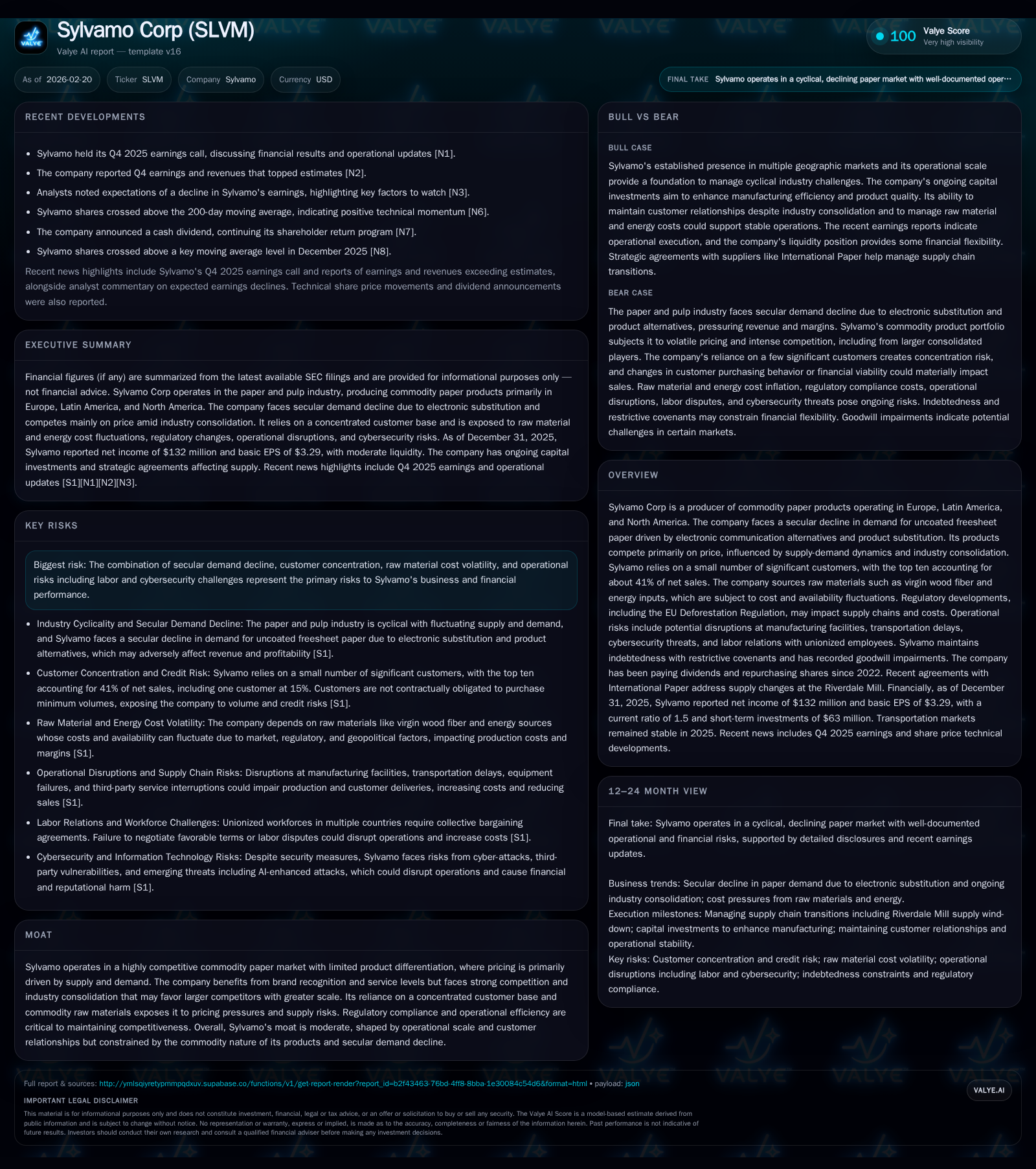

Sylvamo Corp Confronts Commodity Paper Demand Decline and Margin Pressure in a Consolidating Market

Sylvamo operates in a challenging commodity paper industry marked by secular demand decline, raw material cost volatility, and concentrated customer dependencies.

Sylvamo Corp, a global producer of commodity paper products primarily in Europe, Latin America, and North America, faces persistent headwinds from a secular decline in uncoated freesheet paper demand driven by digital substitution. The company’s historical growth has been influenced by industry pricing cycles and operational cost management amidst fluctuating raw material and energy expenses. Despite significant year-over-year declines in operating and net income in 2025, Sylvamo maintains positive cash flow generation and pursues shareholder returns through dividends and share repurchases within debt covenant constraints. Looking ahead, the company’s growth prospects hinge on managing supply chain risks, navigating regulatory complexities including environmental compliance and trade policies, addressing customer concentration challenges, and mitigating operational disruptions. Capital allocation remains disciplined amid leveraging cash flow to reduce debt while balancing investment needs and shareholder distributions.

Company Overview

Sylvamo Corporation is a global producer of commodity-grade uncoated freesheet (UFS) paper products serving Europe, Latin America, and North America. The company's portfolio primarily revolves around UFS paper used in commercial printing and office applications. These end markets have experienced secular demand declines over recent years due to electronic communication replacing traditional paper usage [S21]. With most products being commodities lacking significant differentiation, Sylvamo competes chiefly on cost efficiency and scale to leverage its brand recognition.

Historical Performance

Sylvamo's financial performance over the last several years reflects the broader cyclicality inherent to the paper industry alongside secular headwinds from digital substitution trends. While revenue figures are undisclosed in provided tags, operating income offers insight into profitability trends. Operating income plunged from $453 million in FY2024 to $251 million in FY2025 (-44.6% YoY), signaling margin compression due to inflationary pressures on raw materials like wood fiber, energy costs, plus weaker sales volumes or pricing power under competitive stress [F1][S21].

Net income followed with a steep decrease of 56.3% YoY dropping from $302 million in FY2024 to $132 million in FY2025. Despite this contraction in earnings, Sylvamo generated $268 million operating cash flow in FY2025 — down almost 43% from prior year but still enabling positive free cash flow after deducting elevated capital expenditures which nearly doubled year-over-year to roughly $149 million [F1].

Dividend payments rose annually from $10 million in 2022 to $73 million in 2025 accompanied by opportunistic share repurchases totaling $82 million in FY2025 within an authorized buyback program capped at $450 million as of end-2025 [F1][S7], balancing shareholder rewards against earnings contraction.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 132 | 268 | 251 | -56.3% |

| 2024 | 302 | 469 | 453 | +19.4% |

| 2023 | 253 | 504 | +114.4% | |

| 2022 | 118 | 438 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 73 | 82 | 13.7 |

| 2024 | 62 | 69 | 35.7 |

| 2023 | 57 | 70 | 28.1 |

| 2022 | 10 | 80 | 17.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; Capex data available for selected years only; YoY changes computed where possible based on provided XBRL tags [F1].

Industry Context and Competitive Positioning

The commodity UFS paper market is highly cyclical with significant volume and price volatility caused by macroeconomic shifts affecting industrial nondurables production and consumer spending patterns [S21]. Margins are squeezed during periods of oversupply exacerbated by producers reluctant to idle capacity due to fixed costs. Additionally, customers are consolidating which increases their buying power and exerts downward pressure on pricing. Sylvamo’s moderate moat arises mainly from its operational scale and brand reputation but remains challenged by limited product differentiation inherent to commodity paper businesses [S8].

Key competitors expanding scale through consolidation can leverage procurement synergies that stress smaller players' margins further. Sylvamo must therefore emphasize cost control along with maintaining quality service levels that retain its sizable customer base.

Customer Concentration Risks

Sylvamo generates roughly 41% of sales from its top ten customers alone; the largest customer accounts for approximately 15% of net sales [S6][S8]. This concentration exposes Sylvamo not only to volume loss risks if major customers reduce orders but also increases vulnerability to downstream consolidation effects where large customers demand price concessions.

None of these customers are bound by minimum purchase contracts; as a result order volatility could materially impact financial outcomes unexpectedly [S23]. Furthermore, credit quality deterioration among key customers could delay collections or increase bad debt risk.

Raw Material Sourcing and Cost Pressures

Raw material inputs—particularly virgin wood fiber—represent a majority of production costs along with energy consumables like biomass fuel, natural gas, and electricity [S23].

The company faces exposure to volatilities resulting from weather impacts on forestry yields, logistical constraints influencing transportation costs especially across continents (Europe/Brazil/NA), fluctuating fossil fuel prices affecting energy input prices, plus emerging regulatory frameworks such as the EU Deforestation Regulation increasing compliance burdens around sustainable sourcing. Such factors led to meaningful input cost inflation during 2025 that compressed gross margins despite efforts at price pass-through when market conditions permitted [S10][S23].

Energy efficiency improvements remain critical operational levers given that energy-related expenses form a significant component of manufacturing overheads.

Operational Risks

Manufacturing facility disruptions remain salient risks owing to machinery breakdowns or environmental incidents requiring costly remediation or regulatory penalties [S19][S11]. Labor relations involving unionized mill workers present potential sources of strikes or slowdowns which would interrupt supply chains.

Transportation reliability is central as Sylvamo depends on third-party logistics providers across railways, trucking networks, and seaports; any sudden capacity constraints or rate spikes could inflate delivery costs or degrade service levels impacting customer satisfaction [S14][S24].

Cybersecurity is another growing concern as attacks targeting industrial control systems or corporate IT infrastructure could compromise operational continuity or expose sensitive commercial information leading to reputational damage [S24].

Regulatory Environment

Across all three regions of operation—Europe, Latin America (notably Brazil), North America—Sylvamo must comply with evolving environmental regulations targeting air emissions controls, water discharge limits, hazardous waste handling standards alongside occupational health & safety mandates that require ongoing capital investment and operating expense budget allocations [S19][S11].

Trade measures including tariffs or anti-dumping duties periodically alter competitive dynamics potentially impeding efficient global supply chain functioning particularly if favored local competitors benefit disproportionately from subsidies or protective policies [S10].

Tax controversies like the ongoing Brazilian goodwill amortization deductibility dispute introduce financial uncertainty with potential material tax liabilities pending judicial resolution impacting cash flow planning [S25][S17].

Moreover, anti-corruption statutes across jurisdictions necessitate stringent compliance programs given international operations coupled with third-party partnerships adding complexity around governance responsibilities [S22].

Growth Prospects & Challenges Ahead

Sylvamo’s future growth prospects remain constrained given the secular decline trend for uncoated freesheet papers driven largely by electronic communication alternatives eroding traditional usage sectors such as office printing and publishing magazines/books.

Potential upside drivers include:

- Operational enhancements improving cost competitiveness through technological upgrades reducing waste or energy intensity.

- Strategic focus on niche segments less vulnerable to substitution or value-added specialty papers leveraging existing capacity.

- Managing supply chain resilience amidst global inflationary pressures allowing more stable fulfillment rates preserving customer relationships.[N1][N2]

- Potential participation in industry consolidation either via acquisitions gaining scale or divestitures focusing portfolio on higher-margin assets.

- Navigating regulatory transitions effectively avoiding unforeseen compliance penalties.

Risks capping growth involve sustained demand erosion outpacing efficiency gains causing margin contraction,[N3] intensifying competitive pricing pressures stemming from consolidated buyer power, raw material cost spikes disproportionate to selling price adjustments,[S23], labor shortages driving up wage costs,[S27], transport disruption,[S24], plus geopolitical uncertainties adding volatility to input sourcing particularly for European mills nearest conflict zones.[S1]

Financial Position & Capital Allocation Strategy

As of December 31, 2025, Sylvamo reported current assets of approximately $1.08 billion against current liabilities near $716 million yielding a current ratio around a healthy 1.5x indicative of reasonable short-term liquidity buffers.[F1]

Total stockholders’ equity grew from $678 million at end-2022 to nearly $966 million by end-2025 reflecting retained earnings accumulation despite profit volatility.[F1]

Debt obligations include revolving credit lines ($67 million outstanding), term loans maturing between 2027-2031 aggregating over $685 million combined principal outstanding plus accounts receivable financing facilities totaling approximately $90 million.[S4][F1] This leverage level imposes restrictive covenants limiting discretionary cash uses including dividend payments or share repurchases unless sufficient liquidity thresholds are met.[S15][S7]

Despite profit declines in FY2025 relative to prior years capped dividend payouts rose sequentially reaching $73 million annually demonstrating commitment but constrained room for acceleration under covenant rules.[F1][S7] Similarly, share buybacks continued though at modest scale consuming $82 million during FY2025 keeping pace with board-authorized programs while preserving balance sheet flexibility.[F1]

Free cash flow approximates near $119 million (operating cash flow minus capital expenditures), subject to variability given potential capex demands for compliance investments plus selective operational improvements.[F1] Capital allocation will require balancing debt reductions against investment needs plus continued shareholder returns mindful of cyclicality impacts on profitability.

What To Watch Next (Analysis)

- Quarterly earnings trajectory for signs of stabilization or further margin stress amid input cost trends.

- Developments regarding the Brazil Tax Dispute resolution influencing fiscal outlook.

- Progress on environmental permit renewals affecting production continuity.

- Customer contract dynamics especially changes within top ten clients weightings or purchases.

- Impact of any competitor consolidations altering supply balance causing pricing shifts.

- Effectiveness of cost reduction initiatives yielding margin improvement per ton basis analytics.

- Capital expenditure patterns indicating strategic pivot toward niche product focus or operational modernization.

Conclusion

Sylvamo navigates a structurally declining market where competitive pressures linked to commoditized inputs constrain pricing power amid evolving regulatory landscapes demanding incremental compliance investments. The company must continue leveraging operational discipline while closely managing customer relationships and mitigating supply chain vulnerabilities amid inflationary environments. Capital allocation choices will remain judicious as free cash flow generation supports both debt management goals alongside measured shareholder return programs within covenant bounds. Future performance hinges on how well Sylvamo adapts technologically and strategically within cyclical industry dynamics paired with secular declines complicating long-term growth prospects.

This analysis is based on publicly available information including company SEC filings up to February 20, 2026 ([F1]-[S29]) and recent news transcripts ([N1]-[N6]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments