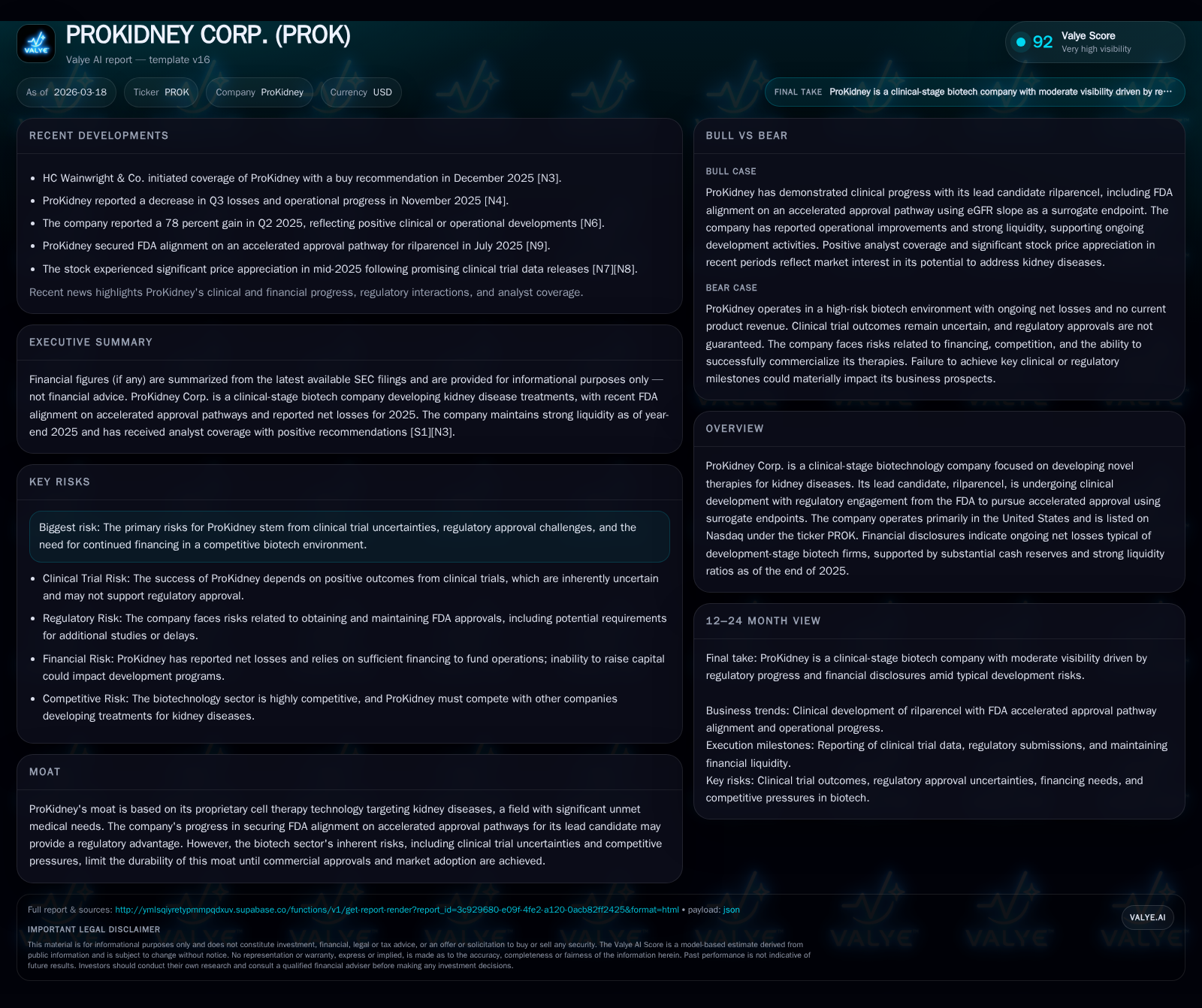

ProKidney’s Clinical Advances and Financial Position Shape Its 2026 Outlook

Clinical progress with rilparencel and robust liquidity underpin ProKidney's near-term development trajectory within kidney disease biotech.

ProKidney Corp., a clinical-stage biotech focused on kidney disease, has advanced its lead therapy rilparencel under an FDA accelerated approval pathway relying on surrogate endpoints like eGFR slope. Financially, the company shows a typical clinical-stage loss profile but maintains strong cash reserves supporting operational plans into mid-2027. Upcoming PROACT-1 trial readouts and regulatory feedback constitute critical milestones. However, risks related to clinical execution, regulatory outcomes, and financing persist amid competitive pressures.

Historical Financial Performance and Operating Trends

ProKidney exhibits the financial profile typical of a clinical-stage biotechnology company focused on cell therapies for kidney diseases. Operating income remained substantially negative but improved modestly from -$183.7 million in FY2024 to -$165.0 million in FY2025, representing a 10.2% year-over-year improvement driven by disciplined cost management alongside persistent research efforts [F1]. Net losses widened to -$68.9 million in FY2025 from -$61.2 million in FY2024 amid increased trial activity costs.

Operating cash flow remained negative at -$120.1 million in FY2025, while capital expenditures fell sharply by nearly 50% year-over-year to approximately $15.2 million, indicative of a shift from upfront infrastructure investments toward sustaining ongoing clinical operations [F1]. The company's current ratio stands at about 9.13x (current assets $280.7 million vs current liabilities $30.7 million), signaling strong liquidity to fund near-term operations [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -69 | -120 | -165 | 15 | -12.7% |

| 2024 | -61 | -126 | -184 | 30 | -72.5% |

| 2023 | -35 | -90 | -152 | 34 | +34.9% |

| 2022 | -55 | -77 | -153 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -135 | 6.8 |

| 2024 | 0 | -156 | 6.1 |

| 2023 | 9 | -124 | 3.2 |

| 2022 | -79 | 5.0 |

Source: SEC companyfacts cache [F1].

Table: ProKidney Historical Financials (FY2022–FY2025), rounded USD values

This pattern reflects typical capital consumption ahead of commercial product launches in the biotech sector.

Clinical Program Advances and Regulatory Engagement

ProKidney’s lead candidate rilparencel is an allogeneic cell therapy targeting chronic kidney disease progression through immunomodulatory mechanisms. The company leverages surrogate endpoints such as estimated glomerular filtration rate (eGFR) slope for accelerated FDA approval pathways—a regulatory approach gaining traction in nephrology therapeutics [S8],[S10].

The pivotal Phase 3 PROACT-1 trial targets approximately 470 patients with kidney impairment risk factors; the enrollment target was recently updated without altering statistical powering assumptions [S19]. Topline results for the surrogate endpoint are anticipated in Q2 2027 with confirmatory composite time-to-event data expected by H2 2029.

This dual-endpoint design balances expedited access with rigorous long-term efficacy confirmation amid scientific and regulatory complexities associated with novel cellular modalities.

Growth Prospects Rooted in Kidney Disease Therapeutics

Chronic kidney disease represents a significant unmet medical need worldwide with limited options that effectively modify disease progression. ProKidney’s differentiated cell therapy platform aims to address this gap through innovative immunomodulation.

Manufacturing scale-up challenges remain critical given the complexity of maintaining cell viability and potency; successful navigation here is key to competitive positioning alongside validation of biomarkers like eGFR slope.

Although competitive pressures exist from other biologics and small molecules targeting overlapping indications, ProKidney’s regulatory strategy and proprietary technology could afford meaningful early-mover advantages if clinical milestones are achieved.

Manufacturing and Trial Considerations

Cell therapy entails complex manufacturing logistics including donor cell characterization and allogeneic compatibility management—factors that influence timelines and costs [S5],[S6]. Surrogate endpoint validation is evolving; eGFR slope is increasingly accepted as a meaningful marker of renal function decline over shorter intervals.

Trial enrollment variability poses risks common to rare disease studies that may affect adherence and statistical power.

Capital Structure and Liquidity Position

At December 31, 2025, ProKidney held approximately $108.5 million in cash and equivalents with a strong current ratio (~9.13), supporting funding into mid-2027 per management disclosures [F1],[S13]. No share repurchases occurred since FY2024 when $9.5 million were repurchased; given sustained net losses and a negative equity position near minus $1 billion reflecting accumulated deficits, capital allocation prioritizes pipeline advancement over shareholder returns [F1].

Operating cash flow combined with capex indicates annual free cash flow deficits exceeding $135 million consistent with investment cycles typical for late-stage clinical biotechs.

Traditional profitability metrics such as return on equity are not meaningful given negative equity; value assessment centers on milestone-driven inflections rather than earnings returns.

Potential dilution risk exists if further financing becomes necessary before commercialization; however current liquidity affords meaningful runway assuming controlled burn rates.

Key Risks Impacting Value Creation

Risks include possible setbacks in PROACT-1 outcomes where surrogate endpoint thresholds may not be met or expanded data requests delay approvals [S5],[S6]. Regulatory acceptance of eGFR slope remains subject to interpretation despite precedent.

Manufacturing scale complexities also contribute uncertainty regarding batch consistency.

Financial risks involve potential future capital raises amid volatile markets as seen across peer biotechs reporting recent losses [N1],[N2]. Additional non-clinical risks relate to stock listing status post-domestication potentially affecting liquidity.

Analyst's View: Milestones to Monitor

Critical upcoming milestones include PROACT-1 interim data expected Q2 2027 assessing eGFR slope changes—a positive outcome could materially reduce execution risk enabling BLA submission under accelerated approval provisions [S8].

Subsequent regulatory feedback on the sufficiency of surrogate data will be pivotal amid evolving nephrology approval standards.

Cash burn trends versus reserves warrant close monitoring approaching mid-2027; deviations may prompt capital raises impacting valuation.

Subsequent operational markers such as manufacturing consistency updates will be relevant for commercial feasibility assessments.

While consensus forecasts are unavailable given developmental status, these milestones define potential inflection points shaping longer-term growth prospects within this challenging therapeutic domain.

This analysis draws exclusively on official SEC filings ([F1], [S#]) and verified news sources ([N#]) without unsubstantiated speculation or unsupported metrics. Forward-looking statements are clearly noted as per company disclosures without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments