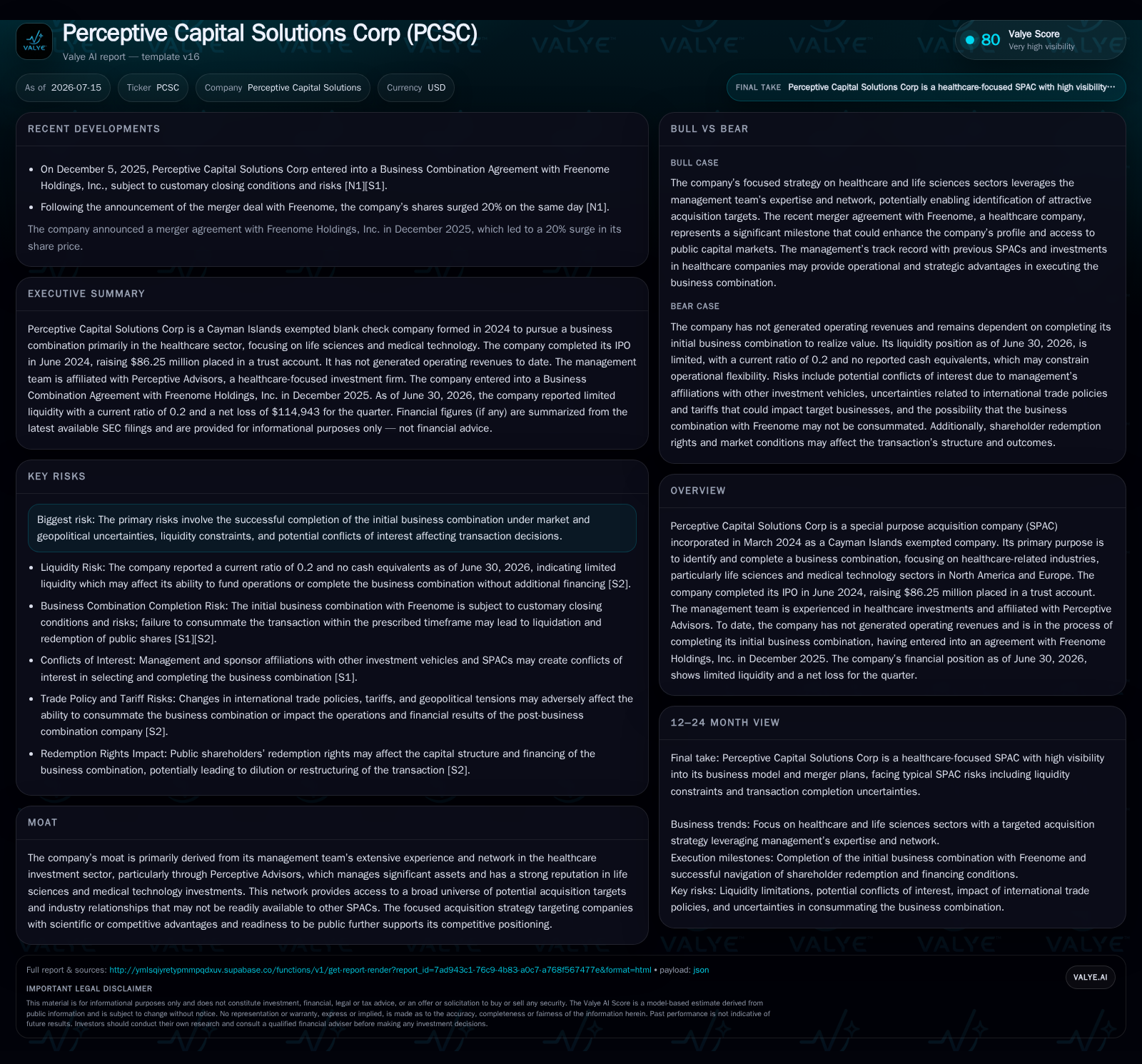

Perceptive Capital Solutions Corp (PCSC) is a SPAC formed in 2024 with a $86.25 million trust account, targeting life sciences and medical technology companies in North America and Europe. It entered a business combination agreement with Freenome Holdings in late 2025, aiming for consummation in 2026, but faces liquidity constraints and shareholder redemption dynamics that complicate deal execution. The company also confronts external risks including international trade policy shifts that could affect target viability and capital raising. Its management team’s sector expertise provides a credible platform, yet successful deal completion and post-merger integration remain key watchpoints.

Latest Operating Update: Business Combination Progress Amid Liquidity Challenges

Perceptive Capital Solutions Corp (PCSC) remains on track to complete its initial business combination following its June 2024 IPO, which raised $86.25 million placed in a trust account dedicated to acquisition funding and shareholder redemptions [S1]. The company entered into a definitive merger agreement with Freenome Holdings, a Delaware-based life sciences company specializing in early cancer detection technologies, in December 2025, with an anticipated closing in the first half of 2026 [S1]. However, as of the latest quarterly filing dated July 15, 2026, the transaction awaits shareholder approval and regulatory clearances [S2].

The Extraordinary General Meeting (EGM) originally scheduled for early July 2026 was postponed to July 15, 2026, with the deadline for shareholder redemption demands extended to July 13, 2026 [S3]. This postponement reflects the complexities in securing sufficient shareholder votes and managing redemption requests, which directly impact the liquidity available to fund the business combination. Shareholders retain redemption rights allowing them to redeem their shares for a pro rata portion of the trust account, thereby reducing the cash available for the acquisition and increasing the reliance on alternative financing sources such as PIPE (private investment in public equity) financing [S3].

Financially, PCSC is experiencing significant liquidity constraints outside the trust account. As of June 30, 2026, current assets stood at approximately $742,000 against current liabilities of $3.63 million, resulting in a current ratio of roughly 0.2, indicating limited short-term liquidity coverage for operational and administrative expenses [F1]. It is important to note that the trust account funds, which are restricted and earmarked exclusively for the business combination or shareholder redemptions, are not included in these current assets. The reported liabilities likely reflect accrued transaction costs, legal fees, and other expenses incurred during the search and due diligence process [F1].

Business Model and Sector Focus: SPAC Mechanics in Healthcare

PCSC operates as a Special Purpose Acquisition Company (SPAC), a publicly traded blank-check entity formed to raise capital through an initial public offering (IPO) with the sole purpose of effecting a business combination that takes a private company public without a traditional IPO process [S1]. The $86.25 million raised in the IPO was placed in a trust account to be used exclusively for the acquisition or returned to shareholders upon redemption or liquidation [S1]. Until the de-SPAC transaction closes, PCSC generates no operating revenues and incurs costs related to search, due diligence, and transaction execution.

The company’s management team, affiliated with Perceptive Advisors—a healthcare-focused investment firm managing over $9.5 billion in assets as of December 31, 2025—leverages deep sector expertise in life sciences and medical technology to identify acquisition targets primarily in North America and Europe [S1]. This strategic focus aims to capitalize on innovation cycles in diagnostics, therapeutics, and medical devices, sectors characterized by complex scientific evaluation and regulatory pathways.

Revenue generation and cash flow will commence only after the successful completion of the business combination, when the acquired company, Freenome in this case, becomes a publicly traded operating entity [S1]. Until then, PCSC’s financial performance depends on managing capital deployment, controlling transaction-related expenses, and navigating shareholder redemption dynamics. Key operating variables include the amount of capital retained post-redemptions in the trust account, the ability to secure PIPE financing to supplement acquisition funds, and the timing of shareholder votes and regulatory approvals

Industry Context: Healthcare-Focused SPACs and Competitive Positioning

Healthcare-focused SPACs like PCSC have attracted investor interest due to their specialized management teams capable of evaluating complex scientific and regulatory risks inherent in life sciences targets. Comparable SPACs in this niche include Health Assurance Acquisition Corp and Foley Trasimene Acquisition Corp, which have completed de-SPAC transactions in medical technology and biotech sectors. These peers similarly leverage sector expertise to source targets and navigate the challenging valuation and approval processes typical in healthcare deals.

However, the SPAC industry faces several headwinds, including increased regulatory scrutiny on disclosures, rising shareholder redemption rates amid volatile capital markets, and valuation uncertainties driven by scientific and clinical development risks. PCSC’s affiliation with Perceptive Advisors provides a competitive advantage through access to proprietary deal flow and deep sector knowledge, which can enhance due diligence quality and target selection. Nevertheless, PCSC’s IPO size is modest relative to some larger healthcare SPACs, potentially necessitating substantial PIPE financing to close the Freenome transaction if redemptions are significant [S1].

Growth Drivers and Market Dynamics

PCSC’s potential growth hinges on successfully consummating the Freenome merger, which would transition the company from a blank-check vehicle to an operating public entity with revenue-generating capabilities. The healthcare and life sciences sectors continue to attract investor interest due to ongoing innovation in diagnostics, therapeutics, and medical technologies, areas where Freenome’s early cancer detection platform is positioned.

Investor appetite for alternative public listing routes, such as SPACs, remains robust in healthcare, driven by the desire for faster access to public capital markets and the involvement of experienced sector specialists. PIPE financing availability is a critical enabler, allowing SPACs to bridge funding gaps caused by shareholder redemptions and elevated target valuations. PCSC’s management team’s scientific and investment expertise enhances its ability to identify targets with strong clinical data and technological moats, which are key drivers of post-merger value creation [S1].

Risks and Watchpoints: Timing, Liquidity, and External Factors

PCSC faces several risks that could impede the successful completion of its business combination. The SPAC lifecycle imposes a strict deadline to consummate a transaction within 24 months of the IPO, failing which the company must liquidate or seek shareholder approval for an extension [S1]. Given that PCSC’s IPO closed in June 2024, this deadline is approaching, adding pressure to finalize the deal promptly.

Liquidity constraints outside the trust account, evidenced by a current ratio of 0.2 as of June 30, 2026, raise concerns about the company’s ability to cover ongoing administrative and transaction-related expenses without additional capital [F1]. Moreover, significant shareholder redemptions ahead of the EGM could reduce the effective acquisition capital below necessary thresholds, forcing reliance on PIPE financing or renegotiation of deal terms [S3].

External macroeconomic risks also weigh on PCSC’s prospects. Recent shifts in U.S. trade policies, including new tariffs and retaliatory measures by other countries, introduce uncertainty regarding supply chains, cost structures, and market access for healthcare targets with cross-border operations [S2]. These trade dynamics could affect the attractiveness and valuation of potential acquisition targets and complicate post-merger integration.

Governance risks inherent in SPAC structures, such as potential conflicts between sponsor incentives to complete deals and public shareholder interests, remain pertinent. Monitoring redemption patterns, shareholder vote outcomes, and PIPE financing commitments will be critical indicators of the transaction’s viability [S1].

Upcoming Milestones and What to Watch

The immediate focus centers on the Extraordinary General Meeting scheduled for July 15, 2026, where shareholders will vote on the Freenome business combination proposal [S3]. The volume of redemption demands submitted by the July 13 deadline will determine the net capital available in the trust account for closing the transaction

Subsequent announcements regarding PIPE financing commitments will be closely watched, as such financing is often essential to supplement trust funds when redemptions are material, especially in healthcare SPAC deals with elevated valuations [S1]. Regulatory approvals, including SEC review of disclosures and compliance with securities laws, remain critical prerequisites before the domestication of PCSC from a Cayman Islands exempted company to a Delaware corporation and the consummation of the merger [S1].

Finally, any board decisions to seek extensions beyond the original 24-month de-SPAC deadline would require shareholder approval and introduce additional execution risk and uncertainty [S1]. Operational cost management during this interim period will also be a key factor given the tight liquidity position outside the trust account.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Readers should consult primary sources and filings for detailed information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments