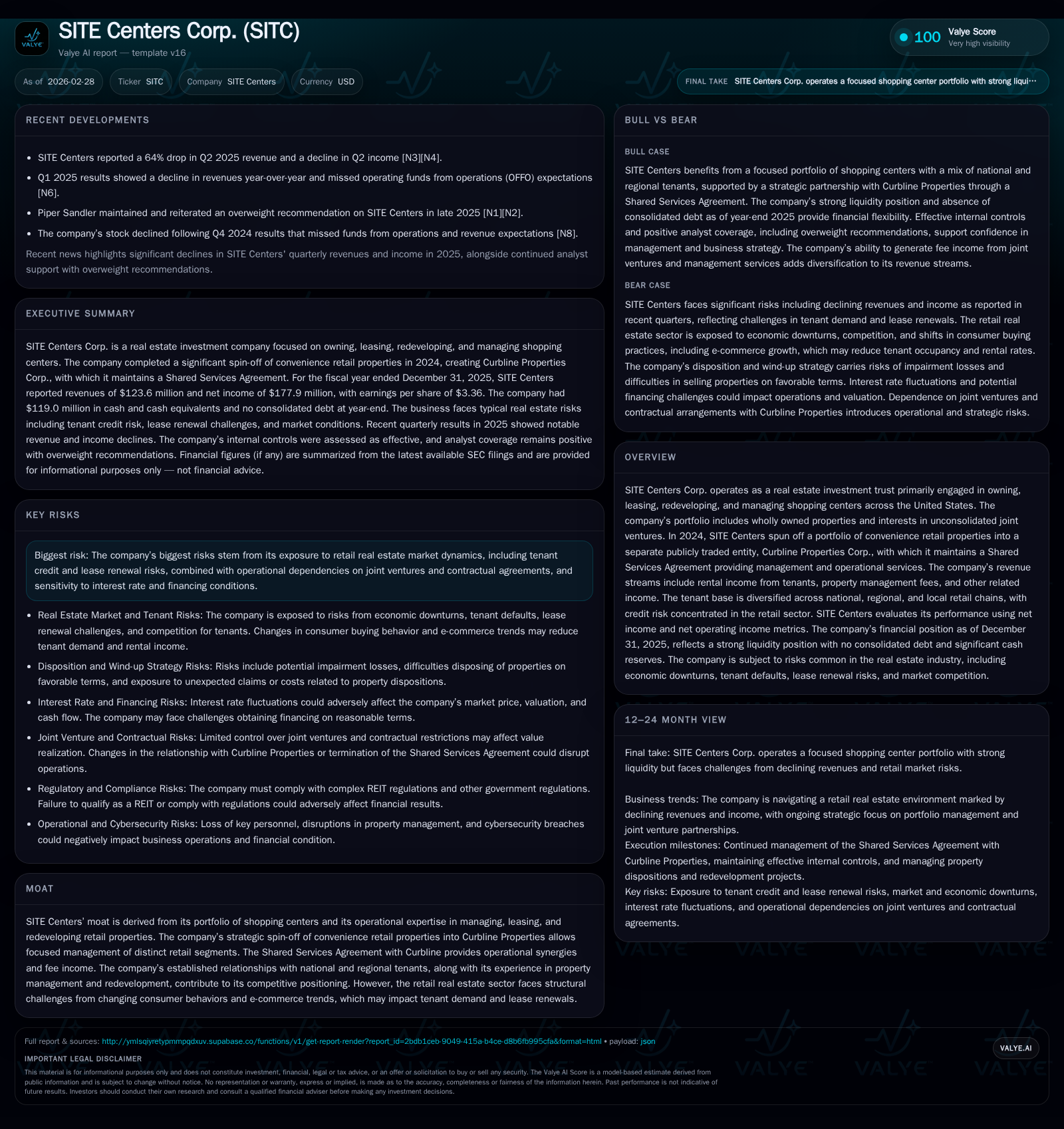

SITE Centers Corp. Navigates Portfolio Spin-Off Amid Retail Sector Challenges

SITE Centers’ 2024 spin-off of convenience retail properties significantly altered its revenue base and capital structure, while the company confronts evolving retail real estate market risks and pursues disciplined capital allocation.

The October 2024 spin-off of a major convenience retail portfolio into Curbline Properties reduced SITE Centers’ revenue by over 55% in FY2025, reshaping its operational focus. Despite this top-line contraction, operating income remained stable year-over-year, reflecting operational efficiencies. SITE Centers completed full repayment of senior notes, mortgage debt, and term loans, reducing leverage but currently operates without a revolving credit facility. Dividend distributions increased substantially in 2025 despite earnings volatility, with no share repurchases executed. The company faces heightened tenant credit risk and lease renewal challenges amid retail sector headwinds and navigates redevelopment complexities tied to joint ventures and contractual obligations with Curbline.

Portfolio Transformation: The 2024 Spin-Off

On October 1, 2024, SITE Centers completed a strategic spin-off of its convenience retail properties portfolio into Curbline Properties Corp., transferring 79 properties totaling approximately 2.7 million square feet of gross leasable area along with $800 million unrestricted cash [S11]. This move dramatically reshaped SITE Centers’ asset base and revenue profile.

As a result, SITE Centers’ annual revenue declined from $277 million in FY2024 to $124 million in FY2025—a decrease of about 55.4%—reflecting the divestiture’s scale [F1]. Net income also decreased significantly from $532 million to $178 million (-66.6%) over the same period [F1]. Despite these declines tied primarily to the spin-off transaction, operating income remained stable year-over-year according to company disclosures [F1], indicating operational efficiency gains or retention of higher-margin assets.

SITE retains an ongoing business relationship with Curbline through a Shared Services Agreement that generates fee income for management services related to the spun-off portfolio [S11][S12].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 124 | 178 | 20 | -55.4% | -66.6% |

| 2024 | 277 | 532 | 112 | -49.2% | +100.2% |

| 2023 | 546 | 266 | 239 | -1.1% | +57.5% |

| 2022 | 552 | 169 | 257 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 356 | 0 | 53.1 |

| 2024 | 128 | 0 | 102.9 |

| 2023 | 121 | 27 | 12.2 |

| 2022 | 120 | 42 | 8.1 |

Source: SEC companyfacts cache [F1].

Note: CapEx data for recent years is unavailable; CFO denotes cash flow from operations.

Retail Market Risks and Tenant Dynamics

SITE Centers operates within a challenging retail real estate environment characterized by:

- Shifts in consumer buying habits favoring e-commerce impacting brick-and-mortar traffic.

- Increased tenant credit risk due to financial stress among retailers including bankruptcy risks.

- Lease renewal uncertainties with potential downward pressure on rents amid changing space needs.

- Competitive pressures from other retail property owners intensifying tenant acquisition and retention efforts.

These factors contribute to volatility in rental revenues and underscore the importance of maintaining tenant quality and lease portfolio stability [S1][S2].

Financial Performance: Earnings Resilience Amid Revenue Decline

The spin-off’s impact is evident in SITE Centers’ financial results:

- Revenue halved between FY2024 and FY2025 due mainly to portfolio divestiture.

- Net income declined more sharply than revenue reflecting transaction-related charges.

- Operating cash flow contracted significantly as reduced rental collections followed asset sales.

- Operating income held steady year-over-year suggesting effective cost management or favorable asset mix post-spin-off.

These results reflect a leaner operational footprint with ongoing liquidity constraints given diminished operating cash flow generation capacity.

Capital Structure and Liquidity Developments

SITE Centers undertook significant debt reduction initiatives through FY2025:

- Full repayment of senior notes using cash on hand and proceeds from mortgage facilities; associated debt extinguishment costs including make-whole premiums were incurred ($6–8 million range) .

- Mortgage facility initiated at $530 million in August 2024 was fully repaid by December 31, 2025.

- Term loan was also repaid ahead of schedule contributing further to deleveraging.

- As of December 31, 2025, SITE operates without any revolving credit facility, relying on cash reserves ($119 million at end-2025) and asset sales for liquidity support [S10].

Debt Extinguishment Costs

The company’s prepayment included make-whole premiums typical under rising interest rate environments demonstrating prudent financial management aimed at long-term cost savings despite upfront expenses .

Capital Allocation: Dividends Maintained Without Buybacks

Post-spin-off capital return priorities include:

- A substantial increase in dividends paid—from $128 million in FY2024 to $356 million in FY2025—reflecting special distributions linked to disposition activity [F1][S4].

- Dividend payments exceed net income for FY2025 indicating use of sale proceeds or cash reserves to fund distributions.

- No common share repurchases occurred during FY2024 or FY2025 contrasting with prior modest buyback activity (~$27 million in FY2023) [F1][S9].

This dividend focus aligns with REIT tax qualification requirements emphasizing consistent shareholder distributions despite earnings variability.

Redevelopment Strategy Under Operational Constraints

Redevelopment activities face complexities including:

- Joint venture structures limiting SITE’s unilateral control over redevelopment decisions affecting timelines and budgets [S21].

- Contractual obligations under the Shared Services Agreement with Curbline requiring ongoing expenditures estimated at about $21 million remaining as of end-2025 out of an initial forecasted $33.7 million at spin-off date [S21].

- External risks such as regulatory approvals delays, labor shortages, supply chain disruptions, and weather impacting construction cost escalation typical within retail real estate development cycles [S2].

These factors create both growth opportunities and contingent liabilities requiring vigilant management oversight.

Outlook: Key Metrics and Risks to Monitor

Investors should closely watch:

- Lease renewal rates and rental terms achieved amid market conditions.

- Tenant credit quality trends given sector volatility.

- Progress on remaining property dispositions balancing liquidity needs against execution risks.

- Redevelopment project completion relative to cost and timing expectations within JV frameworks.

- Financing environment shifts impacting access to new capital absent revolving credit lines.

Together these indicators will inform assessment of SITE Centers’ ability to sustain earnings resilience following its major portfolio repositioning.

This analysis is based exclusively on SITE Centers’ SEC filings through February 28, 2026 and publicly available data referenced herein. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments