SES AI CORP Accelerates Revenue Growth and Scales Manufacturing with Strategic Partnerships and AI-Driven Innovation

SES AI leverages superintelligent AI and recent acquisitions to expand lithium battery technology amidst ongoing losses and scaling challenges.

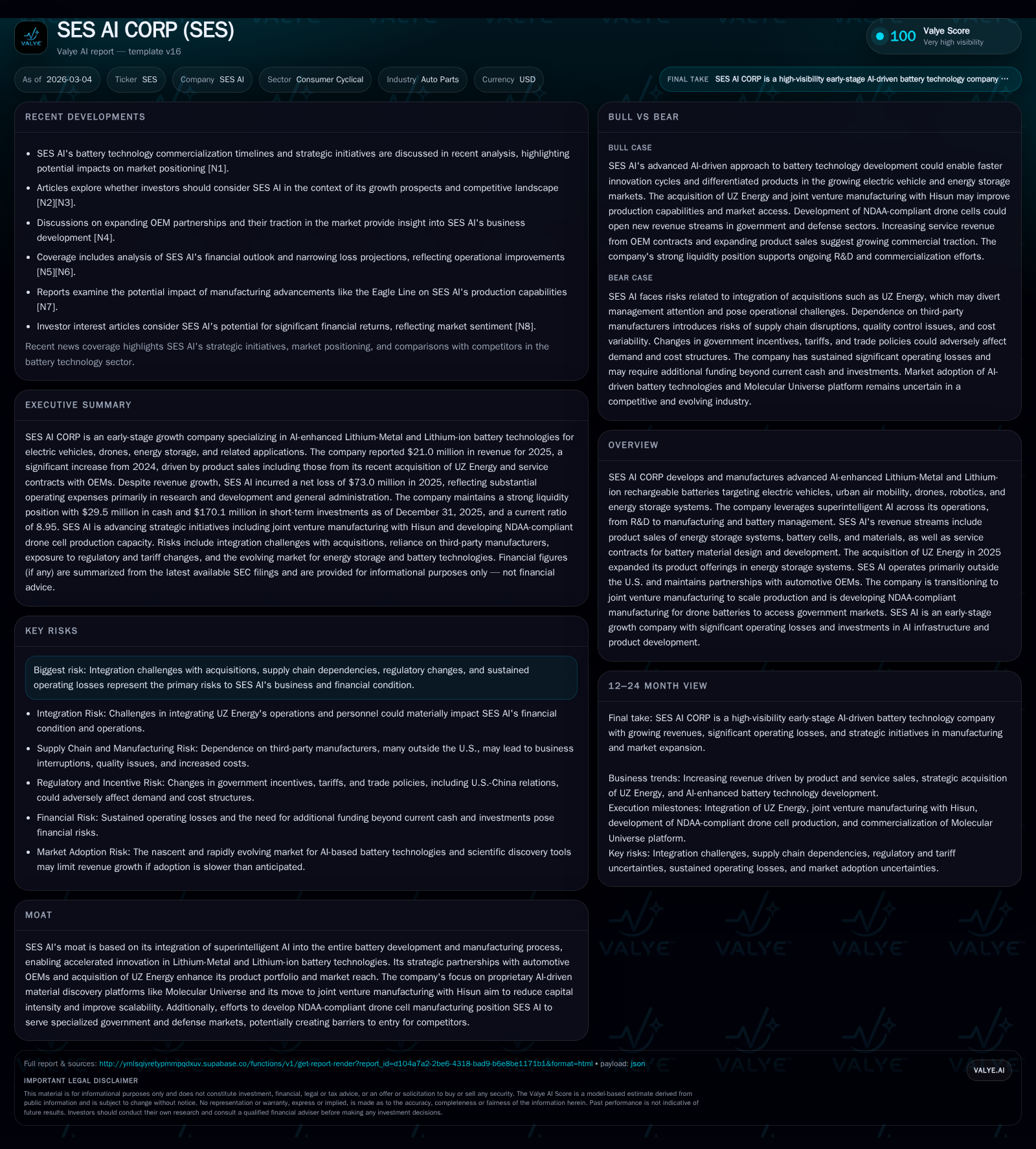

SES AI CORP, an early-stage growth company specializing in AI-enhanced lithium-metal and lithium-ion batteries, recorded a ninefold revenue increase in 2025 driven by acquisitions and expanded service contracts. The company's strategic acquisition of UZ Energy bolstered its energy storage system offerings while its shift to joint venture manufacturing with Hisun aims to improve scalability and reduce capital intensity. Despite improving operating losses, SES AI continues to face significant R&D expenses, integration risks, and a cash burn profile, all supported by substantial liquidity from cash equivalents and marketable securities. Future growth hinges on successful commercialization of its Molecular Universe platform, expansion into NDAA-compliant drone battery production, and effective execution of joint ventures.

Company Overview

SES AI CORP operates within the consumer cyclical sector under the auto parts industry but distinctively concentrates on advanced AI-enhanced lithium-metal and lithium-ion rechargeable batteries targeting electric vehicles (EV), urban air mobility (UAM), drones, robotics, and energy storage systems (ESS). It integrates superintelligent AI at key junctures including R&D, manufacturing, and battery management systems, positioning itself at the intersection of cutting-edge materials science and artificial intelligence.

The company has diversified its revenue streams across product sales—including battery cells, energy storage systems (particularly after acquiring UZ Energy)—alongside service contracts focused on battery material design for automotive original equipment manufacturers (OEMs) and other industrial customers.

Historical Performance

Revenue Growth Drivers

SES AI's most striking financial feature is its dramatic top-line expansion during the fiscal year ending December 31, 2025. Total revenue increased approximately 929% from $2.04 million in 2024 to $21.0 million in 2025 [F1], largely fueled by two pivotal factors:

- The September 15, 2025 acquisition of UZ Energy ([S1], [S20]), a China-based battery energy storage manufacturer that contributed significantly to product revenues.

- A full year of increased service contract activity focused on battery design & development services primarily contracted with automotive OEMs ([S9]).

Service revenues jumped from about $2.0 million to $13.6 million (+~580%), while product revenues simultaneously grew from approximately $0.1 million to $7.4 million mostly due to UZ Energy ESS system sales ([S9]).

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -73 | -58 | -83 | 3 | +27.1% |

| 2024 | -100 | -66 | -109 | 12 | -87.6% |

| 2023 | -53 | -56 | -78 | 16 | -4.7% |

| 2022 | -51 | -46 | -80 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -61 | -34.0 |

| 2024 | -78 | -36.0 |

| 2023 | -72 | -14.9 |

| 2022 | -61 | -13.0 |

Source: SEC companyfacts cache [F1].

Elevated operating expenses reflect the business’s early-stage growth phase with vigorous R&D investment while general & administrative reductions highlight efficiency gains from headcount optimization ([F1],[S14]).

Margins & Profitability Trends

Gross margin declined from approximately 63% in 2024 to about 53.8% in 2025 ([S5],[S9]). This margin compression stems primarily from:

- A higher revenue mix weighted towards hardware-intensive ESS products acquired via UZ Energy with lower gross margins relative to software-driven services.

- Scaling costs associated with nascent manufacturing ramps.

Despite increased scale leading to a narrowing loss from operations (-$82.6 million vs -$109.2 million), SES AI remains unprofitable as it aggressively invests in technology development and business expansion initiatives ([F1], [S19], [S23]).

Future Growth Prospects

SES AI’s growth trajectory hinges on several strategic catalysts detailed below:

Commercialization of Molecular Universe Platform

This proprietary AI-driven materials discovery platform represents a potentially transformative revenue and margin lever ([S1], [S20]). It is designed both as standalone software and integrated tightly into SES’s hardware offerings for differentiated customer solutions across EV, drone, and other applications.

SES expects Molecular Universe adoption to drive revenue growth through new client wins and improved gross margins via intellectual property differentiation ([N1],[N2],[N3]), though the nascent market for AI scientific discovery tools introduces uptake uncertainties ([S20]).

Scale through Joint Venture Manufacturing with Hisun

A strategic shift directs SES away from solely internal manufacturing towards a joint venture partnership model with Hisun to produce novel lithium battery materials commercially ([S1],[S20]). This move aims to:

- Reduce capital intensity typically associated with battery cell manufacturing.

- Accelerate new product time-to-market cycles.

- Scale production capacity more rapidly across global markets.

Risks include exposure to third-party quality control variances, supply chain complexities, and potential production bottlenecks early in ramp-up phases ([S20]).

NDAA-Compliant Drone Battery Production for Government/Defense Markets

Developing manufacturing capabilities compliant with National Defense Authorization Act (NDAA) standards positions SES AI uniquely for drone cell supply within sensitive government ecosystems ([S1],[S20]). This initiative could unlock a high-value niche segment but demands significant capital outlays without guaranteed demand timelines.

Expansion of Product Portfolio Post UZ Energy Acquisition

Integration of UZ Energy has broadened SES’s footprint into residential/commercial ESS markets beyond pure materials science innovation ([S20],[S22]). Synergies are expected between the acquired ESS systems expertise and SES’s core tech platforms fostering cross-selling opportunities.

Forecasts / Milestones / What To Watch (Analysis)

While explicit forward guidance has not been published beyond general commentary on strategic priorities ([N#],[S#]), key milestones likely to influence SES’s outlook include:

- Commercial-scale production capacity achievement for joint venture Hisun manufacturing.

- Market adoption rates for Molecular Universe platform software solutions.

- Successful launch of NDAA-compliant drone batteries capturing government orders.

- Revenue contributions from broader deployment of UZ Energy products outside China. Tracking progress on these fronts will provide insight into delivery against strategic objectives.

Returns / Capital Allocation Profile

Returns & Profitability

Relative to equity of approximately $214.8 million at end-2025 ([F1]), SES reported net loss of roughly $73 million implying an approximate return on equity near -34%. Operating losses declined versus prior year indicating progress but sustained heavy investment pressures remain.

Cash Flows & Liquidity Positioning

Operating cash flow burn remains substantial at -$58.4 million for FY25 despite improvement y/y compared with the prior year (-$66.1 million), underscoring ongoing investment phases ([F1]). Capital expenditures dropped markedly (over 75%) mainly owing to decreased investments in physical plant concurrent with pivoting resources towards AI infrastructure expenditure ([F1],[S23]).

Year-end cash balances stood solid at approximately $29.5 million plus a sizeable portfolio (~$170 million) of short-term U.S Treasury securities providing financial runway exceeding twelve months per management commentary ([F1], [S12], [S16]). This robust liquidity supports SES's R&D-intensive model as it scales commercial initiatives.

Capital Deployment Strategy & Shareholder Returns

SES has authorized a stock repurchase program up to $30 million but did not repurchase shares during Q4 2025 after modest activity earlier in the year; no dividends have been paid nor are planned given reinvestment focus ([S7]). Share-based compensation expense is significant though trending down reflective of workforce adjustments aligned with strategic realignment towards AI-centric efforts ([S17]).

Industry Context (Analysis)

The broader lithium battery industry remains highly competitive characterized by rapid technological evolution amid increasing demand driven by electrification trends across transportation and energy sectors globally. Integration of advanced AI accelerates innovation cycles but requires balancing scale-up challenges against cost structures sensitive to raw material sourcing risks common across participant peers. SES’s reliance on partnerships reflects sector best practices as many players seek flexible capacity expansions while managing multi-geography supply chains complicated by regulations such as NDAA compliance for defense-related usage.

Risks Summary

Key risks include:

- Execution risks incorporating UZ Energy including retention/integration of key personnel capable of sustaining growth momentum ([S2],[S20]).

- Supply chain disruptions related to third-party manufacturing dependencies inherent in joint ventures ([S20]).

- Uncertain market acceptance pace for new Molecular Universe software offerings given the emergent landscape for AI-driven scientific platforms ([S20]).

- Regulatory shifts impacting market accessibility particularly concerning ESS pricing competitiveness vis-à-vis local utility rate changes affecting customer economics ([S2]).

- Sustained losses requiring potential future financing rounds despite currently healthy liquidity reserves ([F1],[S12],[S16]).

Conclusion

SES AI CORP sits at an intriguing nexus of advanced lithium battery material science innovation integrated deeply with superintelligent AI platforms supporting next-gen EVs, drones, urban mobility, and energy storage markets globally outside the United States primarily. The company’s robust revenue scaling—propelled by strategic acquisitions like UZ Energy—and operational pivots towards joint ventures underline its intent to resolve capital intensity issues while broadening market access. However, measured by persistent losses combined with integration complexity and developing commercialization milestones like Molecular Universe adoption or NDAA capabilities rollout, SES remains an early-stage growth entity navigating considerable operational risks amid promising technological catalysts. Monitoring execution progress on these fronts alongside maintaining solid liquidity will be critical factors shaping SES's path forward through its transition phase towards scaled profitability.

This analysis is based solely on publicly available information as of March 2026 including SEC filings and relevant news articles without providing any investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments