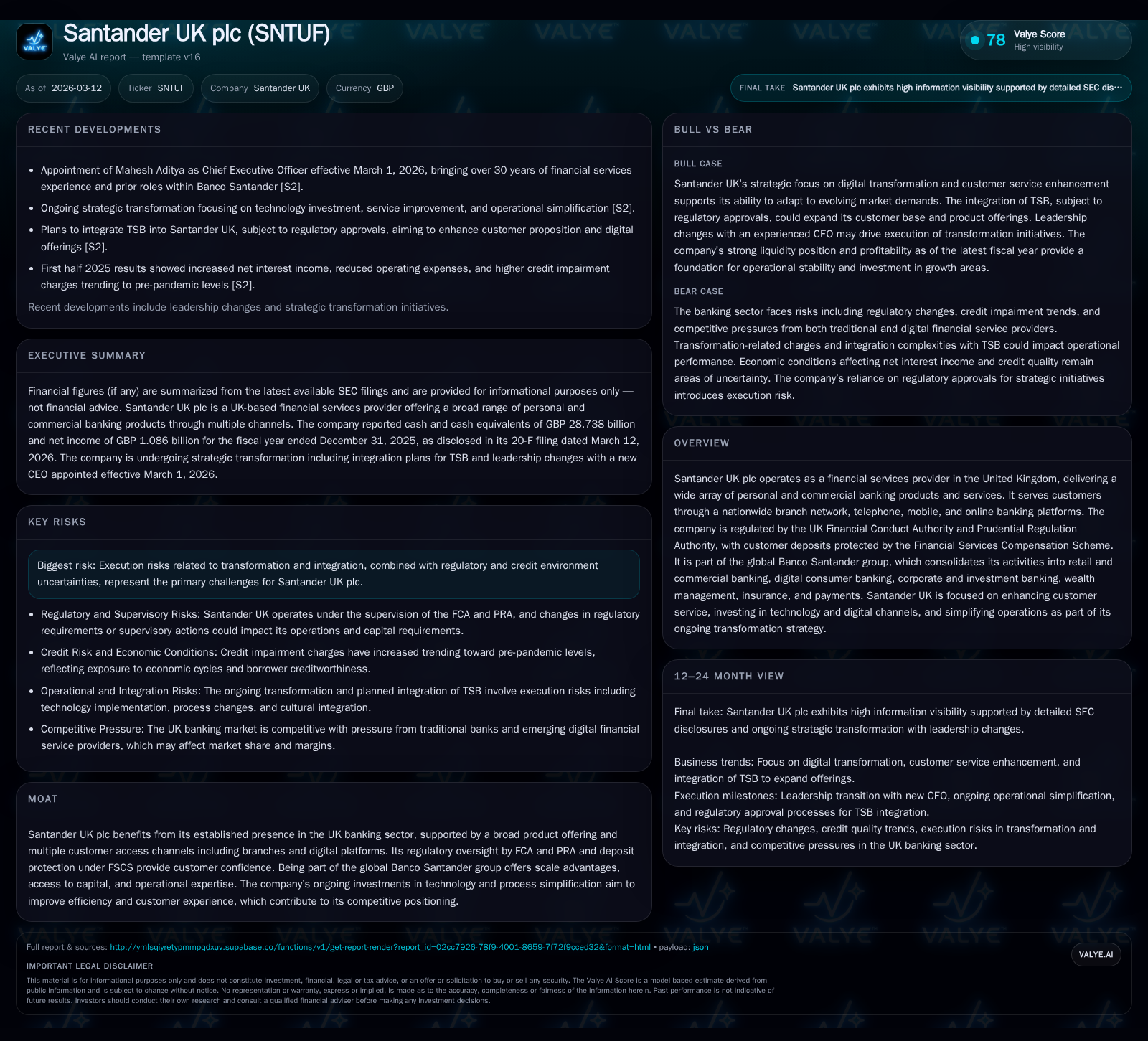

Santander UK’s Evolution: Balancing Digital Expansion and Traditional Banking Strengths

Examining Santander UK's recent financial trajectory, transformation initiatives, and leadership shifts to understand its positioning within the evolving UK banking sector.

Santander UK plc has experienced fluctuating net income over the past four years, peaking in FY2023 before a notable decline in FY2024 and a partial rebound in FY2025. The company is undertaking a strategic transformation from its traditional branch-focused model toward enhanced digital services, supported by investments in technology and operational simplifications. Leadership changes with the appointment of Mahesh Aditya as CEO signal a bolstered focus on risk management and consumer banking best practices. While capital allocation remains disciplined with steady equity growth, regulatory and credit environment risks continue to cap near-term growth potential.

Historical Performance: Trends in Profit and Capital

Santander UK’s financial performance over the last four fiscal years illustrates notable volatility influenced by macroeconomic conditions and strategic adjustments. Net income rose from £1.39 billion in FY2022 to a peak of £1.54 billion in FY2023, representing an uplift driven by solid core banking activities before falling sharply to £971 million in FY2024 due to heightened costs and credit challenges. The latest year saw net income partially recover to £1.086 billion as efficiency initiatives began taking hold [F1].

Equity levels exhibited moderate growth amid profit fluctuations, moving from £14.4 billion at the end of FY2022 up to £15.1 billion by the end of FY2025, reflecting retained earnings and cautious capital deployment [F1]. This capital base underpins an approximate return on equity (ROE) of 7.2% for FY2025, signaling constrained profitability aligned with sector pressures such as interest rate uncertainty.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 1086 | +11.8% |

| 2024 | 971 | -37.0% |

| 2023 | 1541 | +10.5% |

| 2022 | 1394 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 7.2 |

| 2024 | 7.1 |

| 2023 | 10.5 |

| 2022 | 9.7 |

Source: SEC companyfacts cache [F1].

Note: ROE calculated as annual net income divided by equity for that year; cash & equivalents reflect liquid assets held at fiscal year-end.

Transformation Strategy: From Branch Network to Digital Services

Santander UK has embarked on a comprehensive transformation emphasizing expansion of digital channels alongside streamlining legacy operations [S1]. The firm balances maintaining its extensive branch footprint while advancing mobile, online, and telephone banking platforms—aiming for an omnichannel service delivery amid shifting consumer preferences.

Investment focuses include scaling user-friendly digital interfaces and backend automation which can reduce reliance on costly physical branches—a segment challenged by reduced foot traffic industry-wide. Operational reengineering targets cost-to-income ratio improvements critical for sustaining competitiveness amid margin pressures.

Leadership Update and Its Strategic Implications

In January 2026, Santander UK appointed Mahesh Aditya as CEO effective March 1st [S2]. Mr. Aditya’s background is rooted in global risk management at Banco Santander—serving as Group Chief Risk Officer since 2023—and earlier leadership of Santander Consumer USA from 2019-23.

This leadership choice signals emphasis on robust risk governance during the company’s pivot toward digital consumer banking enhanced by prudent credit oversight. His familiarity with U.S. consumer finance markets suggests potential adoption of best practices adaptable for the UK context.

Profitability Drivers and Year-on-Year Shifts

Core profitability drivers revolve around loan book expansion and net interest margins (NIM), though explicit NIM figures are not publicly disclosed [S1]. Fee income streams face pressure amid intensified competition within retail banking products.

FY2024 marked earnings deceleration partly due to elevated impairment charges and regulatory-related expenses reflective of cyclical credit tightening [F1]. The rebound in FY2025 correlates with initial gains from operational efficiencies and normalized credit costs but remains below previous peak levels.

Capital Structure and Liquidity Position

Santander UK maintains a conservative capital structure compliant with Basel III/CRD IV frameworks overseen by the PRA [S3,S8,S11]. Liquidity coverage ratios demonstrate healthy buffers well above minimum requirements bolstered by £28.7 billion cash reserves at end-2025 [F1].

The deposit base remains stable with emphasis on retail customer retention while wholesale funding utilization is tightly controlled through medium-term note programs and structured deposits . Leverage metrics conform within sector standards preserving flexibility for future capital deployment decisions.

Dividend Policy and Capital Allocation

Historically, Santander UK maintained dividend payouts around £668 million prior to 2020 [F1], indicating consistent shareholder returns underpinned by earnings stability until recent operational shifts increased caution.

Due to transformation expenditures and regulatory capital conservation mandates detailed in filings [S1], dividend growth appears moderated post-2019 with no evidence of recent buybacks disclosed.

Capital allocation remains focused predominantly on reinforcing balance sheet resilience rather than aggressive distributions amid ongoing sector headwinds.

Regulatory Environment and Risk Factors Impacting Growth

Operating under dual regulatory supervision from FCA and PRA imposes stringent compliance affecting capital adequacy and lending activities [S7]. Credit environment uncertainties constrain portfolio growth ambitions while heightening impairment provisioning vigilance.

Governance complexity arises from overlapping supervisory requirements impacting liquidity management strategies alongside consumer protection including FSCS deposit guarantees [S1,S7].

Future Prospects: Growth Opportunities and Operational Constraints

Future growth hinges upon successful execution of digital transformation projects designed to enhance customer acquisition and retention through improved service models [S1]. Technological innovation remains pivotal but tempered by execution risks including project delays or integration hurdles common across large incumbents.

Macroeconomic factors like inflation dynamics and interest rates will influence lending demand particularly within commercial portfolios. Competitive intensity within saturated UK retail markets necessitates leveraging Banco Santander group’s scale advantages while avoiding market share gambits risking capital strain.

Key Milestones Ahead and Market Watchpoints

No explicit future guidance disclosed; however key milestones likely include phased digital rollout completions tracked via adoption rate KPIs alongside cost-to-income ratio improvements indicative of operational leverage realization [S1]. Regulatory assessments on capital regime updates remain notable calendar events potentially shaping capital return capacity.

Monitoring credit quality metrics including impairment trends will provide directional signals regarding portfolio health amid volatility.

This analysis summarizes publicly available financial data and company disclosures without providing investment recommendations or forecasts beyond documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments