Seadrill Ltd’s Recovery Tested by Market Volatility and Contract Backlog Dynamics

Post-bankruptcy Seadrill contends with market softness, shrinking backlog, and disciplined capital allocation amid offshore drilling cyclicality.

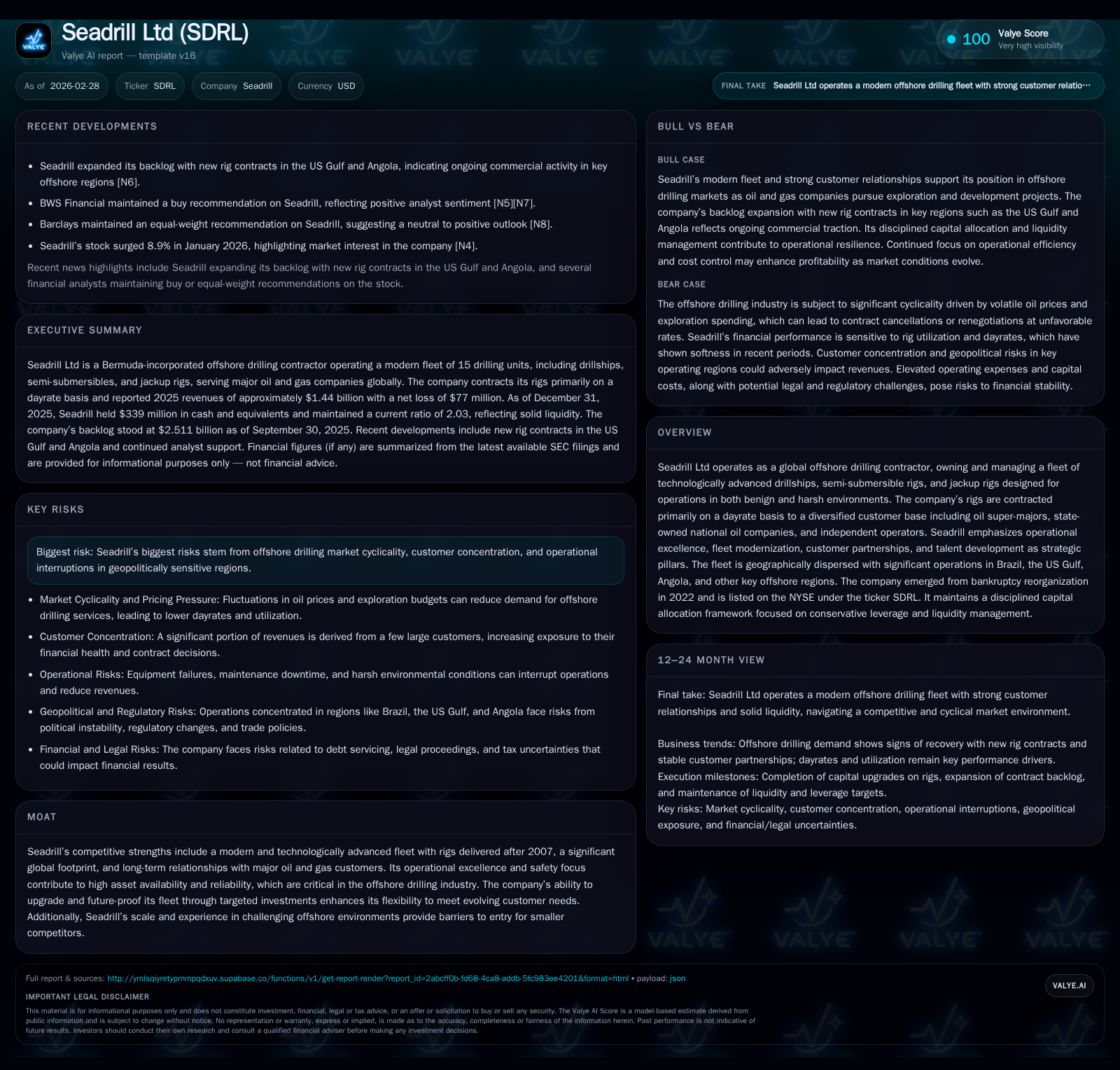

Seadrill Ltd emerged from its 2022 bankruptcy reorganization with a modern offshore drilling fleet and global operational scale. While revenue grew modestly by 3.8% in 2025, profitability sharply declined due to lower rig utilization and dayrates, resulting in an operating income fall of 88.6%. The company’s contract backlog shrank about 21% over the first nine months of 2025, signaling near-term revenue pressures. Despite these headwinds, Seadrill maintains a strong liquidity position though free cash flow turned negative as capital expenditures increased. Future growth hinges on a recovering offshore market balanced against persistent macroeconomic uncertainties and continued customer concentration risks.

Renewed Scale Post-Bankruptcy: Fleet Composition and Operational Footprint

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1437 | -77 | -28 | 47 | +3.8% | |

| 2024 | 1385 | 88 | 412 | -7.8% | ||

| 2023 | 1502 | 287 | 329 | +78.2% | ||

| 2022 | 843 | 201 | 65 | 35 | +134.2% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | -2.7 |

| 2024 | 532 | |

| 2023 | 263 | |

| 2022 | 13.4 |

Source: SEC companyfacts cache [F1].

Seadrill Ltd exited Chapter 11 bankruptcy proceedings in early 2022 and swiftly positioned itself as a leading global offshore drilling contractor with an updated asset base. As of December 31, 2025, the company owned a total of 15 drilling units across various configurations: six seventh-generation drillships, two sixth-generation drillships, one benign environment semi-submersible floater, and one harsh environment jackup actively operating; three rigs remained cold stacked while others underwent upgrades or maintenance projects [S1,S2]. This modern fleet profile reflects targeted management efforts to maintain technologically advanced rigs capable of ultra-deepwater and harsh environment operations—sectors demanding high operational reliability and safety.

Geographically, Seadrill's operations span key offshore activity zones including Brazil (a core region hosting multiple drillships), the U.S. Gulf of Mexico, Angola, Norway, Namibia, and Singapore among others [S12]. The company also manages two rigs owned by Angolan state oil company Sonangol EP—a partnership highlighting its trusted operator status [S1]. This global footprint provides operational flexibility allowing redeployment based on prevailing basin economics.

Operational excellence remains a strategic pillar for Seadrill, critical in addressing logistical challenges associated with harsh environments such as North Sea jackups or Brazilian deepwater drillships where weather volatility and technical complexity prevail. This positioning undergirds barriers to entry against smaller competitors who may lack capital for similarly advanced fleets or experience navigating complex regulatory landscapes.

Revenue Growth Meets Profitability Pressure: Analyzing 2025 Performance

In financial terms, Seadrill reported revenues of approximately $1.44 billion for fiscal year 2025—a moderate increase of roughly 3.8% compared to $1.39 billion in 2024 [F1]. However, this topline growth starkly contrasts with a precipitous decline in operating income which fell to $47 million from $412 million year-over-year—an erosion of about 88.6% [F1]. Net income swung into loss territory at -$77 million in 2025 versus prior profits [F1].

This margin compression largely traces back to weaker dayrates driven by softer rig utilization globally—especially among benign environment floaters which constitute the larger portion of Seadrill's active fleet—and increased inflationary pressures on crew wages, fuel costs, and maintenance expenditures [S1]. The Management Discussion notes decelerating demand translated into intensified competition pushing dayrates downwards while costs remained sticky resulting in shrinking operating leverage.

Operating cash flow moved into negative territory at ($28) million for the year compared with positive $88 million previously—a swing indicative of immediate cash generation challenges faced by offshore contractors during cyclical downturns [F1]. Meanwhile capital spending accelerated notably with capex rising over 150% year-over-year to support rig reactivations and compliance modifications ahead of contractual starts (e.g., Petrobras contracts) [F1,S1]. This investment spike further compressed free cash flow estimated at -$242 million (operating cash flow less capex) for the period.

The juxtaposition between solid revenue resilience amidst stark profitability declines signals short-term softness within contracting environments but preserves long-term commercial viability through fleet readiness.

Market Environment: Dayrate Trends, Rig Utilization, and Macro Risks

Offshore drilling remains inherently cyclical with dayrate fluctuations heavily influenced by broader commodity prices and exploration budgets. In 2025 Brent crude averaged roughly $68 per barrel down from $80 the prior year—pressuring operators' capital allocation decisions and leading to subdued tendering activity for offshore rigs globally [S1].

RigLogix data corroborates declines in marketed utilization rates across most rig classes: benign floaters saw utilization drop from 87% to 86%, harsh environment floater utilization fell from 95% to 93%, while jackups slipped from near-peak highs at around 99% to approximately 97% within the same interval [S1]. The decline was more pronounced particularly among benign environment semi-submersible rigs that tend to be vulnerable during soft markets given their lower technical specifications relative to premium deepwater drillships.

Additional macro risks compound this softness including ongoing uncertainty relating to U.S. trade policies provoking market volatility; inflation driving up operational expense lines; OPEC production decisions impacting supply-demand balance; and lingering geopolitical tensions influencing areas like Angola where Seadrill operates [S1]. These factors collectively stifle immediate offshore exploration appetite though long-term fundamentals remain supportive given shifting energy security priorities.

Contract Backlog Contraction and Its Implications for Future Revenues

A critical indicator of forward revenue visibility—the company's contract backlog—demonstrates tangible pressure as it declined approximately 21% from about $3.18 billion at December 31, 2024 down to $2.51 billion at September 30, 2025 [S2]. Drilling contracts comprised most of this backlog ($2.28 billion) with 'other' management fees making up the remainder.

Backlog reductions reflect completed contracts not immediately replaced at comparable dayrates or durations amidst slower tendering markets. It is noteworthy that many contracts include complex dayrate variability mechanisms such as waiting-on-weather rates or suspension clauses that can reduce effective dayrates if rigs face extended downtime or force majeure events—all prevalent issues during soft demand cycles [S2,S20].

Seadrill estimates roughly half the backlog maturing beyond near term into years beyond 2026; however precise revenue realization will depend on rig reactivation timing amid maintenance schedules along with customer fractional take-up as contract terms mature or options are exercised. The ~21% contraction accentuates near-term top-line caution while underscoring the necessity for stabilizing tender activity to support long-run revenue growth.

Capital Allocation Choices: Buybacks Reversed, Cash Flow Challenges, and Strong Liquidity

Seadrill's capital allocation strategy has pivoted significantly since emerging from restructuring optimism highlighted by aggressive share repurchase programs executed during late-2023 through much of 2024 totaling over $532 million spent buying back stock but ceasing completely entering 2025 as cash preservation took priority amid deteriorating liquidity metrics [F1,S5,S10].

As of December 31, 2025 liquidity remains healthy with unrestricted cash balances of approximately $339 million supported by an undrawn revolving credit facility amounting to $185 million—total available liquidity hovering near $524 million—and a current ratio exceeding two times ($758 million current assets over $374 million current liabilities) demonstrating satisfactory short-term solvency coverage levels despite operational cash flow weakness [F1,S10,S18].

Nevertheless free cash flow turned negative due largely to higher capital expenditures directed towards rig upgrades preparing rigs like West Auriga and West Polaris for new assignments under Petrobras contracts—a strategic choice aimed at longer term asset quality rather than short term payout expansion [F1,S11]. Dividends remained suspended consistent with the cautious stance adopted amid ongoing market uncertainty.

The cessation of share repurchases coupled with an elevated capex regimen highlights management’s balancing act prioritizing liquidity preservation alongside maintaining rig competitiveness amid cyclical trough conditions.

Future Growth Outlook: Market Recovery Signals vs. Consumer Caution

Although explicit guidance for Seadrill’s full year outlook is limited beyond SEC disclosures covering updated backlog figures through late-2025 and qualitative commentary on industry conditions [S21], there are nascent signs pointing toward market recovery materializing circa calendar year 2027 per company assessment anchored on acceleration in deepwater exploration tendering activities by oil super-majors combined with plateauing U.S shale output encouraging renewed investment offshore [S1,N5].

This prospective upswing is tempered however by persistent headwinds relating to slow global economic growth forecasts within major markets coupled with inflationary burdens raising operational costs alongside unresolved geopolitical risks including trade policy flux impacting international supply chains—factors fostering prudence amongst E&P operators presently regarding aggressive capital deployment.

Hence Seadrill's outlook embodies cautious optimism emphasizing monitoring ongoing tender pipelines alongside customer preferences while preserving operational flexibility necessary for navigating fluctuating demand profiles typical of offshore drilling cycles.

Navigating Offshore Cyclicality: Operational Strengths as a Moat

Seadrill’s strategic advantages coalesce around its modernized fleet profile—reflected in predominantly post-2007 build dates encompassing sixth- and seventh-generation drillships equipped with cutting-edge subsea drilling capabilities—and robust safety governance underpinning industry-leading asset availability metrics even under harsh environmental conditions often encountered offshore Brazil or West Africa locales.

Its diversified portfolio spans both benign floaters typically favored for shallower waters and harsh environment assets designed for more challenging geographies including jackups capable of operating amid North Sea weather extremes—a fleet mix conferring multi-generational upgrades that enhance customer appeal across various contract windows.

Longstanding relationships dating back years cultivate trust among leading clients including Petrobras—accounting alone for over one-third of revenues in recent periods—and Sonadrill; these partnerships emphasize not only reliability but also bespoke management services extending beyond rig operation into joint venture collaborations elevating business synergies [S4].

Contract frameworks leveraging complex dayrate constructs incorporating escalation clauses tied to cost indices alongside suspension penalties further mitigate pricing downside risk preserving moderate revenue visibility during transient softness typical for this sector.

While cyclical headwinds remain potent as evident from recent financial results trends—including declining utilization rates forcing dayrate concessions—these intrinsic competitive moats provide resilience protecting market position until macroeconomic conditions normalize enabling upticks in exploration capex cycles beneficially impacting tenders going forward.

This report focuses exclusively on factual company disclosures extracted from official SEC filings augmented by recent analyst observations without incorporating any form of investment advice or price forecasting projections. Readers should consider fundamental cyclicality inherent in offshore drilling alongside highlighted risk factors disclosed by Seadrill Limited that could materially impact future financial outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments