Safeguard Acquisition Corp. Advances Toward Business Combination with Robust Trust Account and Execution Risks

As a recently IPO’d SPAC, Safeguard Acquisition Corp. holds substantial capital ready for acquisition while facing inherent operational and regulatory challenges.

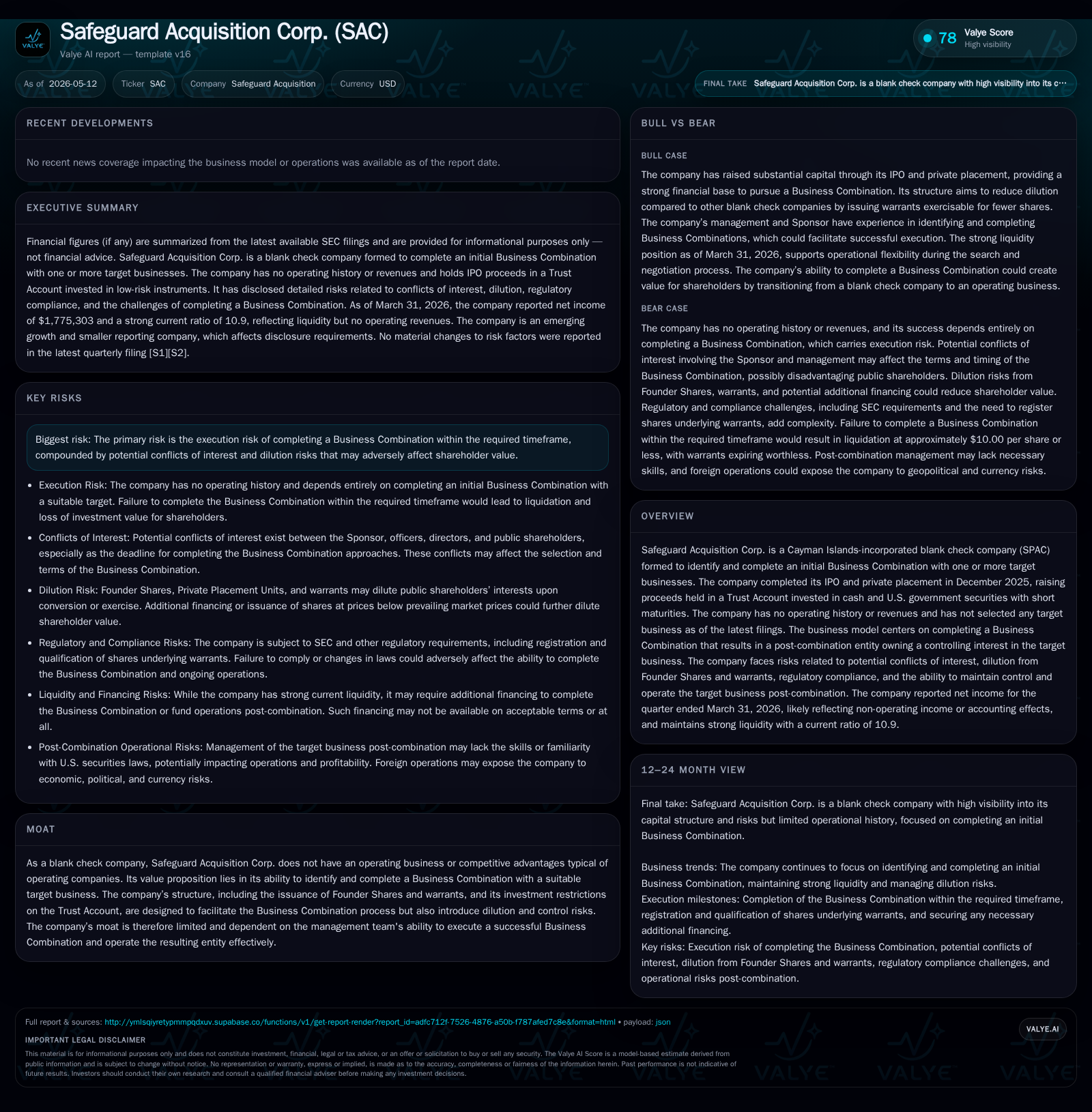

Safeguard Acquisition Corp. (SAC) is a Cayman Islands-incorporated special purpose acquisition company (SPAC) formed in late 2025, with the core objective of completing a Business Combination to transition into an operating entity. The latest quarterly filing confirms no material change in risk profile nor progress toward target identification, reflecting the early stage of SAC’s lifecycle. SAC’s competitive positioning depends largely on management’s ability to finalize a suitable deal within restrictive timeframes, while maintaining shareholder value amid dilution risks. Its business model revolves around deploying approximately $220 million held in trust to acquire controlling interests in target companies, often abroad, necessitating careful navigation of cross-border regulatory and operational complexities.

Recent Operating Update: Early-Stage SPAC Status Maintains Focus on Initial Business Combination

Safeguard Acquisition Corp. reported its quarterly results for the period ending March 31, 2026, marking its first full quarter after an initial public offering concluded in December 2025 [S2]. The filing confirms that the company has not identified any initial Business Combination target nor progressed materially toward consummation beyond deployment readiness. The risk factors disclosed remain unchanged from the annual report filed two months prior [S1], underscoring the nascent stage of SAC's lifecycle as a blank check company operating without revenue or operations.

This status quo is typical for newly launched SPACs where the primary activity centers on capital preservation within trust accounts while pursuing acquisition candidates. SAC's strategic imperative remains clear: successfully identify and complete a combination that yields a controlling interest in one or more targets. The persistent early-stage disclosure signals that the company's near-term operational updates will hinge heavily on transaction developments rather than organic business metrics.

Business Model: Leveraging Capital Markets to Enable Acquisition-Driven Growth

Safeguard Acquisition Corp.'s business model is archetypal of traditional SPACs: it raises capital through an IPO combined with a private placement of units consisting of ordinary shares and redeemable warrants [S1]. Proceeds totaling approximately $230 million were placed into an interest-bearing Trust Account invested primarily in U.S. Treasury securities with short maturities [S22]. These funds are earmarked exclusively for deploying capital into an initial Business Combination or for returning funds to shareholders through redemptions if no transaction occurs by the mandated deadline—24 months from IPO close.

Revenue generation depends entirely on successful identification and closing of one or more Business Combinations resulting in a company controlling voting securities sufficient to preclude investment company status under U.S. laws [S1]. This typically involves acquiring or merging with an operating business domestically or internationally. Until consummation, SAC operates without revenues but incurs administrative expenses funded via limited permitted draws against earned interest on the Trust Account.

Significantly, founder shares held by sponsors represent about 25% ownership excluding private placements [S1], creating incentives aligned with deal closure but also posing potential dilution challenges for public shareholders. Warrants issued to investors carry exercise prices above the IPO price ($11.50 per warrant share), introducing further complexity upon conversion that could affect equity structure post-deal.

Industry Structure and Competitive Position: A Crowded SPAC Market With High Execution Barriers

The SPAC industry remains intensely competitive with numerous firms vying to identify attractive private targets in sectors ranging from technology to consumer products. Given SAC’s recent IPO completion, its positioning relies heavily on management’s expertise in sourcing deals that align both with investor expectations and regulatory scrutiny.

As a blank check vehicle incorporated in the Cayman Islands, SAC faces distinct governance dynamics including specific shareholder approval thresholds tied to issuance of new shares exceeding 15% in combinations [S1]. This impacts deal structuring flexibility compared to U.S.-incorporated peers who may have different legal regimes.

Moreover, post-combination operational risks are magnified given typical cross-border targets — exposing SAC's future portfolio to political, economic, currency volatility issues as well as compliance with regulatory regimes outside the U.S. Management's capacity to manage these multi-jurisdictional challenges will critically shape long-run viability beyond mere transaction execution [S6].

Growth Drivers

The sole growth driver for Safeguard Acquisition Corp. lies in its ability to close an initial Business Combination successfully within mandated deadlines. If executed well, this will convert SAC's funds from passive holdings into operational revenue streams generated by the acquired entity.

Key mechanisms driving potential upside include:

- Capital Deployment Efficiency: Using nearly $220 million held securely in trust at Q1-end offers ample firepower for sizeable transactions consistent with regulations limiting multiple combinations [F1].

- Sponsor Expertise: The board's ability to leverage industry relationships and due diligence capacity can enhance quality of prospective deals.

- Timing Leverage: Early-stage status allows SAC greater choice among targets before rival SPACs exhaust viable pipelines.

- Warrant Structures: Potential future inflows from exercised warrants could provide incremental capital albeit at dilution cost.

- Cross-Border Opportunities: Access to international targets potentially broadens addressable markets beyond domestic saturation.

Risks and Watchpoints

Numerous constraints temper SAC’s pathway:

- Execution Risk: Failure to complete a qualifying Business Combination by December 2027 leads to automatic liquidation and return of funds minus expenses [S1].

- Limited Shareholder Influence: Public shareholders may lack meaningful voting power if management opts out of approval votes per NYSE rules; redeeming shares remains their principal protective mechanism [S1].

- Dilution Risks: Founder Shares retention plus warrant exercises diminish public equity stake post-deal affecting valuation continuity [S1].

- Regulatory Compliance: Evolving SEC requirements increase administrative burdens and may delay transaction timing or increase costs [S4].

- Cross-Jurisdictional Complexities: Foreign acquisitions expose SAC to unfamiliar regulatory environments risking adverse political/economic shocks impacting performance [S6].

- Cybersecurity Exposure: As reliance on third-party digital systems grows during transaction phases, vulnerability to cyberattacks exists despite no internal operations currently [S13].

What to Watch Next

Critical forthcoming milestones include:

- Announcement of Target Engagements: Public disclosures around prospective acquisitions would mark tangible progress beyond capital preservation phases.

- Shareholder Approval Procedures: Whether SAC opts for tender offers vs formal meetings signals anticipated deal complexities and shareholder relation strategies.

- Any Amendments Impacting Warrants or Founder Rights: Changes here affect dilution calculus post-combination [S19].

- Regulatory Developments Affecting Transaction Timelines: SEC commentary or rule changes could impose additional hurdles.

- Capital Deployment Decisions/Use of Trust Account Funds: Actions here will reveal management's confidence levels concerning deal pipeline strength.

Financial Profile: High Liquidity Backed by Trust Account Assets Supports Operating Readiness

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $1481726 | |

| 2026-03-31 | ||

| Current liabilities | $135885 | |

| 2026-03-31 | ||

| Current ratio | 10.9x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As a newly formed acquisition vehicle devoid of operations, Safeguard Acquisition Corp.’s financials reflect its investment holding status rather than earnings generation:

This strong liquidity position is anchored by cash equivalents preserved within the Trust Account used exclusively for merger transactions or shareholder redemptions [F1]. Operating income was negative at approximately $193K as expected due primarily to administrative expenses since inception; net income includes unrealized gains from investments totaling roughly $334K measured at year-end 2025 [F1]. Capital structure features common shares issued through IPO combined with founder shares controlled by sponsors that carry voting influence but dilutive potential when warrants convert.

Disclaimer

This analysis is strictly informational based on publicly available filings as of May 2026 and does not constitute investment advice or recommendations. Market conditions can evolve rapidly; readers should consult qualified financial professionals before acting on any information herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments