Pentair’s Balancing Act: Growth Ambitions Constrained by Customer Concentration and Economic Cyclicality

Pentair plc’s steady revenue gains and efficient capital deployment contrast with concentrated customer exposure and cyclical risks in water treatment and flow solutions.

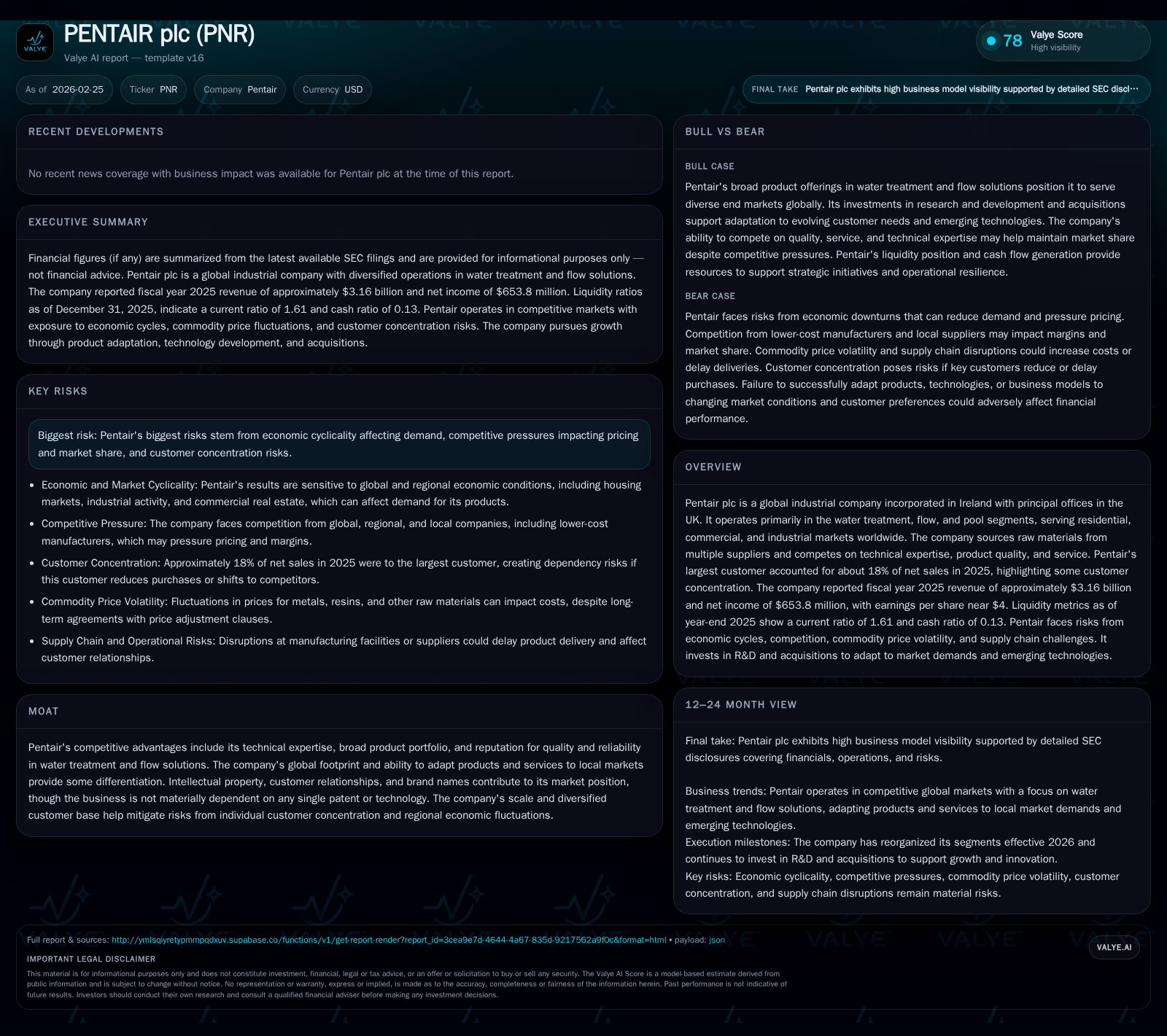

Pentair plc, a global industrial company focused on water treatment, flow, and pool solutions, has demonstrated modest revenue growth and consistent profitability over recent years. Its technical expertise and diverse product offerings underpin a competitive moat, yet the concentration of nearly 18% of sales from one customer highlights a notable risk. The company invests significantly in R&D and strategic acquisitions to capture emerging market opportunities but remains exposed to economic cycles influencing demand. Pentair’s strong operating cash flows have supported dividends and increased buybacks, reflecting disciplined capital allocation despite uncertainties around supply chain dynamics and commodity costs.

Company Overview and Market Position

Pentair plc is an Ireland-incorporated global industrial player headquartered in the UK that primarily provides water treatment, flow control, and pool-related products and services across residential, commercial, and industrial sectors worldwide. Its broad product portfolio coupled with technical expertise grants it differentiation in markets characterized by stringent quality expectations and regulatory oversight. Intellectual property assets, established brand names, and longstanding customer relationships contribute to Pentair's defensible market position.

The company's global footprint enables adaptation of products for local markets but also exposes it to complex supply chains and currency fluctuations that management actively hedges through financial instruments [S4][S6]. Notably, Pentair derives approximately 18% of its net sales from its largest customer group as of 2025—a significant source of revenue concentration that introduces downside risk if purchasing patterns change unfavorably [S18].

Historical Financial Performance

Between fiscal years 2019 and 2025, Pentair has exhibited steady topline expansion alongside margin improvement:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 654 | 815 | 858 | 69 | +4.5% |

| 2024 | 625 | 767 | 804 | 74 | +0.4% |

| 2023 | 623 | 619 | 739 | 76 | +29.5% |

| 2022 | 481 | 363 | 595 | 85 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 164 | 225 | 746 |

| 2024 | 152 | 150 | 692 |

| 2023 | 145 | 0 | 543 |

| 2022 | 139 | 50 | 278 |

Source: SEC companyfacts cache [F1].

Note: Revenue values prior to FY2025 are not available; capex includes payments for property plant equipment; dividends and buybacks are based on cash outflows reported.

Despite relatively modest top-line growth (~2%), Pentair enhanced operating income by nearly double-digit percentages between FY2023-25 driven by operational efficiencies and cost restructurings [F1][S10]. Net income improvements were more muted but remained positive over the period.

Operating cash flow surges outpaced net income gains reflecting effective working capital management amid an environment where raw material prices have shown periodic volatility.[F1]

Growth Drivers and Future Prospects

Pentair’s forward-looking strategy hinges on several pillars:

- Innovation through R&D: Continued investments aim at expanding advanced water filtration solutions addressing sustainability concerns aligned with climate awareness trends globally [S21].

- Selective Acquisitions: The company targets bolt-on acquisitions that can either broaden its technology base or accelerate market penetration especially outside North America [S10].

- Transformation Programs: Ongoing efforts focus on simplifying processes and reducing structural costs while aligning product offering to evolving end-market needs with an emphasis on digitalization.

- Expansion into Emerging Markets: Penetration into developing economies offers room for growth beyond relatively mature Western Europe markets where competitive intensity is high.

However, growth is tempered by economic cyclicality affecting capital investment trends across industrial customers as well as potential pressure on selling prices due to competition with regional suppliers who may maintain lower cost structures or stronger local ties [S23]. Customer concentration also poses downside risk if reliance on major buyers materializes into demand fluctuations.

Forecasts and Key Milestones

The company has not issued explicit public guidance for subsequent years; observations from recent quarterly filings suggest management will prioritize free cash flow maximization alongside margin expansion efforts through operational excellence initiatives.[N# missing S#]

Key indicators to monitor include:

- Sales volume trends within core segments (water solutions, flow technologies)

- Margin trajectory following restructuring charge absorption

- Integration success from new acquisitions that could contribute synergistic benefits

- Impact of material cost environment on gross margins given ongoing commodity price volatility

Capital Structure and Liquidity

As of late FY2025, Pentair maintains a solid liquidity position characterized by a current ratio of approximately 1.61 with cash reserves around $128 million [F1][S20]. The company’s total debt stands near $1.58 billion structured across senior notes due through early-2030s maturities plus revolving credit facilities with staggered repayment profiles mitigating refinancing risk [S4][S13].

Interest rates on borrowings vary from roughly mid-5% range for term loans to senior notes with fixed coupons from roughly mid-4% to near-6%, positioning debt costs moderately in line with market standards for investment-grade industrials.[S13]

Financial covenants restrict leverage ratios below target thresholds (typically <3.75x EBITDA) preserving balance sheet flexibility [S6][S14]. Hedging programs partially shield foreign exchange risks associated with global revenues.

Returns & Capital Allocation Priorities

Based on available data, approximate return on equity calculates near mid-teens (~14%), reflecting consistent profitability relative to equity base [F1].

Free cash flow generation remains robust given operating cash flows exceeding capital expenditures by over $700 million annually recently.

Dividend distributions have grown steadily year-over-year (about $164 million paid in FY2025), echoing commitment to returning value while retaining cash for reinvesting in the business through R&D and acquisitions.

Share repurchasing activity intensified notably with $225 million spent in FY2025 up from zero buybacks in FY2023 highlighting confidence in internal capital deployment options responding to share price levels.[F1][S22]

Industry Context & Domain Nuances (Analysis)

Pentair operates within highly technical segments where equipment lifespan, reliability under variable environmental conditions, and regulatory certifications govern purchasing decisions heavily. The water treatment industry is increasingly shaped by heightened environmental regulation prompting innovation towards energy-efficient systems integrated with remote monitoring capabilities. Moreover, end-users' shift toward sustainability creates growing demand for technologies reducing chemical usage or improving water reuse capabilities—a trend Pentair actively targets. In addition to organic growth drivers, competitive pressure arises not only from multinational incumbents but also from nimble local manufacturers adapting offerings regionally. Supply chain dynamics including raw material availability like specialty metals or plastics used in pumps and filtration membranes remain critical operational considerations potentially driving input cost inflation pressures.

Risks Summary

Key risks articulated include:

- Economic downturns influencing customer order timing or quantity leading to revenue volatility;

- Price competition eroding margins especially if regional competitors gain share or consolidation occurs;

- Customer concentration risk tied predominantly to one significant buyer representing ~18%;

- Supply chain interruptions possibly causing delivery delays impacting sales timelines;

- Failure to successfully integrate acquired businesses or technological innovations possibly limiting competitive positioning.

Conclusion

Pentair stands as a technically proficient player in water treatment related industries exhibiting stable historical performance marked by incremental top-line growth paired with notable margin gains over recent years.[F1] Its investment discipline evidenced by expanding dividends combined with accelerated share buybacks points to active management engagement in shareholder returns.[F1] However, challenges persist around customer concentration risks compounded by macroeconomic cyclicality affecting demand across its commercial-industrial client base.[S18][S23] The firm’s forward momentum depends heavily on sustaining innovation-led product enhancements alongside adept acquisition integration fueled by ongoing transformation initiatives.[S10][S21] Monitoring developments in key end markets—particularly shifts in regulatory environment or fresh competitive entrants—will be vital cues for future performance trajectory.

This analysis incorporates data available up to February 25th, 2026 from SEC filings and company disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments