PUBLIC CO MANAGEMENT CORP Edges Toward Strategic Shift with Healthcare Assets Acquisition Plan

PCMC’s latest quarterly filing reveals pivotal progress toward acquiring a healthcare real estate portfolio, marking a strategic evolution from its shell company status.

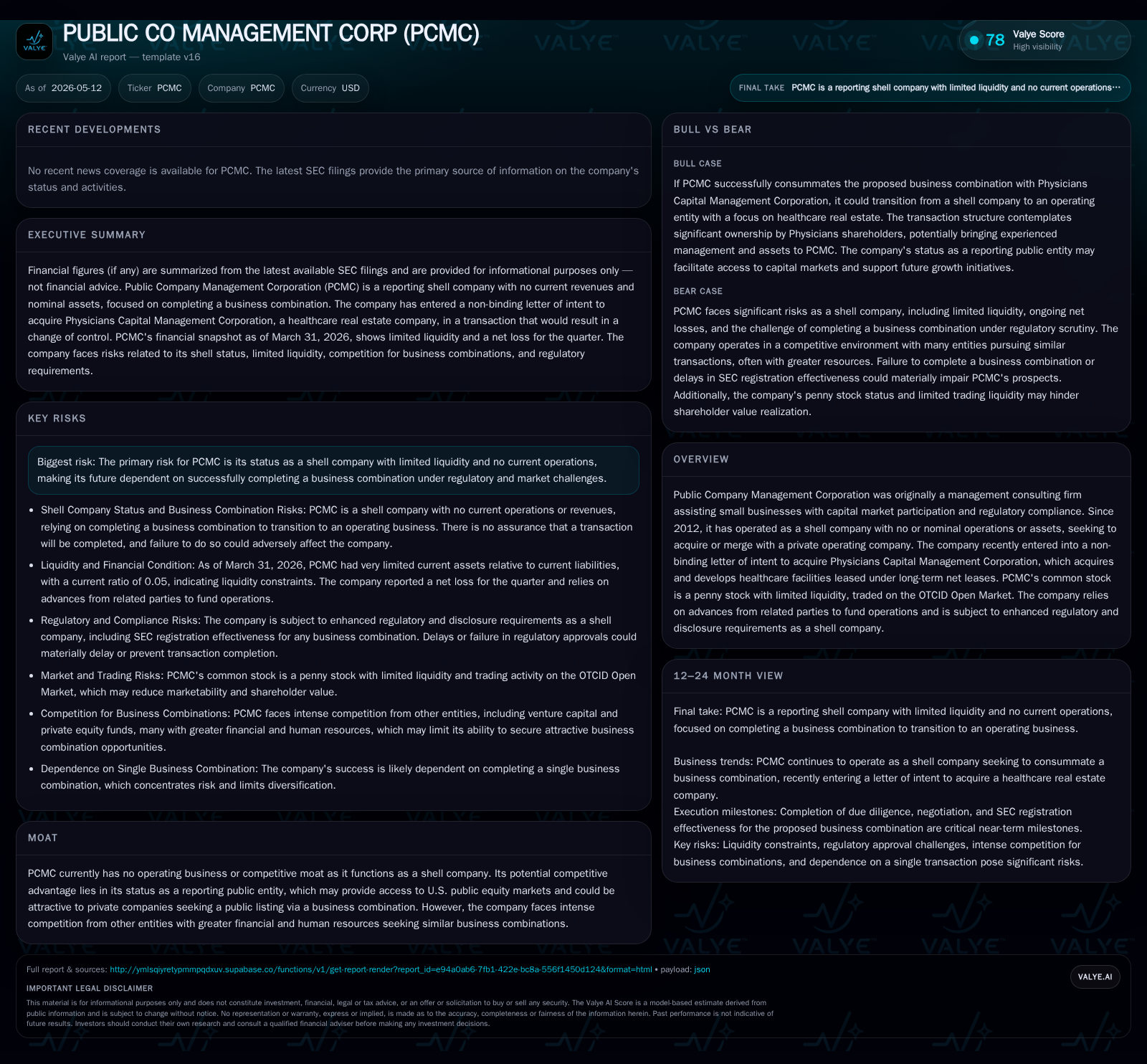

Public Company Management Corporation (PCMC), long functioning as a shell entity, disclosed significant developments in its May 2026 10-Q, highlighting ongoing negotiations to acquire Physicians Capital Management Corporation, a healthcare real estate operator focused on net-leased medical facilities. This transition signals PCMC’s attempt to forge an operational business model centered on healthcare asset management rather than consulting services or passive shell status. While the deal is still conditional and non-binding, amendments to PCMC’s capital structure granting blank-check preferred stock authority support flexibility for this acquisition. The company remains constrained by extremely limited liquidity and a dependence on related party advances, confronting typical risks of penny stocks and shell-company business combination vehicles. Key forthcoming milestones include definitive agreement execution and related governance changes that will test PCMC’s ability to complete the strategic pivot.

Latest Quarterly Update and Strategic Developments

The most recent quarterly filing dated May 12, 2026 (Form 10-Q) provides critical insight into PCMC’s evolving operational landscape [S2]. PCMC remains a reporting public shell company but is actively moving toward effecting a transformative business combination. The company entered into an exclusivity agreement pursuant to a non-binding Letter of Intent (LOI) dated February 23, 2026 with Physicians Capital Management Corporation (Physicians), which specializes in acquiring and developing healthcare facilities leased under long-term net leases [S12][S3]. The LOI establishes that upon closing Physicians shareholders would own roughly 80% of PCMC's equity post-transaction.

Notably, an amendment filed April 13, 2026 amended PCMC's Articles of Incorporation to authorize up to 50 million shares of preferred stock with "blank-check" powers granting the board flexibility to structure financing and equity issuances necessary for the acquisition [S3][S13][S18]. This amendment underscores preparatory corporate actions facilitating this potential strategic shift away from a dormant shell status. The exclusivity period within the LOI restricts Physicians from soliciting alternative offers during negotiation.

Board and management restructuring is anticipated concurrent with the closing. The LOI contemplates appointing Conrad Ivie, M.D., Physicians’ controlling shareholder, as PCMC Chairman and CEO effective at closing [S12]. These governance appointments signify an intention for operational continuity through seasoned leadership experienced in healthcare real estate asset management.

From Consulting Shell to Operating Entity: Business Model Transition

Historically, PCMC was incorporated in Nevada in 2000 initially providing niche consulting services targeting small businesses aiming at capital market participation [S1][S20]. The company's revenue derived primarily from flat-fee consulting engagements involving management advisory, regulatory compliance services, facilitation of public listings for private companies via direct offerings or self-underwriting. Payment methods included combinations of cash and restricted client common stock shares.

The financial crisis fallout starting in 2008 severely undermined the demand for such consultancy amidst reduced markets for fundraising and heightened competition from diverse financial intermediaries including investment banks and venture capitalists. Consequently, post-2012 the company adopted the classic "shell" company profile characterized by nominal assets and no active operations beyond seeking merger or acquisition targets [S1].

The contemplated acquisition of Physicians marks a material pivot from consultative services towards becoming an operating entity owning income-generating healthcare real estate assets. Physicians’ core business model involves acquiring medical facilities then leasing them under long-term triple-net leases where tenants assume property expenses such as maintenance and taxes. This shift implies more predictable recurring rental revenue streams different fundamentally from one-off consulting fees.

Evaluation of Possible Competitive Positioning in Healthcare Real Estate

Should the transaction consummate successfully, PCMC would join an established niche specializing in healthcare-related net-leased properties—an asset class often favored for relative stability due to enduring demand drivers like demographic aging and regulated tenant industries requiring specialized clinical space [S1]. However, competitive positioning remains challenged given many specialized publicly traded REITs and private equity players possess far greater financial scale and operational expertise.

PCMC’s principal strategic advantage post-acquisition could be leveraging its existing public reporting status—albeit as a small OTCID quoted security—to provide Physicians access to public equity capital markets historically difficult for purely private entities. This merging-and-listing vehicle role can appeal particularly if alternative IPO routes are financially or procedurally burdensome for specialized healthcare real estate operators.

Nonetheless, litigation risks frequent among shell-driven reverse mergers combined with limited historical operating track record create credibility hurdles. Given the penny stock context and low trading liquidity of PCMC common shares [S1], attracting institutional investor interest could be constrained absent demonstrable operational progress.

Sector Dynamics and Challenges in Utility of Business Combination Vehicles

Operational success hinges partly on navigating structural challenges inherent in public shell companies that pursue business combinations. Enhanced regulatory scrutiny demands comprehensive disclosure filings including Form S-4 merger proxy statements and pro forma audited financials from acquired entities—a costly multimonth process often delaying deal execution [S21][S27].

Additional complications arise from penny stock regulations entailing mandatory broker-dealer risk disclosures limiting secondary market activity [S1]. Regulatory compliance costs—while manageable given low scale financial activity—will escalate substantially post-combination as new operational filings commence.

Moreover, sector-wide supply constraints exist for quality healthcare net-lease assets amid rising valuations fueled by demographic aging trends benefiting medical facility landlords. Managing these properties also requires robust asset management capabilities tailored to clinical tenants with specific needs differing from traditional commercial retail or office properties.

Against this backdrop, PCMC lacks demonstrated capacity infrastructure but proposes acquisition synergy via Physicians’ existing portfolio plus management team led by Dr. Ivie.

Key Growth Catalysts and Value Drivers Post-Acquisition

Growth prospects depend heavily on successful negotiation completion culminating in definitive agreements followed by closing approvals including stockholder consents where required by Nevada law [S12][S24]. Confirmed appointments such as Dr. Ivie assuming Chairmanship and CEO roles act as positive governance signals enhancing managerial expertise.

Post-closing operational KPIs will center around lease occupancy rates within acquired properties maintaining stable cash flow under long-term leases typical within net lease models. Inherent defensive characteristics against economic cyclicality come from regulated tenant creditworthiness (hospitals or ambulatory surgical centers).

Additionally, structural shifts supported by broader demographics favor demand growth for medical facilities providing expansion opportunities through portfolio scaling or selective acquisitions. The ability to access public market equity through PCMC’s reporting platform could improve capital raising efficiency fostering organic growth.

Risks and Constraints Underpinning PCMC’s Transformation Roadmap

Principal risk elements revolve around continued extreme liquidity stress documented by a March quarter-end current ratio near 0.05 due to current assets totaling just $15K against liabilities exceeding $313K [F1]. Dependency on unsecured advances from related parties to meet operating costs without revenue inflows highlights constrained financial runway absent immediate transaction close [S28].[F1]

Execution risk encompasses failure to reach binding definitive agreements within exclusivity periods or encounter regulatory delays impacting transaction timing adversely. Post-closing issuance of restricted securities implicates holding periods under Rule 144 constraining share liquidity even after relisting emerges clarifying valuation uncertainties.[S4]

Furthermore, SEC reporting complexities combined with high volatility penny stock status compound uncertainty over eventual investor reception. Competing shells pursuing similar niches dilute prospective investor attention while any instability in newly assumed asset portfolios could impair cash flow reliability.

Upcoming Targets and Catalysts for Stakeholders’ Attention

Investors should monitor imminent milestones such as:

- Definitive acquisition agreement execution following completion of due diligence;

- Finalization of board composition including formal appointment confirmations for Dr. Ivie as Chairman/CEO;

- Shareholder consent solicitations aligned with Nevada Revised Statutes mandates;

- Public filings evidencing cessation of shell status including comprehensive Form 8-K disclosures detailing combined entity operational overview;

- Closing conditions satisfaction including possible third-party lender or regulatory clearances;

- Early-period financial reporting demonstrating rental income realization sustaining corporate viability. These events will critically inform whether PCMC can effectively transition into an operating entity within healthcare real estate leasing [S3][S4][S6].

Summary Financial Position Snapshot

Latest financial snapshot

Liquidity constraints starkly illustrate operational vulnerability with liabilities dwarfing liquid assets heavily reliant on related party funding arrangements absent organic cash generation [F1][S28]. This balance sheet profile typifies early-stage public shells awaiting transformative transactions.

This analysis synthesizes facts drawn explicitly from recent SEC filings up to May 12, 2026 and corroborating data sets without speculative extrapolation respecting the company-specific evidentiary base available at this time. No investment advice is expressed or implied herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments