RGA’s Underwriting Expertise Drives Earnings Amid Regulatory and Market Pressures

RGA achieves robust earnings growth through underwriting excellence and hedging while managing rising regulatory reserves and market volatility.

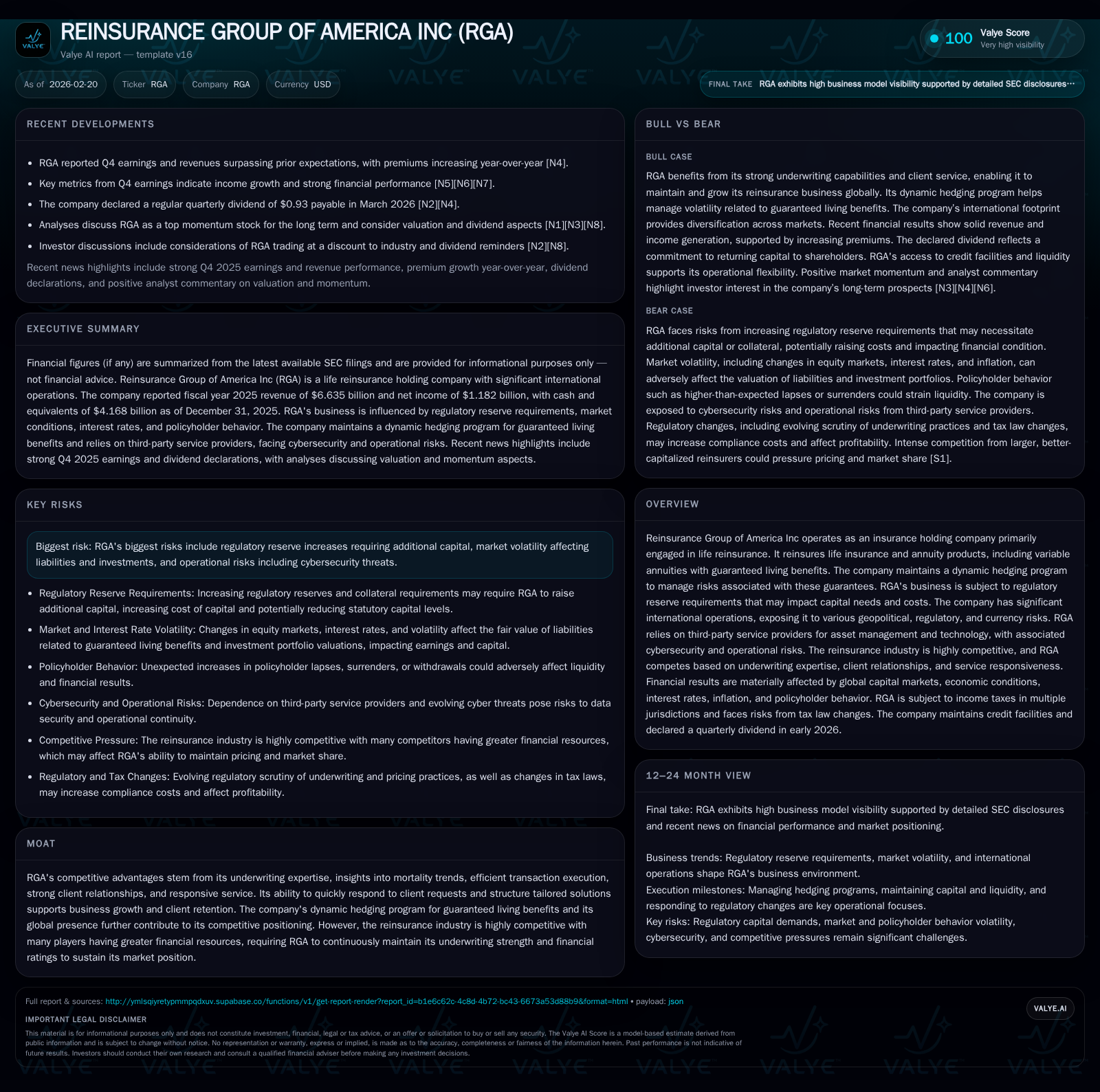

Reinsurance Group of America (RGA) delivered a strong revenue increase of 26.6% in 2025, driven primarily by premium growth fueled by its underwriting capabilities. Net income surged 64.9% year-over-year, reflecting both pricing power and effective dynamic hedging programs mitigating guaranteed living benefit risks. However, escalating regulatory reserve demands under Regulation XXX and collateral requirements for retrocession pose capital constraints that could limit risk appetite going forward. Market fluctuations, particularly in interest rates and credit risks tied to mortgage-backed securities, remain notable hazards. RGA’s global footprint drives growth opportunities amid currency and geopolitical complexities. The company maintains solid financial health with an 8.8% ROE, strong operating cash flows, and steady dividend payments, though buyback programs appear limited recently.

Historical Growth Patterns and Key Performance Drivers

Reinsurance Group of America (RGA) has demonstrated marked financial momentum in recent years, punctuated most notably by its performance in fiscal year 2025. Revenues advanced sharply to $6.635 billion in 2025 from $5.241 billion the previous year—a healthy 26.6% year-over-year increase driven by premium growth largely attributable to life insurance reinsurance and annuity products including variable annuities featuring guaranteed living benefits (GMLB) [F1][N1].

Net income advanced even more swiftly, reaching $1.182 billion in 2025 versus $717 million in 2024 (+64.9%). This surge reflects not only increased volume but improved underwriting execution amidst competitive pressures as well as gains from RGA's dynamic hedging program designed to mitigate volatility related to variable annuity guarantees [F1][S16]. The underwriting franchise's strength is further underpinned by deep insights into mortality trends and capacity for swift transaction execution—key differentiators in a commoditized landscape where nuanced risk evaluation is essential .

Operating cash flow experienced material volatility; although it declined by approximately 56% from an unusually elevated $9.37 billion level in 2024 to $4.09 billion in 2025, it nonetheless remains robust relative to underlying earnings after accounting for nominal capital expenditures ($25 million–$33 million range) [F1]. This oscillation partially reflects non-cash reserve adjustments and timing impacts common in reinsurance cash flows but warrants ongoing scrutiny.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6.6 | 1182 | 4.1 | +26.6% | +64.9% |

| 2024 | 5.2 | 717 | 9.4 | +4.7% | -20.5% |

| 2023 | 5.0 | 902 | 4.0 | -69.2% | +44.8% |

| 2022 | 16.3 | 623 | 1.3 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 240 | 8.8 |

| 2024 | 229 | 6.6 |

| 2023 | 219 | 9.9 |

| 2022 | 205 | 15.0 |

Source: SEC companyfacts cache [F1].

Note: Operating income data unavailable in the provided tags; capex values estimated from available annual data; sharp revenue drop in FY2022 likely linked to divestitures or accounting reclassifications outside narrative.

Regulatory Reserve Challenges and Capital Constraints

A critical headwind for RGA arises from the increasing regulatory reserve burdens imposed under Regulation XXX and principles-based reserving (PBR) regimes mandated for U.S.-based life insurers [S1]. These frameworks compel the holding of higher statutory reserves against mortality and other policyholder risks relative to traditional methods.

The impact cascades through RGA’s capital modeling because ceding insurance companies must hold commensurately higher reserves — increasing ceded reserves on RGA’s books unless collateralized retrocession arrangements are secured from affiliated or third-party reinsurers meeting stringent regulatory criteria [S1]. Availability of such collateral can be intermittent, costly, or restricted during volatile markets, tightening capacity for new business writings or driving up costs.

This reserve accretion elevates capital needs directly, pressuring statutory capital ratios that are pivotal for licensing requirements and rating agency credit assessments [S12]. Should sufficient collateral not be attainable or if retrocession counterparties tighten terms, RGA might be forced to increase its own reserves beyond expected levels — a scenario that could materially dampen statutory capital and curtail growth without fresh equity or subordinated debt issuance [S14]. Notably, term life insurance—a price-sensitive segment—is especially vulnerable as insurers may raise premiums preemptively in response to these costs which could depress volumes upstream impacting RGA’s reinsurances.

Moreover, credit facilities supporting collateral posting are enforced with covenants on net worth and leverage metrics; breach risks add another layer of operational complexity under stressed conditions [S11]. This regulatory overlay creates a persistent constraint balancing growth aspirations against financial prudence.

Market Exposure: Dynamic Hedging and Investment Portfolio Risks

Variable annuities embedded with GMLB expose RGA to pronounced market sensitivities owing to their fair value liability accounting modulated by equity index levels, interest rate shifts, and implied volatility changes [S16]. To address this, RGA operates a bespoke dynamic hedging program aimed at offsetting income fluctuations via derivatives aligned with underlying risks.

While this strategy mitigates variability effectively under normal conditions, residual basis risk remains inherent due to timing lags between liability recalculations and hedge adjustments, extreme market dislocations causing rapid swings, unusual policyholder behavior such as surrenders triggered by rate moves, and imperfect correlation between fund returns versus hedging instruments [S16]. Such factors mean the hedges may occasionally fail to fully neutralize earnings swings necessitating close monitoring.

Investment portfolios comprise a mix of high-grade fixed maturity securities alongside exposures with greater credit risk concentrations such as commercial mortgage-backed securities (CMBS), residential mortgage-backed securities (RMBS), mortgage loans on commercial properties including lifetime mortgages held indirectly through partnerships or funds [S6][S7]. Defaults or increased delinquency rates on these assets could reduce investment income, trigger impairments, or cause realized losses if forced asset sales become necessary due to liquidity strains or policyholder withdrawals.

Geographic or sector concentrations within these real estate linked assets exacerbate risk if macroeconomic shocks disproportionately hit specific regions or property types simultaneously limiting asset disposal options at fair prices during stressed scenarios [S8]. Furthermore, inadequate valuation methodologies amid volatile markets might prompt material write-downs affecting both reported earnings and regulatory capital cushions.

Credit risk also extends beyond direct investments — counterparties in derivatives transactions or collateral arrangements bring potential default exposures that could cascade financially or materially curtail market access upon downgrades or rating actions against RGA itself or major partners [S6].

Revenue Mix and International Business Impact

Life reinsurance remains the backbone of RGA’s revenue base complemented by specialized annuity coverages primarily centered on variable annuities with accompanying guaranteed living benefits product lines resistant yet sensitive to macro-financial shifts [N1][S25]. These products necessitate sophisticated actuarial modeling coupled with complex hedging approaches distinguishing RGA from less specialized peers.

International operations represent a significant portion of premium volume enhancing geographic diversification but also amplifying exposure to non-U.S regulatory regimes that differ substantially in reserving rules, solvency expectations and collateral demands which escalate compliance complexity [S25].

Currency translation introduces additional volatility as fluctuations directly influence reported revenues and earnings given the substantial non-U.S dollar denominated inflows converting back at potentially adverse spot rates impacting quarterly comparisons even if operating fundamentals remain steady.

Political instability or macroeconomic perturbations overseas could upset underwriting assumptions or constrain market access occasionally disrupting revenue streams resulting in uneven quarter-to-quarter results requiring management agility.

Financial Health: Capital Allocation, Dividends, and Buyback Activity

RGA reports an approximate return on equity (ROE) of about 8.8% based on trailing twelve months net income relative to stockholders’ equity as of end-2025 ($13.46 billion equity vs $1.18 billion net income) reflecting reasonable profitability amidst balancing underwriting cycles and capital demands [F1]. This ROE situates the company competitively within life reinsurer peer cohorts given the constraints imposed by regulatory loadings detailed earlier.

Operating cash flow remains robust despite year-over-year decreases—$4.09 billion recorded with relatively low capital expenditure outlays (~$33 million). This produces ample free cash flow supporting ongoing dividends which have consistently increased over the past four years from $205 million paid in dividends in FY22 up through $240 million estimated for FY25 evidencing management commitment toward shareholder returns within prudent limits dictated by statutory restrictions due to subsidiary payout limitations inherent in insurance structures [F1][S17].

Share repurchases have been notably muted recently with only minimal activity reported historically ($25 million repurchase noted Q3-22). Given the demands of rising regulatory capital requirements potentially pressuring surplus levels little substantive buyback has occurred indicating a conservative stance prioritizing balance sheet strength over aggressive capital redeployment currently.

What to Watch: Upcoming Milestones and Analyst Expectations

Absent explicit forward-looking guidance as per recent filings,[N2] several key metrics warrant careful monitoring:

- Regulatory developments influencing reserve models including any rule amendments impacting PBR calculations which could abruptly change capital consumption profiles;

- Investment portfolio performance especially CMBS/RMBS default trends alongside interest rate trajectories since these substantially affect liability valuations on annuity guarantees;

- Premium volumes growth trajectory particularly new business premium inflow trends against possible demand drag from increased pricing prompted upstream by insurer clients reacting to cost inflation driven by regulation;

- Effectiveness metrics around dynamic hedging programs assessing how well market-driven liabilities continue being offset amid evolving rates/volatility patterns;

- Credit rating agency reviews possibly influencing borrowing costs or covenant flexibility may signal changing perceptions around financial strength important for counterparty confidence;

- Management commentary around dividend capacity vis-à-vis earnings stability given constrained capacity posed by regulatory frameworks.

Analyst commentaries note cautiously optimistic outlooks premised on leveraging strong underwriting acumen combined with rigorous risk management though highlight valuation debates tethered closely to uncertainties around reserve trajectory impacts implying investor attention remains focused on capital efficiency trends going forward [N4][N7].

Conclusion: Balancing Competitive Advantage with Risks

RGA’s demonstrated ability to harness its underwriting expertise complemented by sophisticated dynamic hedging strategies underpins its recent earnings acceleration despite challenging external conditions characterized by rising regulatory reserves and heightened market volatility.This competitive moat—rooted deeply in actuarial specialization, transaction agility,and client responsiveness—forms a critical barrier reinforcing its position within life reinsurance globally. Nonetheless,the growing stringency of reserve mandates,enforced collateralization prerequisites,and complex multi-jurisdictional operational footprint impose tangible constraints demanding vigilant capital stewardship alongside nimble asset-liability management.The persistent investment portfolio risks linked particularly to mortgage credit exposures coupled with cyber-security operational concerns underscore ongoing challenges requiring proactive mitigation efforts.In navigating this balance,RGA continues prioritizing financial strength preservation while seeking calibrated growth leveraging its core competencies—a nuanced equilibrium that will shape its trajectory amid evolving industry landscapes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments