Hyperliquid Strategies Inc: Navigating Massive Losses Alongside Strong Liquidity and Buybacks Amidst Unclear Business Model

Hyperliquid’s financial reporting reveals a puzzling mix of deep quarterly losses, a commanding cash position, and active stock repurchases in the absence of business transparency.

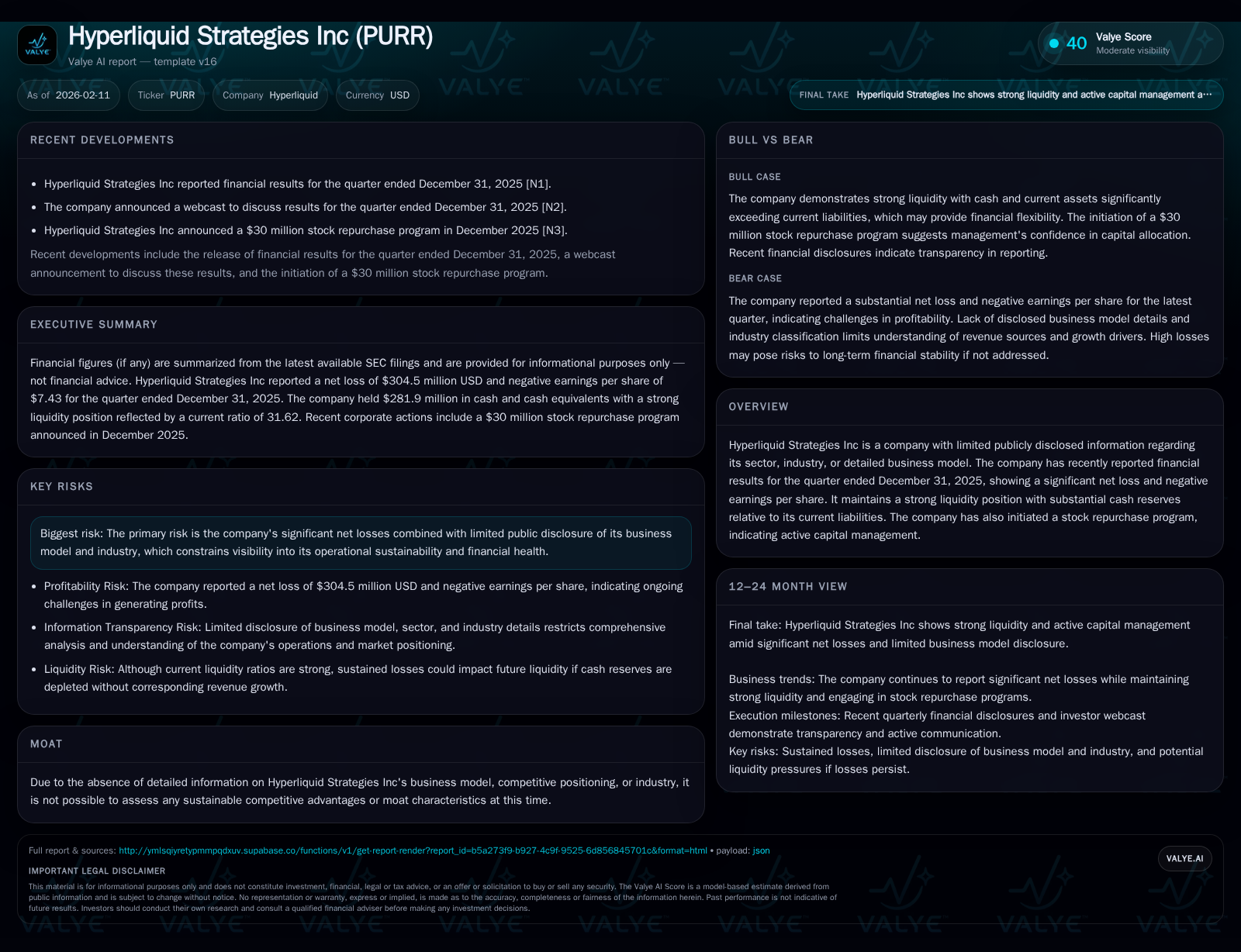

Hyperliquid Strategies Inc disclosed a sharp $304 million net loss for Q4 2025 yet holds substantial liquidity with over $281 million in cash, resulting in an exceptional current ratio above 31. Concurrently, the company has launched a share repurchase program despite operating losses and scarce disclosure about its business sector or operations. This paradoxical positioning complicates external understanding of its strategic rationale and risk profile. Without clear insight into underlying activities, assessing its competitive moat remains impossible, leaving stakeholders to navigate considerable uncertainty.

The Enigma of Hyperliquid Strategies: What Lies Beneath Scarce Transparency?

Hyperliquid Strategies Inc presents an intriguing puzzle for analysts given the near-complete absence of publicly available detail about its sector affiliation, industry context, or core business operations. Official statements and filings avoid defining the company’s exact economic activity, offering only generalized commentary typical of early-stage or highly secretive ventures [N1][S2]. This opacity is critical as it restricts fundamental understanding and traditional valuation frameworks. Without knowing what drives revenue or cost structures, external observers are left piecing together clues from fragmented financial data and sparse corporate disclosures.

This veil complicates assessment of not only growth prospects but also systemic risks tied to industry cycles or regulatory environments. A company whose purpose is unclear invites skepticism about sustainability and strategic direction. The enigma is compounded by the stark contrast between reported fiscal metrics and strategic actions — setting the stage for deeper investigation.

Dissecting the Q4 2025 Financial Fallout: Why the Losses Run Deep

The headline figure from Hyperliquid’s latest quarterly results is an eye-catching net loss totaling approximately $304 million [F1][N1]. This magnitude eclipses typical quarterly swings for companies absent major restructuring or write-downs. The figures also reflect negative earnings per share, underscoring persistent bottom-line pressure with no immediate signs of profitability.

While direct line-item expense breakdowns are limited, such a sizable loss suggests either substantial nonrecurring charges (impairments, asset write-offs) or aggressive investment burn rates exceeding revenue generation. The lack of declared revenue figures or segment reporting leaves the underlying causes ambiguous. Management commentary in planned investor webcasts may shed some light, but until then this loss stands as a red flag illustrating significant operational challenges or strategic gambles yet to pay off [N2][S2].

This financial hemorrhaging contrasts sharply with the solidity implied by balance sheet liquidity — positioning Hyperliquid as a loss-making entity with resources that could potentially fuel continued investment or debt service.

A Fortress of Cash: Evaluating Hyperliquid’s Liquidity Armory

A standout metric from the company's recent filings is its extraordinary liquidity profile. As of December 31, 2025, cash and equivalents totaled roughly $282 million against current liabilities under $9 million [F1]. Resultantly, the current ratio clocks in at an exceptional 31.62 — an outlier among public companies.

This liquidity surplus suggests robust capacity to cover short-term obligations many times over and a financial runway that cushions ongoing losses. However, it also raises questions about capital deployment efficiency and return on cash holdings during periods of sustained negative income.

In isolation, this cash fortress signals resilience and perhaps flexibility to pursue strategic initiatives without immediate funding constraints. Yet without transparency on uses of funds — whether for R&D, acquisitions, or debt repayment — interpretation remains speculative.

Stock Buybacks Amid Financial Pain: Reading Between Capital Management Moves

Perhaps one of the more paradoxical elements is Hyperliquid's choice to inaugurate a stock buyback program concurrent with reporting massive losses [N1]. Typically associated with excess cash flow and shareholder value enhancement after periods of strength, buybacks here might reflect alternative strategic signaling.

One plausible interpretation is management’s belief that shares are undervalued given market misconceptions arising from scant information. Alternatively, buybacks could serve as confidence gestures intended to stabilize market perceptions amidst turbulent results.

However, deploying capital toward repurchases rather than reinvestment or debt reduction during severe losses may invite scrutiny regarding long-term value creation priorities. This bold capital management approach amid financial adversity highlights an unconventional corporate stance warranting close investor monitoring.

Risk Radar: Navigating Uncertainties from Minimal Disclosure to Structural Threats

Hyperliquid explicitly lists significant risks related to limited operational visibility combined with sizable net deficits in its official regulatory filings [S2]. These factors hinder traditional risk analysis techniques; familiar industry benchmarking or peer comparison cannot effectively apply when core business details are missing.

Moreover, ongoing losses exacerbate concerns over sustainability absent known revenue streams or profitability milestones. The informational vacuum elevates uncertainty premiums—investors essentially must contend with undetermined existential risks beyond quantitative metrics alone.

Such disclosure disclaimers underscore the formidable barrier to confident investment thesis formation while highlighting potential vulnerabilities inherent in opaque business models confronted with heavy spending trajectories.

Moat Myth or Reality? The Challenge of Assessing Competitive Edges Without Clear Industry Signals

Conventional diligence involves probing for sustainable competitive advantages—intellectual property, network effects, cost leadership—that underpin defensible profit margins over time. For Hyperliquid, however, such assessments remain unattainable due to missing contextual detail on market position or product uniqueness [valye_report_excerpt].

Without clarity on customer base, technology differentiation, or regulatory protections—elements typically illuminating moats—any measure of competitive durability becomes guesswork. Consequently, valuation models predicated on enduring economic rents falter under inadequate data.

This void leaves stakeholders without standard comfort zones where durable moat signals inform risk-adjusted return expectations.

Strategic Outlook: Weighing What Little Is Known Against Potential Futures

Synthesizing available evidence illustrates a company navigating contradictions: deep losses versus ample liquidity; scarce operational transparency against assertive capital returns; potential strategic intent veiled behind inscrutable filings [N2][S2][valye_report_excerpt].

Management's upcoming webcast promises incremental insight but likely will refrain from comprehensive disclosures given prior patterns. Analysts must therefore balance cautious anticipation against prudent skepticism while watching for trajectory shifts in profitability trends or narrative clarity.

In absence of clearer guidance concerning business fundamentals, any forward-looking views must remain provisional and attentive to liquidity preservation measures alongside evolving loss dynamics.

Ultimately, Hyperliquid serves as a compelling case study on managing informational scarcity within capital markets—a challenge increasingly relevant amid emerging industry disruptions characterized by nascent technologies or confidential competitive environments.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations. The analysis relies on publicly available data as referenced and acknowledges substantial informational limitations inherent in company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments