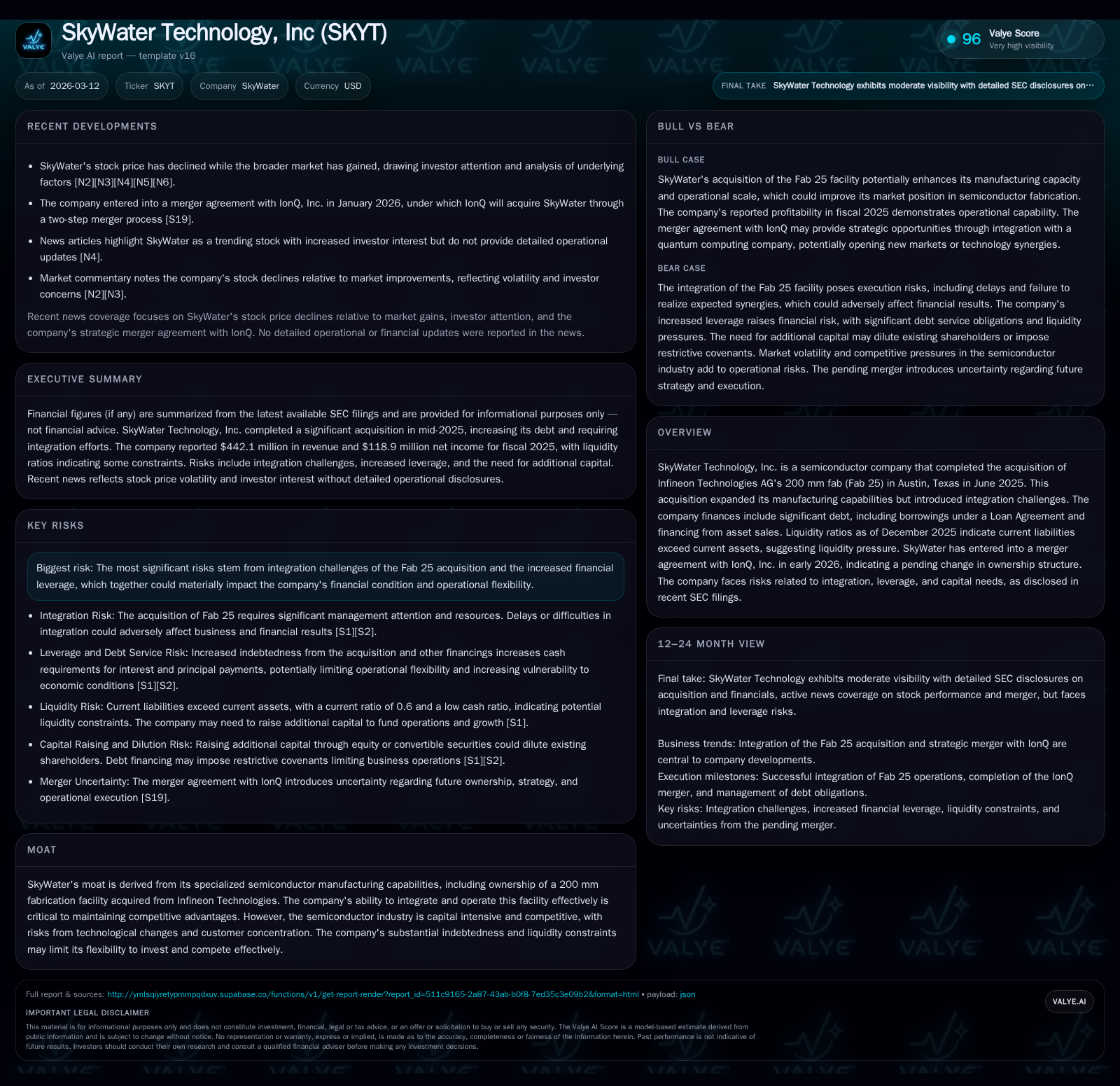

SkyWater Technology's 2025 Surge: Acquisition Benefits and Debt Weigh on Future

SkyWater's acquisition of Infineon's Fab 25 drove a top-line leap in 2025 but added debt and integration risks that cloud financial flexibility.

In 2025, SkyWater Technology capitalized on its strategic acquisition of a 200 mm semiconductor fab from Infineon, resulting in a 29% revenue surge. Despite this growth, the company contended with operating losses and significant leverage that strained liquidity and operational flexibility. The pending merger with IonQ in early 2026 introduces fresh dynamics, with key milestones centering on regulatory approvals and integration synergies amid a capital-intensive environment. Investors should weigh the balance between expansion-driven growth and heightened financial risk tied to increased borrowing.

Acquisition-Driven Revenue Growth Timeline

SkyWater Technology’s fiscal year 2025 marked a pivotal inflection as revenues surged to approximately $442 million, up roughly 29.2% from $342 million in 2024 [F1]. This leap corresponded directly with the June 30, 2025 acquisition of Infineon Technologies AG’s Fab 25, a specialized 200 mm semiconductor fabrication facility situated in Austin, Texas [S2]. The transaction expanded SkyWater's manufacturing bandwidth substantially, positioning it closer to addressing mid-tier wafer demand segments often characterized by complex fab processes distinct from leading-edge nodes.

Despite this revenue acceleration, operating income deteriorated to -$2.58 million from a positive $6.56 million in the prior year [F1], underscoring margin pressure inherent in scaling new fab operations amid integration costs and initial underutilization risks common in wafer fab capacity ramps.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 442 | 119 | -29 | -3 | +29.2% | +1850.5% |

| 2024 | 342 | -7 | 18 | 7 | +19.4% | +77.9% |

| 2023 | 287 | -31 | 10 | -15 | +34.6% | +22.3% |

| 2022 | 213 | -40 | -14 | -30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -53 | 63.3 |

| 2024 | 11 | -11.8 |

| 2023 | 1 | -57.2 |

| 2022 | -31 | -73.8 |

Source: SEC companyfacts cache [F1].

Tables show steady revenue expansion driven by strategic capacity additions but volatile earnings metrics reflecting operational scale-up pains [F1].

Operational Integration Challenges Post-Fab 25 Purchase

Acquiring an active semiconductor fab like Fab 25 includes inheriting complex wafer processing lines, multi-sourced suppliers, and embedded workforce practices unevenly aligned across sites [S2][N4]. Management has flagged significant resource diversion to merge Fab operations effectively and align tooling standards — an undertaking fraught with schedule risk given the precision required for throughput optimization in legacy fabs.

Moreover, expected revenue synergies and cost efficiencies remain contingent on stabilizing production yields and workforce productivity, which historically can lag acquisition timelines in wafer fab consolidations due to equipment re-certifications and process harmonization delays [S2]. The unique nature of a mature fab also restricts rapid capacity expansions without substantial capital investment.

Financial Leverage and Liquidity Constraints Underlining Risk Profile

Post-acquisition indebtedness ballooned materially, from pre-transaction levels to roughly $183.8 million by September-end 2025 [S5][F1], driven largely by borrowings under an amended Loan Agreement providing up to $350 million credit capacity but constrained by borrowing bases tied to accounts receivable, inventory, and equipment valuations [S4][S7]. Interest rates around this debt stand at elevated levels between approximately 8.6% and 8.7%, raising borrowing costs amid tightening monetary conditions [S9][S10].

Liquidity ratios exacerbate concerns — a December-end current ratio near 0.6 highlights current liabilities exceeding current assets by over $130 million [F1], placing stress on working capital management during ongoing expansion phases that typically see cash outflows rise before operational leverage gains accrue.

Additionally, support letters from major stakeholders like Oxbow Industries provide some backstop funding options (up to $12.5 million), yet these are time-bound and subject to renewal uncertainty beyond March 18, 2026 [S4][S5], intensifying refinancing risk horizon.

Evaluating SkyWater’s Profitability: From Operating Losses to Net Income Swing

Although operating results for FY2025 slipped into a modest loss of $2.58 million [F1], net income presented a striking positive turnaround posting approximately $118.9 million net profit versus prior year net losses near $6.79 million [F1]. This disconnect signals significant accounting complexities — likely involving one-time gains such as asset sales or mark-to-market adjustments rather than sustainable operational improvement.

As these non-operating impacts obscure core business profitability assessments, cautious interpretation is warranted for valuation purposes given the capital-intensive context where recurring earnings power traditionally hinges on wafer fab yield improvements and volume scale economics [F1].

Capital Allocation Strategy: Debt Structure, Cash Flows, and Shareholder Returns

Capital expenditures surged over twofold in FY2025 reaching about $24.3 million from around $7.9 million previously — a direct reflection of investments made towards integrating Fab 25 machinery upgrades and capacity scaling efforts [F1]. However, juxtaposed against negative operating cash flow of nearly $29 million, free cash flow generation remains deeply negative by an estimated $53 million annually when subtracting capex expenditures [F1].

Return on equity scores impressively high at roughly 63% based on net income relative to equity base ($118M/$188M), but this metric is influenced disproportionately by non-cash or transient items rather than recurring earnings strength [F1]. Notably absent are any dividends or share repurchase programs amidst tight liquidity buffers — indications that retained earnings prioritize debt servicing and capital reinvestment [S20][S26].

Outlook and Key Milestones Post-IonQ Merger Announcement

Early February 2026 disclosures confirmed a merger agreement whereby IonQ will acquire SkyWater Technology in what represents a convergence of semiconductor manufacturing expertise with emerging quantum computing ambitions [N1][S3]. Expected synergistic opportunities lie primarily in leveraging SkyWater’s specialized fabs toward quantum device production requirements — a market nascent but with high strategic premium.

Closing conditions remain subject to standard regulatory reviews and stockholder approvals slated through late-2026 events linked closely with filings per SEC proxy schedules [S26][N1]. Risks include execution distractions during integration phases alongside potential dilution inherent in share exchange mechanisms outlined under merger terms.

Implications of Increasing Interest Costs on Financial Flexibility

The impact of rising global interest rates amplified SkyWater’s interest burden significantly given its exposure under floating rate loan facilities capped presently near high single digits (8.6%-8.7%) [S9][S10][S11]. The borrowing base restrictions periodically recalibrated against collateral metrics induce further unpredictability around maximum credit availability especially if inventory or receivable turnover weakens during macroeconomic downturns.

These dynamics compress cash flow coverage ratios narrowing leeway for costly refinancing alternatives while concurrently imposing tighter covenants restricting incremental leverage or material asset divestitures absent consent [S11][S17].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments