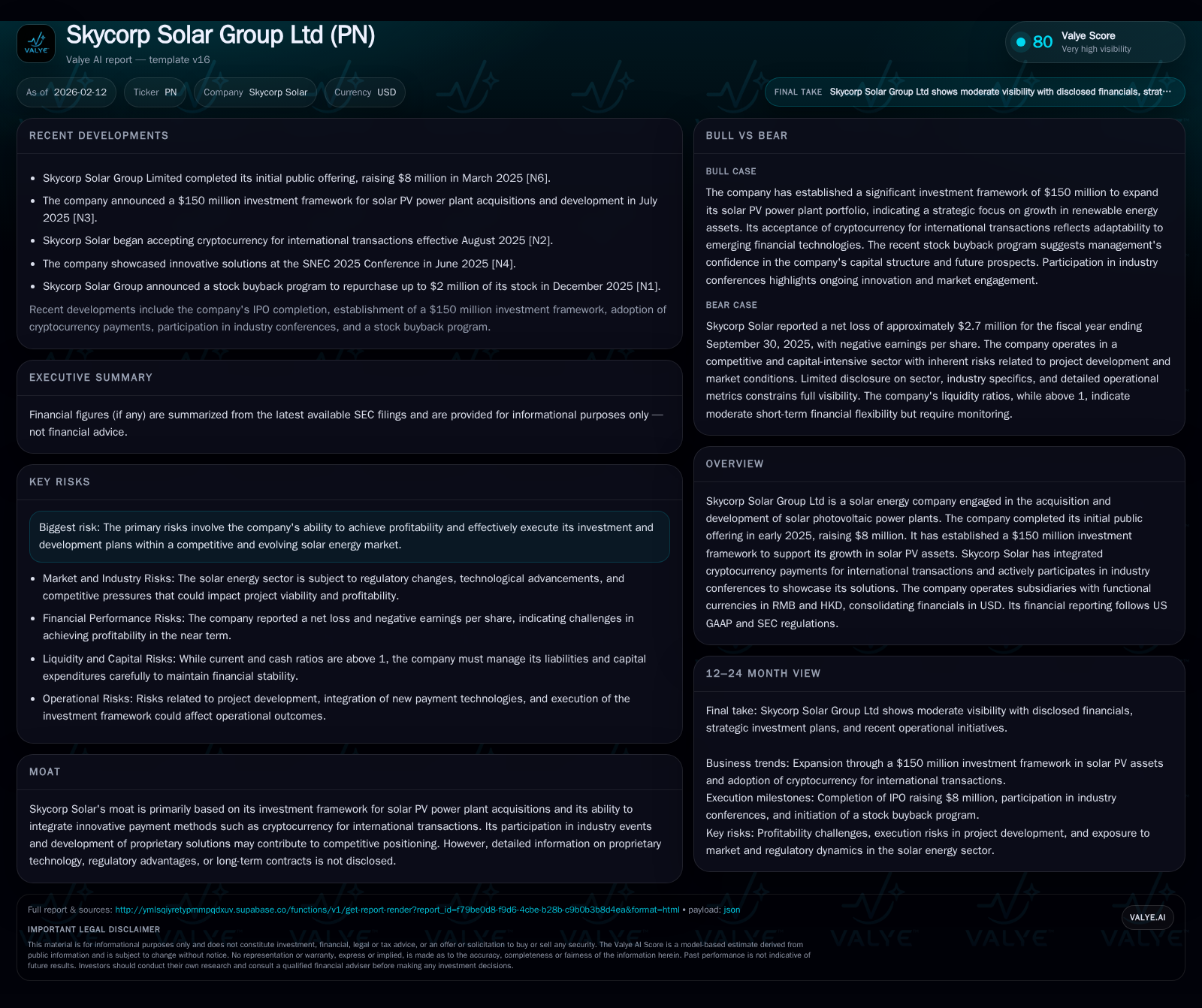

Skycorp Solar's Strategic Shift in Solar PV and HPC Amid Nasdaq Compliance Challenges

Exploring Skycorp Solar’s evolving business model, manufacturing growth, and regulatory hurdles as it navigates financial headwinds.

Skycorp Solar Group Ltd primarily operates as a manufacturer of solar photovoltaic products, generating over 97% of its revenue from this segment while cautiously expanding into high-performance computing server solutions. Despite top-line revenue growth to $63.3 million in fiscal 2025, the company reported a net loss, reflecting challenges in scaling profitably amidst market competition and investment demands. Manufacturing capacity expansion is underway with a new plant planned for 2027 in Nanjing, positioning Skycorp to diversify and improve margins. However, recent Nasdaq notification concerning minimum bid price non-compliance introduces near-term risks that the company must address. Skycorp’s use of cryptocurrency payments and IP portfolio highlight innovation efforts, though regulatory complexities around foreign investment and insurance gaps present further operational challenges.

From Solar Cables to Green Computing: Skycorp’s Dual-Industry Approach

Skycorp Solar Group Ltd anchors its business chiefly on manufacturing solar photovoltaic (PV) products—solar cables and connectors—with this segment contributing approximately 97.4% of fiscal year 2025 revenues. Simultaneously, the company has pursued a nascent yet strategic entry into high-performance computing (HPC) servers, accounting for about 2% of revenue that year, down from nearly 7% previously [S1]. This pivot reflects a broader vision: leveraging renewable energy solutions to power energy-intensive data centers sustainably.

The dual-industry approach fuses traditional solar hardware manufacturing expertise with emerging tech sectors where HPC servers align with green energy imperatives. Such integration aims to satisfy a growing market demand for environmentally responsible computing infrastructure—a trend rising amid escalating energy costs and corporate sustainability commitments. Yet, HPC sales remain modest relative to core solar activities, indicating this is an area likely targeted for gradual expansion rather than immediate scale.

This blend positions Skycorp uniquely but also generates operational complexity where the company must maintain competencies across diverse technologies and customer bases. The approach underscores management's intent to evolve beyond commodity PV product offerings toward integrated clean-energy IT solutions.

Financial Snapshot: Growth and Profitability Challenges

Fiscal year 2025 saw Skycorp achieving revenue growth to $63.3 million from $49.9 million the prior year—a significant increase driven by expanded sales volumes primarily within solar PV products [F1][S1]. However, this top-line advance was accompanied by an operational loss nearing $2.7 million compared with a modest profit a year earlier.

The widening loss suggests mounting pressure from increased operating expenses—possibly related to R&D investments, marketing efforts to support HPC product expansion, or costs linked to production scale-up preparations. Notably, the current ratio stood at about 1.59 (current assets roughly $34.6 million against current liabilities around $21.7 million), indicating Skycorp retains an adequate liquidity buffer for short-term obligations despite ongoing unprofitability [F1].

This financial snapshot portrays a company navigating between growth ambitions and the practical hurdles of converting rising revenues into sustainable profits. The burden remains on operational efficiencies and margin enhancements especially as new manufacturing projects commence.

Manufacturing Footprint and Capacity Expansion Plans

Skycorp’s present manufacturing stronghold is its facility located in Ningbo, Zhejiang Province, operational since June 2015 with an annual production capacity of approximately 180 million meters of solar cable equivalent product [S1]. This sizable capacity underpins their ability to meet current demand domestically and internationally.

Looking forward, plans are underway for establishing another facility in Nanjing’s Pukou District expected to begin operations in 2027 [S1]. The new site aims to broaden product offerings beyond cables toward more diversified PV solutions while permitting cost structure improvements through economies of scale and process automation strategies.

Such capacity expansion is pivotal not only for volume-driven cost reduction but also for bolstering margin resilience amid intense sector competition. The focus on automation signals management's push toward leaner operations ensuring timely delivery aligned closely with incoming orders.

Global Market Reach and Currency Dynamics

Internationally, Skycorp targets markets across Asia—including China as its home base—and Europe [S1]. This geographic spread aligns with regions exhibiting robust demand growth in green energy adoption alongside technology upgrades for data center infrastructure.

However, managing cross-border operations introduces complexities tied to currency translation effects; subsidiaries operate under functional currencies of the Chinese Renminbi (RMB) or Hong Kong Dollar (HKD), which are translated into US dollars for consolidated reporting [S1]. Fluctuations in exchange rates can materially influence reported earnings and asset values independently of operational performance.

Furthermore, international expansion exposes the company to incremental legal obligations—including tariffs and foreign taxation—as well as potential operational cost increases attributable to integration challenges across diverse regulatory environments.

Innovation Edge: Patents, Technology Integration, and Cryptocurrency Usage

Technology innovation sits at the core of Skycorp’s competitive posture. The company holds a portfolio of 58 patents encompassing multiple key technologies essential to its solar PV manufacturing processes [S1]. This intellectual property reservoir undergirds its product differentiation efforts amid commoditized markets.

Strategic partnerships with integrated circuit (IC) chip manufacturers enhance product capabilities particularly as they venture deeper into serving HPC server clients with both new and used units [S1]. Such collaborations harvest technical synergies crucial for meeting increasingly stringent performance standards demanded by enterprise customers.

A notable innovation adoption is Skycorp’s acceptance of cryptocurrency payments for international transactions—suggesting an openness towards fintech solutions aimed at streamlining cross-border trade settlements [valye_report_excerpt][S1]. This novel payment method can offer efficiency gains though also entails exposure to crypto asset volatility risks.

Active participation in industry conferences signifies intent not just to showcase offerings but also gather market intelligence necessary for iterative technology evolution.

Yet despite these advancements, disclosures lack evidence of proprietary technology leading directly to significant regulatory advantages or firm long-term supply contracts that typically strengthen barriers against competitors.

Navigating Regulatory Terrain and Foreign Investment Landscape

Operating primarily within China situates Skycorp within a complex regulatory framework shaped by evolving foreign investment laws enacted recently—the PRC Company Law amendments (2023), Foreign Investment Law (2019) with subsequent Implementing Rules—and associated policy instruments such as the Negative List updated in late 2024 [S1].

These regulations dictate that foreign investors receive pre-entry national treatment barring prohibitions/restrictions detailed in negative lists which define prohibited/restricted industries from foreign participation [S1]. Notably Skycorp’s current business lines are not on the restricted or prohibited lists which lends operational freedom; however, amendments may change this status unpredictably.

The complexity extends because subsidiaries incorporated domestically must comply simultaneously with various layers of law impacting ownership structure, managerial appointments, reporting requirements, etc., while seeking favorable interpretations that preserve capital inflows under foreign ownership.

Consequently regulatory risk remains moderate but nontrivial especially when geopolitical tensions potentially induce abrupt policy shifts affecting foreign invested enterprises' operation continuity or cost basis.

Nasdaq Compliance Spotlight: Implications and Response Strategies

In late October 2025 Skycorp received formal notice from Nasdaq pointing out failure to meet the required minimum bid price ($1 per share) over a prescribed consecutive trading period triggering initial non-compliance status under Nasdaq Listing Rule 5550(a)(2) [S2].

This notice initiates a compliance cure period extending through April 28, 2026 during which Skycorp must restore its share price above threshold for at least ten consecutive trading days to retain listing without further measures [S2]. Failure would permit eligibility for an additional six-month extension contingent on satisfying other Nasdaq requirements—potentially involving reverse stock split actions designed to elevate per-share pricing notably criticized by shareholders due dilution/market reception concerns.

While receiving such notices is not uncommon among small-cap growth companies facing volatile market sentiment or subdued trading liquidity conditions—it nevertheless poses reputational risk that may dampen investor confidence or restrict access to capital markets needed for financing expansion plans.

Skycorp management thus faces pressing tasks balancing strategic communicative transparency with tactical share price support initiatives amid this compliance challenge.

Risks on the Horizon: Execution, Competition, and Insurance Gaps

Execution risk remains front-and-center given demands imposed by ramping up production capacity while simultaneously diversifying offerings into HPC-related segments not traditionally within core competencies [valye_report_excerpt][S1]. Failure in scaling efficiency or supply chain disruptions could stress margins further.

Competitive environment intensifies as global players expand aggressively both within established renewable energy domains and emerging high-performance computing infrastructure sectors complicating clear differentiation paths.

Intellectual property protection though backed by patents is potentially insufficient absent legally binding licensing agreements or exclusive contracts limiting competitor replication risks [valye_report_excerpt]. This vulnerability necessitates continuous innovation cycles plus safeguarding mechanisms against infringements.

Of notable concern is lack of business disruption insurance exposing Skycorp financially if unforeseen events such as natural disasters or supply interruptions impair operations resulting in lost revenues potentially exacerbating already thin profit buffers [valye_report_excerpt].

Outlook: Can Skycorp Translate Scale into Sustainable Profits?

The company’s trajectory offers cautious optimism tempered by current losses juxtaposed against evident top-line growth fueled by robust solar PV demand globally [valye_report_excerpt][S1]. Planned Nanjing plant commissioning could mark inflection points enhancing gross margins through scale economies alongside incremental automation benefits reducing production costs.

Innovation-led initiatives—cryptocurrency-enabled international transactions along with technical alliances targeting HPC ecosystem penetration—reflect strategic attempts at diversification foundational for future resilience.

Nevertheless balancing rapid growth investments against profitability pressures will test management acumen particularly within tightening capital markets characterized by increased scrutiny following Nasdaq listing concerns.[S2]

Regulatory vigilance remains critical given China’s fluid foreign investment policies requiring adaptive compliance frameworks ensuring uninterrupted operation whilst optimizing capital structure for sustained development.

In summary, while no imminent adverse forecasts presently loom explicitly according to disclosed information,[S1] materialization of strategic objectives demands disciplined execution amidst navigating evolving external economic, regulatory, and market landscapes.

This analysis synthesizes information available as of early 2026 from public filings without offering investment guidance. Readers should consider broader market context alongside specific company disclosures when forming perspectives about Skycorp Solar Group Ltd's prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments