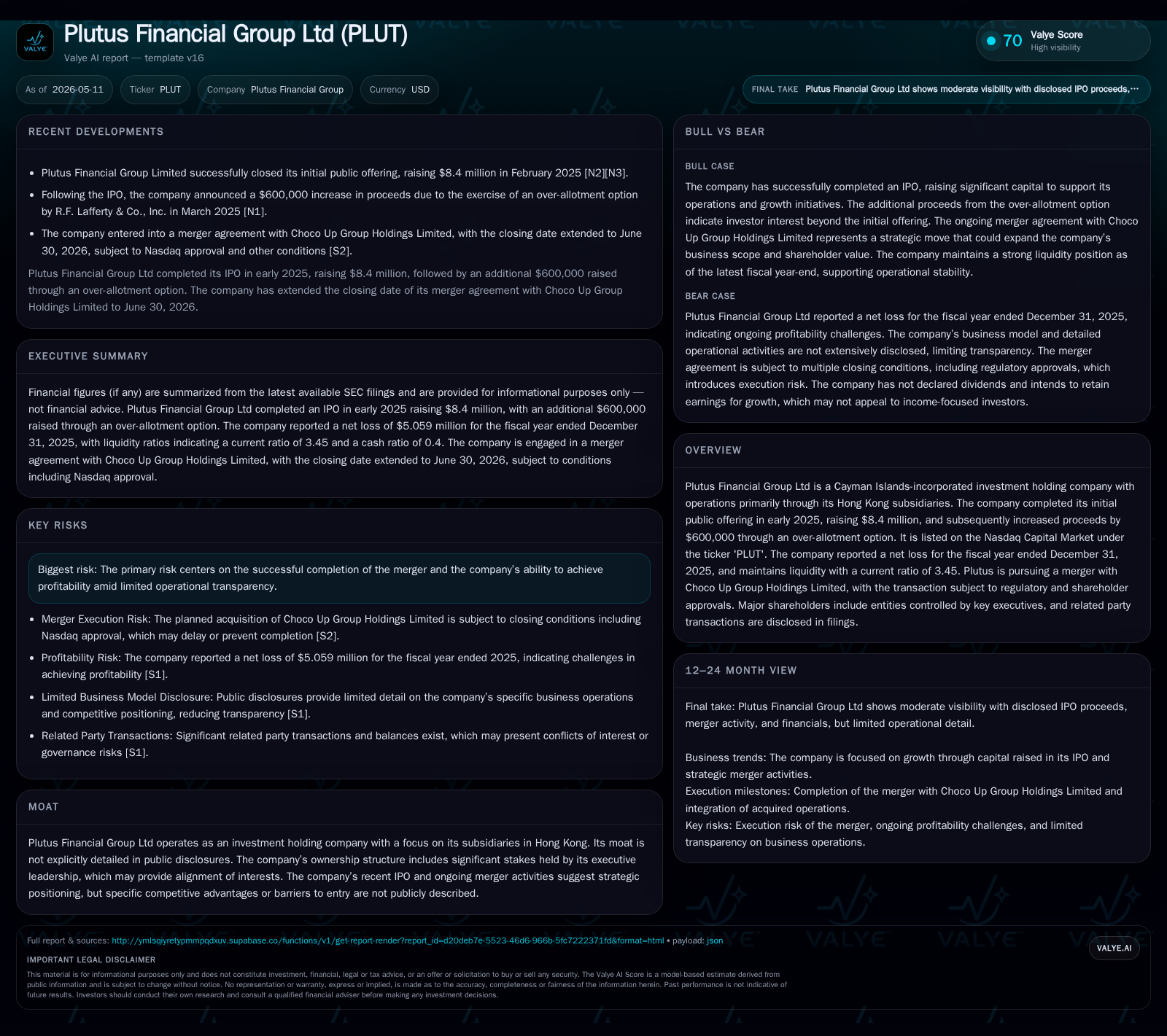

Plutus Financial Group Extends Merger Deadline Amid Ongoing Operating Challenges

The company navigates regulatory delays and operating losses while preparing for a transformative merger with Choco Up Group Holdings.

Plutus Financial Group Limited extended the closing deadline of its pending merger agreement with Choco Up Group Holdings Limited to June 30, 2026, reflecting continued regulatory review by Nasdaq. The company operates through its Hong Kong subsidiaries providing securities brokerage and asset management services under SFC licenses. Despite steady asset management fees, Plutus faces declining brokerage commissions and persistent operating losses driven by subdued market activity and increased legal costs. The merger aims to unlock growth opportunities and capital structure optimization but remains contingent on regulatory approval. Liquidity remains adequate to support ongoing operations during this period.

Recent Operating Update: Merger Deadline Extension

On April 1, 2026, Plutus Financial Group executed a Second Amendment to its Merger Agreement with Choco Up Group Holdings Limited, extending the transaction's Outside Date from March 31 to June 30, 2026 [S2]. This follows an earlier extension from the original December 31, 2025 deadline. The repeated extensions underscore ongoing regulatory scrutiny by Nasdaq and the complexities inherent in cross-border fintech mergers.

Management’s commitment to completing this transformative merger is evident despite operational headwinds and regulatory uncertainties. Completion will significantly alter Plutus’s capital structure through issuance of new Class A and B ordinary shares to Choco Up shareholders [S1]. However, final regulatory approval remains pending.

Business Model Overview: Brokerage and Asset Management in Hong Kong

Plutus operates primarily through two wholly owned subsidiaries based in Hong Kong: Plutus Securities Limited (licensed for Type 1 dealing in securities) and Plutus Asset Management Limited (licensed for Types 4 advising on securities and 9 asset management) [S1].

Plutus Securities delivers retail brokerage services via internet platforms, mobile apps, and phone hotlines for trading on the Hong Kong Stock Exchange. It also offers margin financing secured by listed securities collateral, securities custody and nominee services ensuring secure clearing and settlement processes. While underwriting and placing services were significant in prior years, no meaningful underwriting revenue has been reported since the IPO market downturn beginning in 2024 [S1][S10].

Plutus Asset Management provides professional funds management including discretionary accounts tailored to individual client risk profiles. Its investment offerings span real estate funds, fixed income products, private equity investments, and hedge funds. Revenue is generated from asset management fees as well as performance fees contingent upon exceeding high-water marks [S1][S10].

Revenue Trends and Financial Performance

Total revenues declined from HKD21.9 million in 2023 to HKD10.4 million (~$1.34 million USD) in 2025 due mainly to reduced brokerage commissions reflecting lower trading volumes and decreased interest income from margin loans [S1][F1]. Asset management fees remained relatively stable during this period but did not offset declines elsewhere.

Operating losses have widened with a net loss of approximately $5.06 million reported for fiscal year ended December 31, 2025 [F1], driven largely by elevated legal and professional expenses related to merger activities as well as subdued core business growth.

Competitive Landscape

Hong Kong's financial services sector is highly competitive with stringent regulation enforced by the Securities and Futures Commission (SFC). Brokers face pressure on commission rates amid industry digitization reducing entry barriers.

Plutus's scale remains modest relative to large incumbents or regional firms. Its competitive differentiation rests on service quality delivered through a network of independent account executives engaged under flexible perpetual contracts that foster client continuity but allow termination with notice [S1].

Margin lending demand has fluctuated notably; outstanding margin loans decreased from HKD15.9 million at end-2024 to HKD10 million at end-2025, impacting recurring interest income streams [S11].

The absence of IPO underwriting since early 2024 reflects challenging capital markets conditions affecting potential fee income.

Growth Drivers: Merger Synergies and Strategic Alignment

The pending merger with Choco Up Group Holdings is the company's key growth catalyst [S1][S2]. The transaction will reshape capital structure through issuance of new ordinary shares enabling potential balance sheet strengthening necessary for scaling brokerage credit capacity and expanding asset management product offerings.

The recent appointment of Onestop Assurance PAC as a unified audit firm supports streamlined financial oversight aligned with merger integration efforts [S3].

Potential synergies include cross-selling opportunities between client bases, expanded product suites leveraging combined technology platforms, and enhanced operational efficiencies across Hong Kong-Shenzhen corridors.

Successful completion hinges on timely Nasdaq clearance before the extended June deadline; any further delay could impact strategic momentum.

Risks and Watchpoints

Key risks include:

- Uncertainty regarding final regulatory approvals from Nasdaq necessary to close the merger transaction [S2].

- Persistent operating losses totaling approximately $5 million net loss in FY2025 despite revenues near $1.34 million USD [F1], exacerbated by legal/professional fees associated with merger activities.

- Fluctuating margin loan utilization affecting interest income stability; customer margin lending reduced significantly year-over-year [S11].

- Internal control weaknesses related to accounting expertise impacting U.S. GAAP financial reporting accuracy; remediation efforts are underway ahead of merger completion [S15].

- Related party transactions require careful governance oversight post-merger.

- Competitive pressures in brokerage commission pricing amid digitization trends.

- Cybersecurity risks remain an ongoing focus for board oversight though no material incidents have been reported thus far [S1].

Near-Term Milestones to Monitor

Investors should watch for:

- Final Nasdaq approval of the merger no later than June 30, 2026 per latest amendment [S2].

- Post-close quarterly financial reports showing synergy realization progress.

- Integration updates including IT systems unification or new product launches across subsidiaries.

- Progress on internal control remediation addressing prior material weaknesses documented at fiscal year-end December 31, 2025 [S15].

- Margin lending portfolio trends signaling stabilization or growth in interest income streams.

- Changes in executive leadership or ownership stakes influencing strategic direction given major shareholders hold controlling interests via Radiant Global Ventures Limited and Divine Star Ventures Limited [S1].

Latest Financial Snapshot (as of December 31, 2025)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1665000 | |

| 2025-12-31 | ||

| Current assets | $14mm | |

| 2025-12-31 | ||

| Current liabilities | $4mm | |

| 2025-12-31 | ||

| Current ratio | 3.45x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Revenue | $1.34 million |

| Net Income | -$5.06 million |

| Cash & Equivalents | $1.67 million |

| Current Ratio | 3.45 |

| [F1] |

Cash reserves remain sufficient to support ongoing operations despite losses ([F1],[S4]-[S6]). The current ratio above three times indicates healthy liquidity relative to current obligations ([F1]). However, continued operating deficits highlight the importance of successful merger completion to unlock growth scalability ([F1],[S1]). Regulatory capital requirements under Hong Kong Financial Resources Rules are currently met but require monitoring given margin financing fluctuations ([S5]).

Disclaimer

This analysis is based exclusively on publicly available SEC filings up to May 11, 2026. It does not constitute investment advice but provides an informed perspective on Plutus Financial Group Ltd’s recent developments and strategic outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments