Ampco-Pittsburgh Corp Balances Operational Restructuring and Asbestos Liabilities While Managing Capital Structure

The latest quarter highlights Ampco-Pittsburgh's ongoing operational reshaping, capital structure adjustments, and asbestos-related risk management amid industrial manufacturing headwinds.

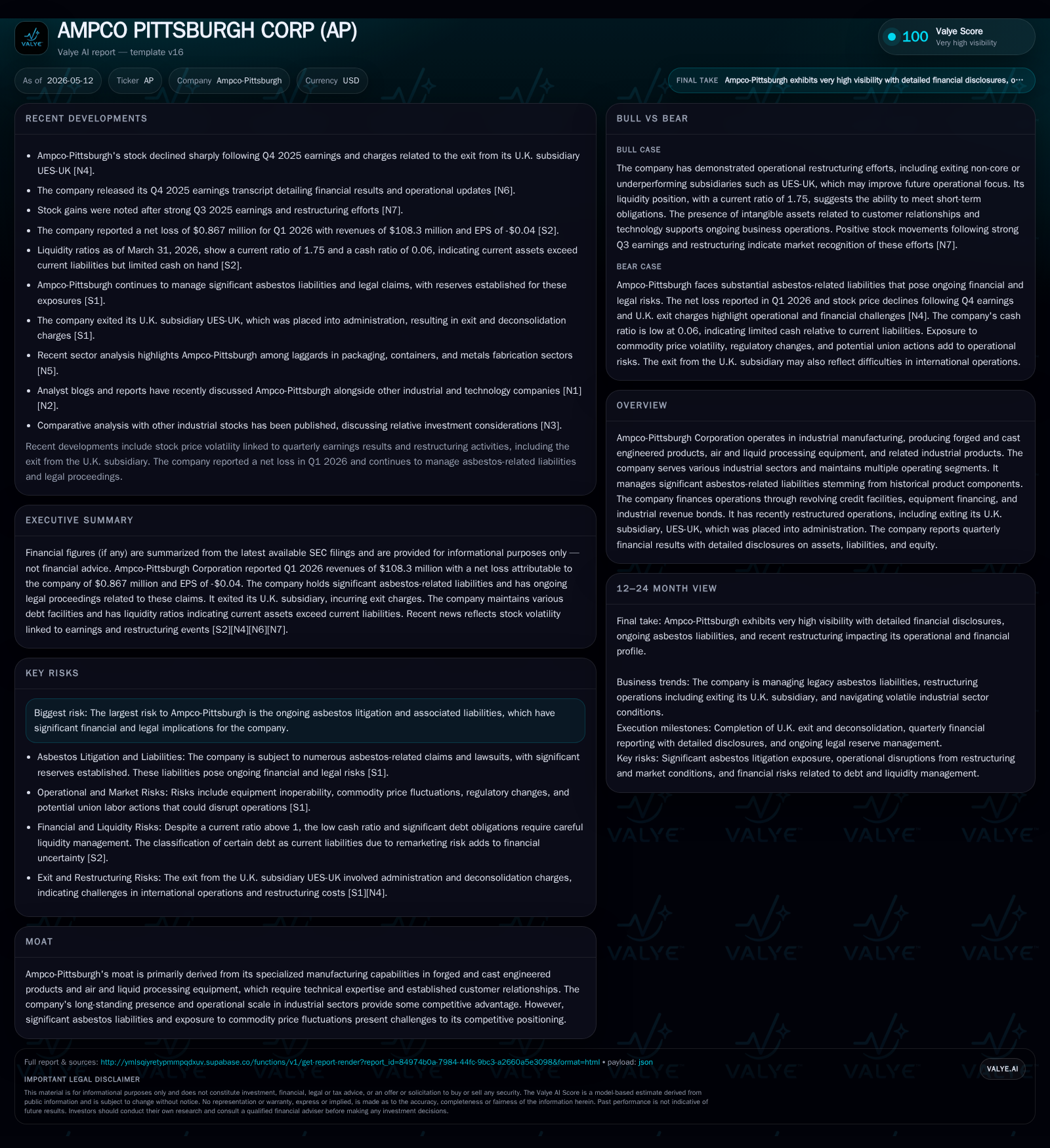

Ampco-Pittsburgh reported key updates in its Q1 2026 filing including compliance with covenants under its revolving credit facility and a rise in short-term swing loan balances. The company continues managing the fallout from the insolvency of its UK subsidiary UES-UK while dealing with asbestos litigation exposure. Ampco-Pittsburgh operates two main segments focused on forged/cast engineered products and air/liquid processing equipment, serving industrial sectors that face structural demand challenges. Its growth hinges on successful restructuring, cost controls, and navigating legacy liabilities. Significant debt remains on the balance sheet backed primarily by asset-based revolving credit and industrial revenue bonds. Monitoring operational execution and asbestos claim developments will be critical for future outlook.

Recent Operating Update: Q1 2026 Highlights

Ampco-Pittsburgh Corporation’s latest quarterly filing dated May 12, 2026 ([S2]) provides crucial insights into the company's near-term operating posture. The firm reported maintaining compliance with all applicable covenants tied to its amended revolving credit facility established June 25, 2025. This senior secured asset-based revolving credit facility amounts to $100 million with an extension option up to $125 million contingent on lender approvals. Interest rates under this facility are tied to SOFR plus a margin between 2.00%–2.50%.

Notably, the swing loan balance rose from $1.22 million at December 31, 2025 to $4.26 million as of March 31, 2026 ([S2]), reflecting temporary advances classified as current liabilities pending repayment or refinancing. This uptick points to working capital pressures or timing differences in customer payments and cash collection cycles.

Meanwhile, the company continues its exit from UK operations evidenced by Union Electric Steel UK Limited (UES-UK) already placed into administration since late 2025 ([S1], [S22]). This deconsolidation streamlines Ampco’s footprint but imposed restructuring charges impacting recent operating results.

Overall liquidity remained stable with cash & equivalents of $9.23 million as of March-end ([F1]). Current assets stood at approximately $249 million versus current liabilities of $142 million yielding a current ratio near 1.75 which suggests moderate short-term financial flexibility.[F1]

Business Model Overview

Ampco-Pittsburgh manufactures high-performance specialty metals and engineered equipment serving diverse industrial markets globally ([S2], [S1]). The company operates principally through two segments:

- Forged and Cast Engineered Products (FCEP): Focused on metal components such as forged mill rolls and cast products requiring technical forging expertise tailored for demanding industrial applications.

- Air and Liquid Processing (ALP): Offers custom-designed air handling systems, centrifugal pumps, heat exchange coils, and related equipment critical for fluid processing needs.

Revenue derives predominantly from sales contracts where customers pay for highly customized components or systems designed for their specific industrial process requirements. Pricing has exposure to raw material costs (notably aluminum and copper), industrial commodity cycles, and contract terms which together influence revenue mix and margins.

Margins depend heavily on operational scale efficiencies within forging/casting processes and engineering customization capabilities. Specialty nature grants some pricing power versus commoditized steel suppliers but is limited by cyclical industrial capital spending patterns.

Industry Structure & Competitive Position

Ampco sits within a fragmented industrial manufacturing landscape characterized by regional competition among specialized metal forging/casting providers alongside larger diversified steel product manufacturers outlet for air/liquid processing equipment.

Its moat is moderate—anchored by proprietary technical know-how in forging complex mill rolls combined with an installed customer base demanding engineered solutions (). However, market oversupply in global steel contributes cyclicality that constrains sustained pricing gains. Additionally, replacement capital investment cycles fluctuate notably by end-market economic conditions affecting order volumes.[N3]

Competitive pressures also arise from emerging low-cost manufacturers globally while regulatory complexity regarding environmental compliance adds operating challenges.[S1]

Growth Drivers

Key drivers supporting growth prospects include:

- Operational Restructuring: Post-exit from UK operations reduces legacy underperforming assets allowing focus on profitable core segments ([S1]).

- Technical Differentiation: Specialized engineering capabilities in forging tight tolerance mill rolls and customized air/liquid system design sustain customer loyalty.

- Capital Investment Cycles: Industrial customers’ replacement demand for mill rolls and process equipment correlates with broader manufacturing activity trends providing potential volume upsides.

- Pricing Management: Ability to manage raw material cost pass-throughs through contract terms or hedging influences product margin resilience.[S25]

- Backlog & Customer Deposits: Increasing customer prepayments suggest stabilized or improving order visibility which could translate into smoother revenue flow.[S28]

However, growth is fundamentally tethered to structural demand in cyclical industries like steel manufacturing where excess capacity can dampen capital spending.

Risks & Watchpoints

Ampco faces several notable risks that could impede growth or pressure profitability:

- Asbestos Litigation Exposure: Significant legacy asbestos claims related to historical product components remain a foremost financial risk requiring careful reserve management ([S1]).

- Leverage & Debt Service: Substantial outstanding debt (~$115 million) supported by asset-based lending necessitates disciplined cash flow management especially given potential covenant constraints ([F1], [S13]).

- Commodity Price Volatility: Fluctuations in steel inputs such as aluminum or copper potentially erode margins if not effectively hedged or passed through contractually ([S25]).

- Geopolitical & Economic Factors: Global trade disruptions or recessionary pressures could reduce end-user capital expenses impacting order volumes ([S14]).

- Operational Execution Risk: Maintaining cost discipline post-restructuring while integrating new technologies or capacity investments influences competitive positioning.

Close monitoring of asbestos claim trends—both frequency and severity—and the evolution of working capital financing needs through swing loans will provide early signals about financial health.

What To Watch Next

Critical upcoming indicators include:

- Quarterly updates on swing loan levels relative to operating cash flows reflecting liquidity stability.

- Progress in resolving asbestos-related liabilities either through settlements or court rulings affecting reserve adequacy.

- Order backlog movements within the FCEP/ALP segments signaling shifts in demand outlook.

- Raw material price hedging effectiveness mitigating input cost pressures amid inflationary environment.

- Cost optimization efficacy following UK operation wind-downs verifying restructuring benefits.

- Capital expenditure announcements supporting segment capacity upgrades or new product lines consistent with longer-term growth strategy.

Management guidance disclosures in future filings will help clarify expectations around these milestones explicitly if available.[N1][N2]

Financial Profile - Q1 End Snapshot [F1][S13]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $9mm | |

| 2026-03-31 | ||

| Total debt | $115mm | |

| 2026-03-31 | ||

| Net debt | $106mm | |

| 2026-03-31 | ||

| Current assets | $249mm | |

| 2026-03-31 | ||

| Current liabilities | $142mm | |

| 2026-03-31 | ||

| Current ratio | 1.75x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Net Debt approximated as Total Debt less Cash & Equivalents.

The company retains meaningful leverage largely via secured asset-backed facilities including revolving credit lines collateralized by receivables and inventory with maturities extending through mid-decade ([S2]). The Corporation was in compliance with the applicable covenants as of March 31, 2026 ([S2]).

Operating losses at the latest annual period reflect ongoing restructuring impacts coupled with legacy liability costs; however cash flow generation supports continued operational funding without immediate refinancing pressures ([F1]).

Disclaimer: This analysis is based exclusively on publicly filed regulatory disclosures up to May 12, 2026. It does not constitute investment advice or recommendations but aims to provide an informed industry perspective grounded in available corporate data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments