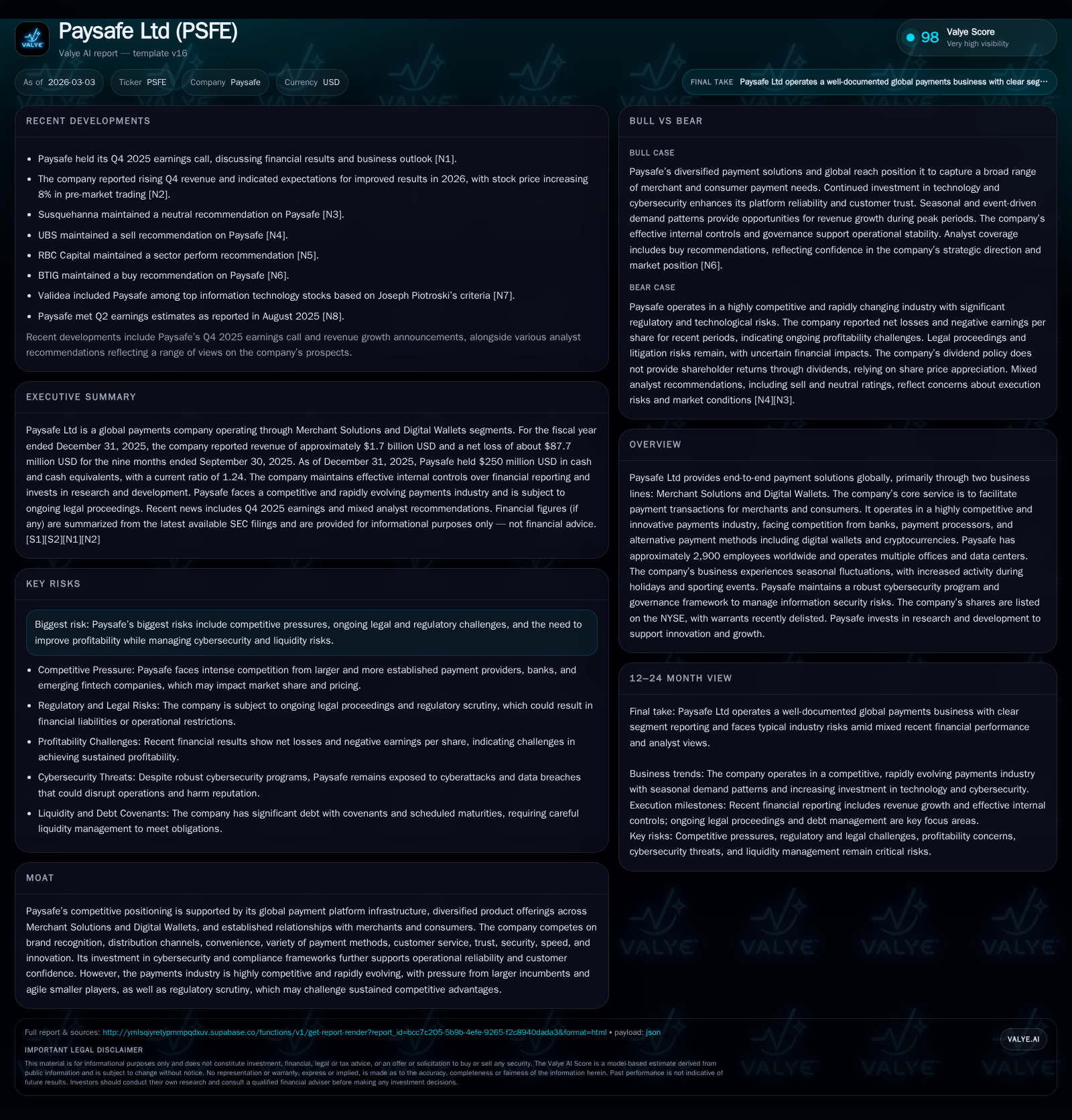

Paysafe Ltd’s Financial Reset and Strategic Growth Trajectory

Paysafe has achieved revenue stabilization amid margin pressures by intensifying R&D investment and executing disciplined capital deployment, setting the stage for sustainable growth.

Paysafe Ltd reported near-flat revenues at $1.7 billion in 2025 with operating income nearly halving, reflecting margin compression despite manageable cost controls. The company’s expansion of its R&D budget highlights a clear strategic bet on innovation, especially in cybersecurity and payment technology enhancements. While competitive and regulatory headwinds persist, Paysafe’s diversified Merchant Solutions and Digital Wallets segments benefit from seasonal tailwinds and global reach. Capital allocation through aggressive share repurchases complements a solid liquidity profile, though returns remain modest. Governance updates aim to strengthen oversight as the company pursues growth amid evolving payments industry dynamics.

Financial Performance: From Volatility Toward Stability

Paysafe Ltd’s top-line exhibited remarkable stability in fiscal year 2025, with revenues reaching approximately $1.7 billion, virtually flat year-over-year (-0.2%) after several years of double-digit growth [F1]. This plateau reflects broader industry trends where payment processing volumes are normalizing following pandemic-driven acceleration, compounded by heightened competition among payment processors and alternative methods.

However, beneath the surface of stable revenues lies a pronounced weakening in profitability metrics: operating income fell sharply by around 46% compared to the prior year, totaling roughly $72 million [F1]. This decline reflects margin compression driven by increased investment in technology infrastructure, transaction-related costs, and regulatory compliance expenditures, all within a highly competitive price-sensitive market. Notably, net income swung back into positive territory in 2024 at $22 million after consecutive loss-making years, suggesting progress toward sustainable operational efficiency albeit on a modest scale [F1].

Operational cash flow remains solid albeit contracted slightly by 7% year-over-year to about $236 million in 2025 [F1]. Capital expenditures scaled back by around one-fifth relative to 2024, settling near $12.6 million, indicating cautious capex discipline amid ongoing technological upgrades [F1]. The resulting free cash flow approximates $224 million, providing ample liquidity for strategic initiatives.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1701 | 236 | 72 | -0.2% | ||

| 2024 | 1705 | 22 | 254 | 133 | +6.5% | +209.4% |

| 2023 | 1601 | -20 | 234 | 159 | +7.0% | +98.9% |

| 2022 | 1496 | -1863 | 924 | -1872 | -1578.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 224 |

| 2024 | 238 |

| 2023 | 221 |

| 2022 | 920 |

Source: SEC companyfacts cache [F1].

FCF estimated as CFO minus Capex; Net Income not available for FY25; Percentages rounded.

Segment Breakdown: Merchant Solutions versus Digital Wallets

Paysafe operates primarily through two business lines: Merchant Solutions — encompassing merchant acquiring services, payment orchestration platforms and settlement processing — and Digital Wallets catering directly to consumer digital money management including stored value accounts and payout services [S1][N2].

Each segment navigates seasonality distinctly: Merchant Solutions typically sees heightened transaction activity during holiday seasons driven by retail promotions backed by merchant marketing initiatives. Digital Wallets experience demand surges tied closely to major sporting events where wagering activity intensifies [S16][S18]. This seasonality necessitates scalable infrastructure capable of managing peak volume spikes without service degradation.

From a competitive standpoint, Merchant Solutions faces pressure from incumbent banks integrating direct acquiring services with their credit/debit networks alongside emerging fintech companies leveraging API-based payment hubs that reduce merchant friction points at acquisition costs optimized through data analytics [S8]. Digital Wallets contend with rapid adoption curves among consumers shifting toward multi-method mobile payments including crypto-enabled wallets and local alternative payment methods (APMs) such as bank-based instant payments prevalent across Europe and Asia markets.

Efficient KYC/AML compliance across both verticals increases onboarding complexity; elevated merchant acquisition costs reflect extended vetting cycles mandated by jurisdictional regulators [S5][S8]. This dual-segment diversity helps mitigate concentration risk but also mandates simultaneous technological innovation investment.

Competitive Landscape and Regulatory Challenges

The global payments ecosystem demonstrates relentless competitive intensity characterized by convergence of financial institutions expanding digital offerings and nimble fintech entrants innovating with blockchain or real-time settlement capabilities [S8]. Large incumbents leverage entrenched distribution channels while smaller players capitalize on agility—this continues to exert pricing pressure on providers like Paysafe.

Regulatory scrutiny intensifies particularly around anti-money laundering laws (AML), Know Your Customer (KYC) protocols and data privacy regulations across multiple jurisdictions where Paysafe operates [S18][S21]. Licensing requirements remain stringent for cross-border operations affecting speed-to-market for new client rollouts or wallet feature expansions.

Legal proceedings remain an area of exposure despite recent dismissal of major securities litigation cases involving allegations tied to disclosure practices and financial outlook guidance [S5][S6]. Managing operational risk attributable to cyber threats is critical given payment data sensitivity; Paysafe maintains layered security controls validated through independent audits aligning with sector best practices in fraud prevention technology [S23][N1].

Innovation Focus: R&D's Role in Future Positioning

A marked strategic shift is evident through Paysafe’s doubling of annual research & development spending—from approximately $7.3 million in both FY23-24 to nearly $15.8 million in FY25—signaling a commitment to robust upgrade cycles of its software platforms [F1][S1]. This elevated investment supports enhancements across payment orchestration capabilities including new API integrations for alternative payment methods, user interface modernization for digital wallet apps targeting adoption among younger demographics, as well as fortified cybersecurity layers designed to mitigate fraud risk.

These efforts also encompass fraud analytics powered by machine learning models able to flag transactional irregularities in real time—a vital asset given the increasing sophistication of cyber threats facing global pay-tech players [N1]. R&D outlays are therefore not just product-facing but integrally linked to sustaining trustworthiness which remains a key competitive differentiator.

Looking Ahead: Growth Prospects and Market Expectations

While explicit forward earnings guidance is absent from Paysafe’s most recent communications [N2], management expresses cautious optimism regarding continued revenue performance improvement in fiscal year 2026 driven by incremental market share gains within both Merchant Solutions and expanded wallet user bases particularly in regulated markets benefiting from tailored compliance frameworks.

Watchpoints include potential expansion into underpenetrated geographies leveraging existing platform architecture combined with partnerships targeting sectors like online gaming or digital entertainment where transaction velocity remains high despite macroeconomic headwinds [N2][S1]. Correspondingly, further developments in incorporating crypto-assets or distributed ledger technology into wallet offerings could unlock differentiation but entail regulatory approval complexities.

Regulatory license renewals remain critical milestones affecting go-to-market continuity especially within European Union states increasingly harmonizing digital payments oversight under revised Payment Services Directive rules [S18]. Faster resolution or adaptation to emerging AML monitoring requirements will influence operational flexibility.

Capital Management: Share Repurchases, Cash Flow, and Returns

In the absence of dividends—Paysafe holds no current plans for regular cash distributions—the company prioritizes shareholder returns through opportunistic stock repurchases. The Board authorized an additional $140 million share buyback capacity during FY25 on top of prior authorizations commencing end-2023 [S4][S19]. Actual share retirements occurred throughout calendar year including significant volumes between March-November averaging prices between $6.74 to $16.32 per share.

Liquidity strength is underscored by year-end cash plus equivalents tally exceeding $250 million coupled with recurring operating cash flow generation (~$236 million) comfortably covering modest capital expenditure needs yielding free cash flow near $224 million annually [F1]. Leverage metrics are stable with facilities drawn primarily via term loans distributed between USD and EUR obligations bearing interest rates ranging approximately from mid-4% to mid-7%, inclusive of effective hedging via rate swap agreements mitigating floating rate variability risks [S9][S10][S11][S12].

Approximate return on equity is constrained near low single digits (~2.6%) reflecting residual earnings pressure linked to investment cycle timing and amortization impacts stemming from historical business combinations [F1]. Nonetheless disciplined capital deployment through buybacks enhances per-share metric trajectories consistent with peer buy-side norms within pay-tech industry fraught with evolving margin challenges.

Governance Reforms and Board Reshaping

Recent governance adjustments have involved board composition changes aimed at reinforcing oversight functions aligned with increased regulatory complexity faced by global operators like Paysafe [S3]. Two director resignations were offset by appointment of four new members expanding the Board size from ten to twelve seats.

Committee leadership was restructured with new chairs assigned across Audit (Ms Heiss), Risk Oversight (Mr Brooker), Compensation (Mr Jabbour), and Nominating & Governance Committees (Mr Keeley), signaling enhanced focus on financial integrity controls alongside talent retention strategies integral to tech-driven payment firms navigating tight labor markets [S3][S19].

This recalibration serves as proactive alignment with best practice standards facilitating timely response mechanisms relative to emergent cybersecurity threats or compliance policy evolution imperative for maintaining investor confidence.

Disclaimer: This analysis is a factual summary based exclusively on public filings ([F1],[S#]) and news transcripts ([N#]) as of early March 2026 related to Paysafe Ltd's reported results and disclosures. It does not constitute investment advice or recommendations nor forecasts beyond stated official sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments