Riot Platforms Accelerates Growth with AI Data Center Expansion in Q1

Riot Platforms delivered stronger-than-expected Q1 revenue driven by AI data center initiatives despite ongoing net losses and capital intensity.

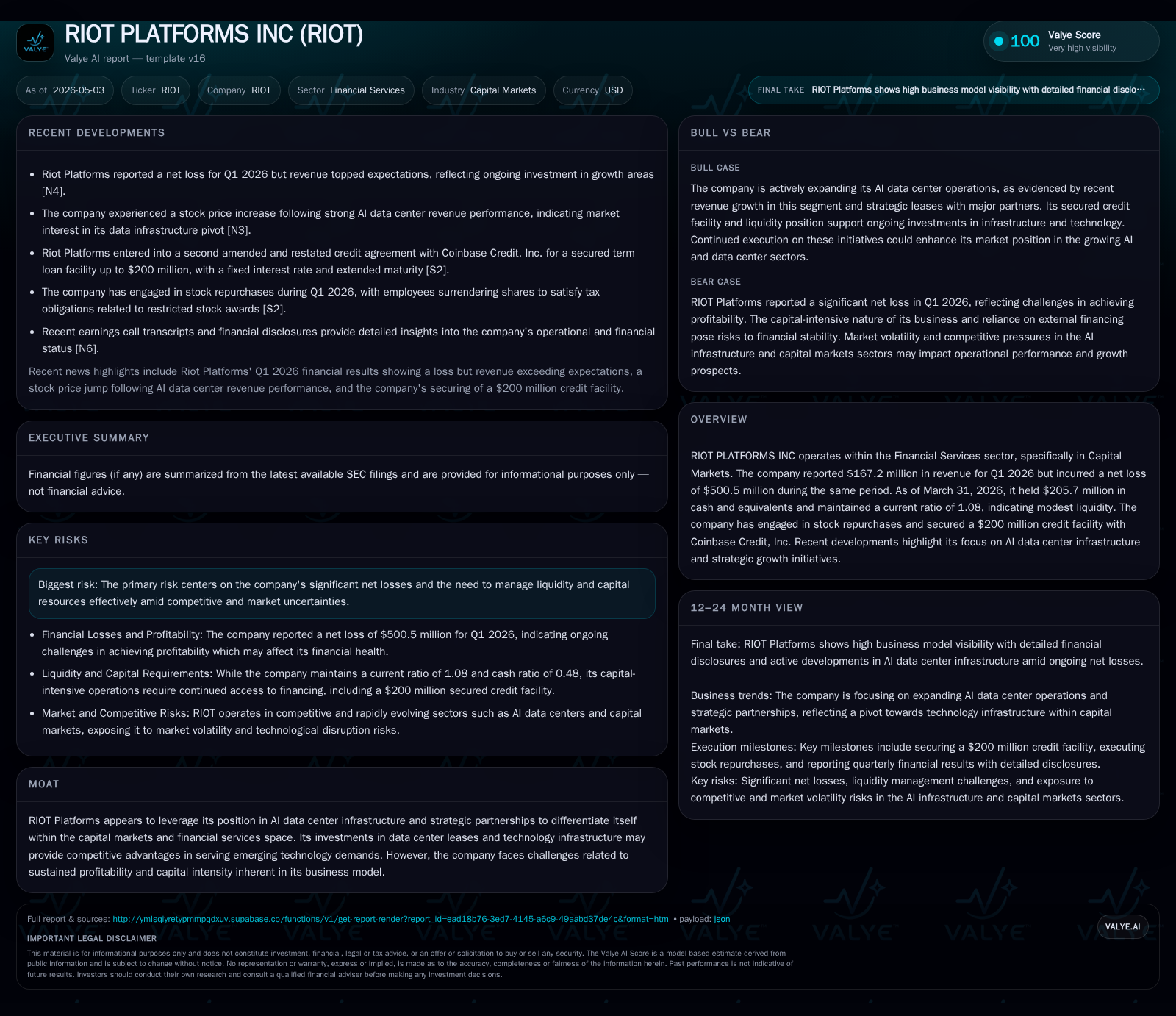

In Q1 2026, Riot Platforms posted $167.2 million in revenue, beating estimates largely through expanding AI data center infrastructure. The company sustained a significant net loss of $500.5 million amid heavy investment in scaling its technology and infrastructure footprint. Riot also secured a $200 million credit facility extension with Coinbase Credit to bolster liquidity. The business is pivoting from traditional capital markets services toward technology-enabled AI infrastructure, leveraging strategic partnerships and data center leases. However, near-term profitability remains challenged by substantial capital expenditures and sector volatility.

Q1 2026 Operating Update: Revenue Beats and Strategic Capital Moves

Riot Platforms reported first-quarter revenues of $167.2 million for the period ended March 31, 2026, exceeding market estimates by capitalizing on its growing footprint in AI data center infrastructure [S2][N4]. This marks a key pivot from its legacy focus on capital market activities toward technology-centric services addressing surging demand for AI workload processing capacity.

Despite the top-line strength, Riot registered a sizeable net loss of $500.5 million, reflecting heavy investments in operational scale-up, infrastructure build-out, and associated expenses [S2][N4]. The disparity underscores the capital-intensive nature of evolving into an AI infrastructure provider while still navigating legacy business complexities.

To underpin this growth strategy and manage liquidity risks from ongoing negative earnings, Riot amended a secured credit agreement with Coinbase Credit, Inc., extending a $200 million term loan facility at a fixed interest rate with maturity provisions that allow further extensions subject to lender consent [S3][S11][S22]. This facility supports Riot’s financing needs as it executes on expanding data center assets.

Business Model and Product Offering: From Capital Markets to AI Infrastructure

Originally rooted in capital markets services within the financial sector, Riot Platforms has progressively transformed into an operator and lessor of specialized data centers optimized for artificial intelligence workloads [S1]. The company generates revenue primarily through leasing high-performance computing space and related infrastructure to customers who require massive computational power for use cases such as machine learning model training.

This shift reflects a recognition of structural industry changes where raw blockchain or trading operations alone offer limited growth compared to the rapidly expanding need for scalable AI infrastructure. Riot’s technical edge rests on owning or leasing critical facilities tailored to energy efficiency and computational density standards necessary for AI applications—a significant value-add over generic data centers [S1][N1].

However, this model entails substantial upfront capital expenditures for building or acquiring these facilities alongside ongoing operational costs tied to power consumption and cooling requirements—factors that contribute to the company’s negative profitability metrics despite promising topline trends.

Industry Positioning and Competitive Dynamics in Financial Services Tech

Within the broader financial services technology ecosystem, Riot occupies a niche intersecting capital markets expertise with advanced IT infrastructure for AI workloads. Key competitive advantages stem from strategic partnerships such as the alliance with Coinbase Credit, which not only provides financing but also integration opportunities across blockchain and digital asset platforms [S1][N12].

Barriers to entry include high capital intensity—securing prime facility locations, managing energy costs—and navigating stringent regulatory environments affecting technology deployment in highly regulated financial domains [S6][S18]. These factors together create a moat that rewards scale players capable of large upfront investments while continuously innovating operational efficiencies.

Customer retention appears anchored on switching costs related to relocating intensive compute operations that depend heavily on uptime guarantees and cooling availability. As demand for AI-ready data centers grows alongside advances in machine learning models requiring extensive computation capacity, Riot's positioning as an early mover aids its competitive stance but also invites acceleration challenges.

Growth Drivers: AI Data Centers, Strategic Partnerships, and Market Adoption

The primary catalyst for Riot’s recent revenue expansion is accelerated adoption of artificial intelligence workloads requiring dedicated high-density compute environments [S2][N14]. These workloads exceed traditional cloud hosting demands due to customized hardware configurations such as GPUs or TPUs optimized specifically for machine learning tasks.

Strategic partnerships not only provide financial backing but also facilitate customer acquisition channels by embedding Riot’s infrastructure offerings into larger ecosystems focused on cryptocurrency trading or digital assets where compute needs converge [N1].

Reported increases in lease contract volumes demonstrate tangible traction in occupancy across Riot’s facilities—a key KPI reflecting growing utilization rates essential both for economics of scale and investor confidence.

Underlying technological shifts toward distributed computing architectures propel continued demand growth beyond cyclical market fluctuations typical of raw capital market services.

Risks and Constraints: Profitability, Capital Intensity, and Market Volatility

Despite compelling top-line momentum, Riot Platforms faces significant challenges relating to sustained unprofitability—as exemplified by the $500.5 million net loss in Q1—and elevated leverage with total debt approximating $853.7 million as of late 2025 against cash reserves of roughly $205.7 million at quarter-end [F1][S2]. This leaves a net debt position exceeding $647 million indicating dependence on external financing.

The reliance on costly credit facilities highlights liquidity sensitivities amid heavy capex cycles needed for next-generation data center construction. Moreover, operating margins remain compressed due to ongoing energy costs inherent in supporting AI workload infrastructures.

Externally sourced risks include regulatory uncertainties impacting financial service technology providers and potential changes in energy pricing regimes all adding layers of unpredictability in cost management.

Execution risks are non-trivial as well; scaling complex facilities without compromising uptime or technical performance benchmarks demands robust project management proficiency alongside evolving cybersecurity protocols specific to financial industry standards.

What to Watch Next: Guidance, Execution Milestones, and Demand Signals

Attention should focus on forthcoming quarterly guidance reflecting the trajectory of AI-related revenue streams versus legacy segments [S2][N6]. Key execution milestones include announcements regarding new data center deployments or expansions under lease agreements signaling sustained demand pickup.

Utilization metrics across existing leased capacity will serve as an important proxy for operational efficiency improvements expected from scale effects.

Additionally, monitoring further strategic partnership developments could provide insight into ecosystem integration success influencing longer-term growth prospects.

The balance between incremental margin improvement initiatives vis-à-vis continued capital spending will be critical indicators of whether Riot can transition toward sustainable profitability.

Latest Financial Snapshot: Liquidity, Debt, and Capital Flexibility

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $206mm | |

| 2026-03-31 | ||

| Total debt | $854mm | |

| 2025-12-31 | ||

| Net debt | $648mm | |

| 2025-12-31 | ||

| Current assets | $463mm | |

| 2026-03-31 | ||

| Current liabilities | $429mm | |

| 2026-03-31 | ||

| Current ratio | 1.08x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD Million) |

|---|---|

| Cash & Equivalents | 205.7 |

| Total Debt | 853.7 |

| Net Debt | 648.0 |

| Current Assets | 462.7 |

| Current Liabilities | 429.3 |

| Current Ratio | 1.08 |

As of March 31, 2026, Riot maintained modest liquidity with a current ratio slightly above 1 at 1.08 supported by $205.7 million in cash reserves against current liabilities totaling approximately $429.3 million [F1]. However, the overall debt load at $853.7 million remains sizeable relative to resources available underscoring reliance on external financing machinery such as the recently amended Coinbase credit facility [S3][S11][S22].

This snapshot contextualizes the delicate balancing act between funding ambitious growth initiatives amid thin margin structures and challenging operating cash flows typical within highly technical infrastructure ventures transitioning their core business models.

This analysis is based solely on referenced SEC filings dated up to April 30, 2026 (), related news reports (), and current company facts snapshot ([F1]). It excludes any speculative interpretation beyond disclosed information or forward-looking investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments