Adagio Medical Advances ULTA VT Ablation Amid Liquidity Challenges and Clinical Milestones

Adagio Medical progresses pivotal ULTA-based ventricular tachycardia treatment with a critical FDA trial complete and liquidity tightening.

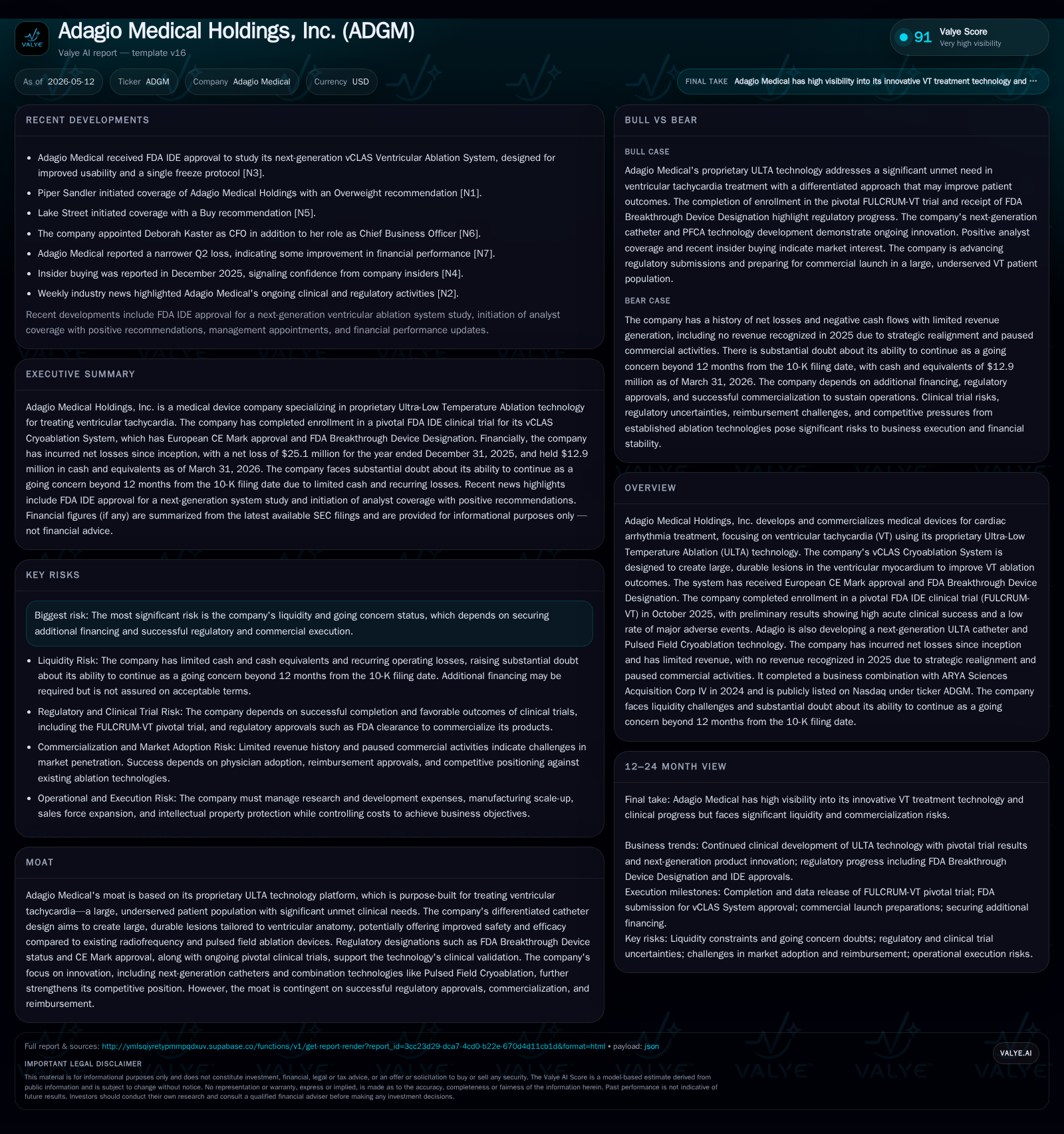

In its latest quarterly update, Adagio Medical Holdings reported no revenue for Q1 2026 reflecting a continued strategic pause in commercial activity while completing enrollment in its pivotal FULCRUM-VT trial. The company’s proprietary Ultra-Low Temperature Ablation (ULTA) technology targets the underserved ventricular tachycardia (VT) market with promising clinical data under FDA Breakthrough Device Designation. However, despite critical regulatory progress, Adagio faces substantial liquidity constraints with less than a year’s runway at current burn levels. Its growth hinges on forthcoming clinical trial results and securing additional funding to enable FDA approval and commercial launch in the U.S.

Recent Operating Update

Adagio Medical Holdings’ latest quarterly filing dated May 12, 2026 ([S2]) reveals continued operational execution focused on advancing its proprietary ULTA technology platform for ventricular tachycardia (VT) treatment. Notably, the company reported no revenue in Q1 2026—a continuation of the full-year 2025 status—attributable to a deliberate strategic pause in commercial activities including an inventory buyback undertaken during the prior year [S1]. This reflects management’s recalibration to synchronize commercialization efforts with anticipated regulatory approvals.

Crucially, Adagio completed enrollment of its pivotal FULCRUM-VT Investigational Device Exemption (IDE) trial in October 2025 ([S1]). Preliminary acute trial data demonstrate robust procedural success: a 97.4% non-inducibility rate of target ventricular arrhythmias post-ablation, alongside a low major adverse event incidence of 2.4%. The study enrolled a complex patient cohort across nineteen North American centers, encompassing both ischemic and non-ischemic cardiomyopathies, thus broadening applicability [S1]. Detailed six-month outcome data await publication at Heart Rhythm 2026, which will be instrumental for U.S. Food & Drug Administration (FDA) approval submissions.

Liquidity remains a pressing challenge; cash and equivalents stood at $12.9 million as of March 31, 2026, with total debt near $22.9 million resulting in net debt close to $10 million [F1]. This constrains operational runway as major regulatory milestones approach.

Business Model

Adagio Medical generates value by developing medical devices using its proprietary Ultra-Low Temperature Ablation (ULTA) technology aimed at treating VT—a life-threatening cardiac arrhythmia predominantly managed via catheter ablation techniques today. Revenue generation will flow from direct sales of its vCLAS Cryoablation System catheters and ancillary disposables used intra-procedurally by electrophysiologists.

The company’s core product addresses fundamental limitations inherent in radiofrequency (RF) ablation devices that were originally designed for atrial fibrillation rather than VT. By leveraging cryoablation at ultra-low temperatures optimized for ventricular myocardium's thicker anatomy, the system aims to create large, durable lesions that penetrate deeply while minimizing irrigation requirements [S1]. This differentiation potentially improves both safety profiles and long-term ablation success rates—a significant advance given VT’s complex pathophysiology.

Revenue mechanics hinge on procedure volumes—the number of VT ablations utilizing Adagio's tech—and device pricing negotiated mainly with hospitals and integrated delivery networks. Pricing power depends heavily on demonstrated clinical efficacy and cost-effectiveness relative to entrenched RF or pulsed field alternatives. Early European CE Mark approval enabled limited initial sales outside the U.S., but the bulk of future revenues depend on successful FDA clearance following FULCRUM-VT results.

Industry Structure and Competitive Position

The VT ablation market is characterized by complex patient needs with considerable unmet demand for safer and more efficacious therapies amid rising prevalence due to aging populations and increased cardiac disease burden. Current standard-of-care employs RF-based catheters designed primarily for atrial arrhythmias, leading to off-label or suboptimal use in VT with procedural complexity and variable outcomes.

Competitors include established device manufacturers focusing on RF and emerging entrants leveraging pulsed field ablation technology targeting broader electrophysiological indications but not yet specifically optimized for ventricular applications. Adagio's moat lies in its ULTA platform tailored explicitly for VT with breakthrough regulatory designations—namely FDA Breakthrough Device status granted in April 2025—and supportive clinical evidence [S1].

Nonetheless, incumbent firms possess entrenched hospital relationships and reimbursement channels, placing emphasis on Adagio’s need to prove superior safety/efficacy profiles through pivotal data and real-world adoption catalysts.

Growth Drivers

Key growth drivers stem from several interconnected vectors:

- Regulatory Progress: Positive six-month outcomes from the FULCRUM-VT IDE trial expected imminently will pave FDA submission pathways, foundational for commercial scale-up in the U.S.

- Market Need: VT affects an estimated hundreds of thousands annually in the U.S. alone with limited optimal therapies; demonstrating compelling clinical benefits could significantly expand procedure volumes.

- Technology Innovation: Beyond the vCLAS system, development of next-generation ULTA catheters incorporating Pulsed Field Cryoablation seeks to broaden indications including diverse arrhythmia types potentially enhancing future product pipeline value.

- Geographic Expansion: With CE Mark approval achieved, renewed European commercial efforts may resume following prior strategic pauses.

- Partnerships or Licensing: Potential collaborations within cardiac electrophysiology ecosystems could accelerate penetration leveraging established distribution or commercialization infrastructures.

Success is tied closely to measurable KPIs like trial enrollment efficiency (completed), procedural adoption metrics post-launch, backlog growth once commercial activity resumes, margin improvements via manufacturing scale-up, return visits/repeat ablations reduction evidencing durability gains, and eventual reimbursement acceptance in key markets.

Risks / Watchpoints / Growth Constraints

Fundamental risks magnify around:

- Liquidity Constraints: Current capital reserves limit operational runway into late 2026 absent further financing events; failure to secure timely capital jeopardizes trial completion analysis absorption costs and commercial launch readiness [F1].

- Regulatory Uncertainty: While early clinical success is favorable, longer-term outcomes remain unreported; any safety signals or efficacy shortfalls could delay or derail FDA approvals.

- Market Adoption Hurdles: Transitioning physicians from incumbent RF or growing PFA technologies requires convincing demonstration of clinical superiority coupled with competitive device pricing.

- Reimbursement Environment: Securing favorable hospital reimbursement codes remains critical given procedural cost sensitivity in electrophysiology suites.

- Operational Execution: Manufacturing scale-up complexities inherent to novel cryoablation devices pose potential delays or cost overruns.

- Competition: Larger medtech companies investing heavily in adjacent ablation spaces may accelerate innovation pace or leverage size advantages leading to squeezes on pricing power or share gains.

What To Watch Next

Several milestones will materially influence Adagio's trajectory:

- April 2026: Presentation/publication of six-month results from FULCRUM-VT pivotal study at Heart Rhythm conference ([S1]).

- FDA Submission: Timing contingent upon positive data release; formal premarket approval pathway initiation will be key stringency test.

- Commercialization Announcements: Plans regarding marketing rollout strategy relapse post regulatory green light.

- Financing Activity: Any public or private equity/debt raises announced will provide essential liquidity clarity amid burn-rate pressures reported [S16][F1].

- Pipeline Updates: Progress toward launching next-generation ULTA/Pulsed Field Cryoablation tools announced over coming quarters.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $13mm | |

| 2026-03-31 | ||

| Total debt | $23mm | |

| 2026-03-31 | ||

| Net debt | $10mm | |

| 2026-03-31 | ||

| Current assets | $16mm | |

| 2026-03-31 | ||

| Current liabilities | $9mm | |

| 2026-03-31 | ||

| Current ratio | 1.85x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026 [F1]: Net loss was reported as approximately $25 million for full-year ending December 31, 2025 [F1], consistent with continued pre-commercial development phase expenditure patterns emphasizing R&D investment over revenue generation given strategic repositioning decisions during calendar year 2025 [S1][S2].

Conclusion

Adagio Medical is positioned at an inflection point where promising proprietary cryoablation technology tailored for ventricular tachycardia could disrupt a large unmet clinical arena reliant on suboptimal legacy modalities. The company’s recent completion of pivotal clinical trial enrollment under an FDA Breakthrough Device Designation marks key technical validation progress paired with European CE Mark marketing clearance already received.

However, near-term operational viability is challenged by limited liquidity that necessitates prompt capital infusion alongside execution discipline poised to convert strong clinical hypotheses into regulatory approvals and effective commercialization frameworks—no small feat given medtech competitive dynamics around innovative cardiac arrhythmia therapies.

Investors monitoring Adagio should focus keenly on forthcoming clinical updates from the FULCRUM-VT trial six-month outcomes as well as management’s success in extending financial runway through capital markets or strategic partnerships that support launch scale-up capabilities towards what could be a meaningful advancement in VT patient care.

This analysis is based strictly on available SEC filings dated through May 12, 2026 ([S1]-[S3]) and corroborative financial snapshot data ([F1]), without forward-looking investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments