Relmada Therapeutics Advances Controlled-Release Chemotherapy and Neurosteroid Pipeline Amid Clinical Transition

Recent quarterly disclosures confirm Relmada's strategic pivot to NDV-01 and sepranolone, ushering in critical Phase 3 and 2b trial initiations in 2026.

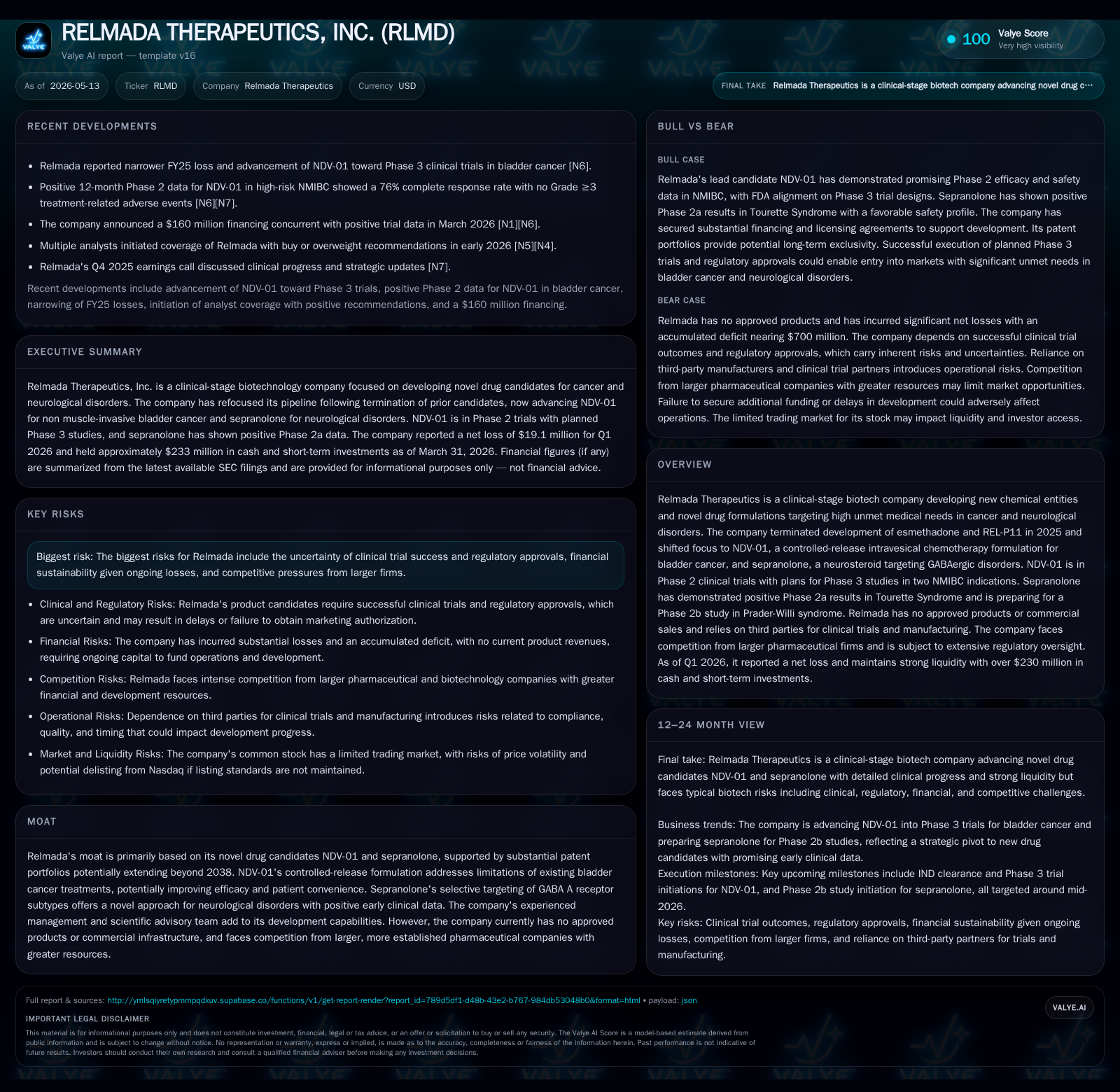

In its latest quarterly filing, Relmada Therapeutics reaffirmed its transformation to focus exclusively on two clinical-stage candidates: NDV-01, a controlled-release formulation for bladder cancer, and sepranolone, a neurosteroid targeting neurological disorders related to excessive GABAergic activity. The company has ceased development of prior drug candidates esmethadone and REL-P11, emphasizing pipeline diversification and risk mitigation. NDV-01 is poised for mid-2026 Phase 3 trials in non-muscle invasive bladder cancer (NMIBC), while sepranolone prepares for a Phase 2b study in Prader-Willi syndrome (PWS). Despite no current commercial products, Relmada’s patent portfolios underpin structural advantages, though clinical uncertainties and funding remain key challenges.

Recent Operating Update

The active programs are progressing toward pivotal milestones: NDV-01 is currently engaged in Phase 2 clinical testing in Israel assessing safety and efficacy against high-risk NMIBC forms with plans to initiate two Phase 3 studies targeting high-risk second-line BCG-unresponsive patients and intermediate-risk adjuvant treatment cohorts by mid-2026 [S1]. This controlled-release intravesical chemotherapy candidate combines gemcitabine with docetaxel to improve drug residence time within the bladder—addressing limitations seen with existing regimens.

Sepranolone targets neurological disorders stemming from excessive GABAergic signaling such as Prader-Willi syndrome (PWS), Tourette Syndrome (TS), essential tremor, among others. Positive Phase 2a results have been reported in TS patients demonstrating significant clinical improvements without systemic or off-target CNS side effects [S16]. A Phase 2b trial for PWS is slated to start mid-year [S16], providing a crucial inflection point for clinical validation across indications.

A contemporaneous corporate presentation update filed alongside the quarter [S3] reaffirmed management’s commitment to execute on these milestones supported by their scientific expertise and newly expanded patent estates.

Business Model

Relmada operates as a clinical-stage biotech firm focused on developing novel chemical entities (NCEs) or advanced formulations addressing significant unmet medical needs primarily within oncology and neurological disease spaces. The company generates no current revenues or profits but relies on equity financings to fund operations. It outsources all clinical trials and manufacturing functions to specialized third-party contractors rather than building internal commercial or production capabilities [S1].

The business model hinges on achieving successful late-stage clinical validation followed by regulatory approvals that could enable commercialization either independently or via partnerships/licensing arrangements. Revenue streams anticipated include upfront licensing fees, milestone payments from partners upon development/approval achievements, royalties from net sales post-launch, or direct sales if commercially viable infrastructure is developed.

Strategically, Relmada leverages patented innovations—such as the sustained-release design of NDV-01 allowing improved delivery of standard chemo agents intravesically—as well as sepranolone’s unique neurosteroid profile modulating specific GABA A receptor subtypes implicated in neurological dysfunctions. However, lacking marketed products means the company must judiciously manage capital allocation toward high-value assets while navigating lengthy regulatory pathways.

Industry Structure and Competitive Position

The specialty pharmaceutical industry where Relmada operates is highly competitive with rapid innovation cycles but also tremendous barriers due to regulatory scrutiny and capital intensity. In oncology—specifically non-muscle invasive bladder cancer (NMIBC)—Relmada faces competition from established players such as Johnson & Johnson through CG Oncology, UroGen Pharma (recently acquired by Pfizer), Soleno Therapeutics, Aardvark Therapeutics, and Protara Therapeutics who offer varying immunotherapy or chemotherapy options [S12]. NDV-01’s competitive edge rests on its controlled-release chemotherapy formulation designed to enhance efficacy and patient compliance over conventional instillations.

Neurological disorder therapeutics like those targeted by sepranolone inhabit niches where current treatments are often symptomatic with incomplete efficacy or tolerability issues. By selectively modulating GABAergic systems via a neurosteroid epimer distinct from allopregnanolone variants already known (e.g., brexanolone), sepranolone posits a novel mechanism potentially addressing core pathophysiology rather than symptoms alone. Successful Phase 2a outcomes augment its differentiation versus other neuropsychiatric therapies often burdened with CNS side effects.

Nonetheless, as a smaller entity lacking commercial scale or broad R&D pipelines compared to multi-billion-dollar pharma companies, Relmada must prioritize capital efficiency while seeking external collaborations for broader market reach post-regulatory approval.

Growth Drivers

Key growth catalysts stem from near-term planned trial initiations which will validate lead asset potential:

- NDV-01 IND Clearance & Phase 3 Initiation: FDA clearance anticipated mid-2026 will enable critical trials evaluating efficacy in BCG-unresponsive high-risk NMIBC patients plus intermediate-risk adjuvant candidates. Positive data here can unlock pivotal registration filings globally.

- Sepranolone Phase 2b Trial Initiation: Commencing mid-2026 in PWS will assess efficacy across core features of this orphan neurological disorder where treatment options remain scant.

- Patent Protection Extending Through at Least 2038: Robust intellectual property exploitation provides exclusivity enabling competitive positioning against biosimilars or generic challengers.

- Advancement of Clinical Data Readouts: Favorable interim analyses or top-line data can fuel partnering discussions or licensing deals enhancing financial runway.

These drivers are structurally supported rather than cyclical; success requires operational execution through trial recruitment, regulatory interactions, data integrity maintenance for submission dossiers.

Risks and Growth Constraints

Risks abound given the early-stage nature:

- Clinical Trial Uncertainty: Both NDV-01 and sepranolone depend heavily on demonstrating statistically significant efficacy endpoints; failure or delay could severely impair valuation.

- Regulatory Hurdles: Changing requirements or interpretation delays may hinder timely marketing approvals impacting commercialization timelines [S1].

- Financial Sustainability: Continuing net losses funded largely by equity dilution necessitate careful cash management; limited cash reserves (~$9.8 million as of March-end) impose runway constraints absent additional fundraising [F1].

- Third-party Reliance: Outsourcing key activities subjects control risks around quality compliance, timing deviations impacting study outcomes or supply chain disruptions.

- Competition from Larger Pharma: Market incumbents wield vast resources for R&D optimization, marketing muscle, potentially crowding Relmada’s market share post-launch [S12].

- Limited Commercial Infrastructure: Absence of sales/distribution capabilities necessitates partnerships which might dilute margins or influence strategic independence.

What to Watch Next

Investors should monitor several execution milestones that could markedly influence ongoing assessment:

- IND clearance decision by FDA for NDV-01 allowing U.S.-based pivotal trial initiation expected by mid-2026 [S1].

- Actual start dates for the two planned NDV-01 Phase 3 studies plus enrollment progression updates confirming recruitment efficiency.

- Launch timeline announcement for sepranolone’s Phase 2b trial in Prader-Willi syndrome scheduled mid-year 2026 [S16].

- Interim or top-line data releases that validate therapeutic hypotheses ahead of registrational study designs.

- Capital raising activities which will be critical given current liquidity levels; progress reports on partnership negotiations could signal future financial stability.

Continued compliance with Nasdaq listing standards including minimum share price thresholds also impacts stock liquidity considerations moving forward [S7].

Financial Profile Briefly Supporting Narrative

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2026-03-31 | ||

| Current assets | $235mm | |

| 2026-03-31 | ||

| Current liabilities | $13mm | |

| 2026-03-31 | ||

| Current ratio | 18.26x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Relmada reported cash & equivalents totaling approximately $9.8 million against current liabilities near $12.9 million yielding an ample current ratio of about 18.26 indicating short-term ability to cover obligations comfortably [F1]. Long-term debt is negligible based on last available data around $110k from end-of-year 2019 metrics implying low leverage exposure [F1]. Operating losses remain significant reflective of ongoing development expenditures—the net loss reported was approximately $57 million for calendar year-end December 31, 2025 indicating continued investment burn ahead of product revenues materializing [F1].

Liquidity is therefore dependent on access to capital markets or strategic partnerships given lack of commercial income—this underscores operating risk amid trial program spending commitments.

Conclusion Disclaimer

This analysis synthesizes publicly available filings up to May 13, 2026. It does not constitute investment advice but aims to provide a structured perspective based on disclosed operational developments combined with industry context. Readers should consult dedicated sources before making any investment decisions related to RELMADA THERAPEUTICS INC.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments