Summit Midstream Corp Confronts Commodity Price Sensitivity and Customer Concentration Amid Debt Constraints

Latest quarterly results underscore operational stability but highlight persistent risks from debt leverage and customer dynamics.

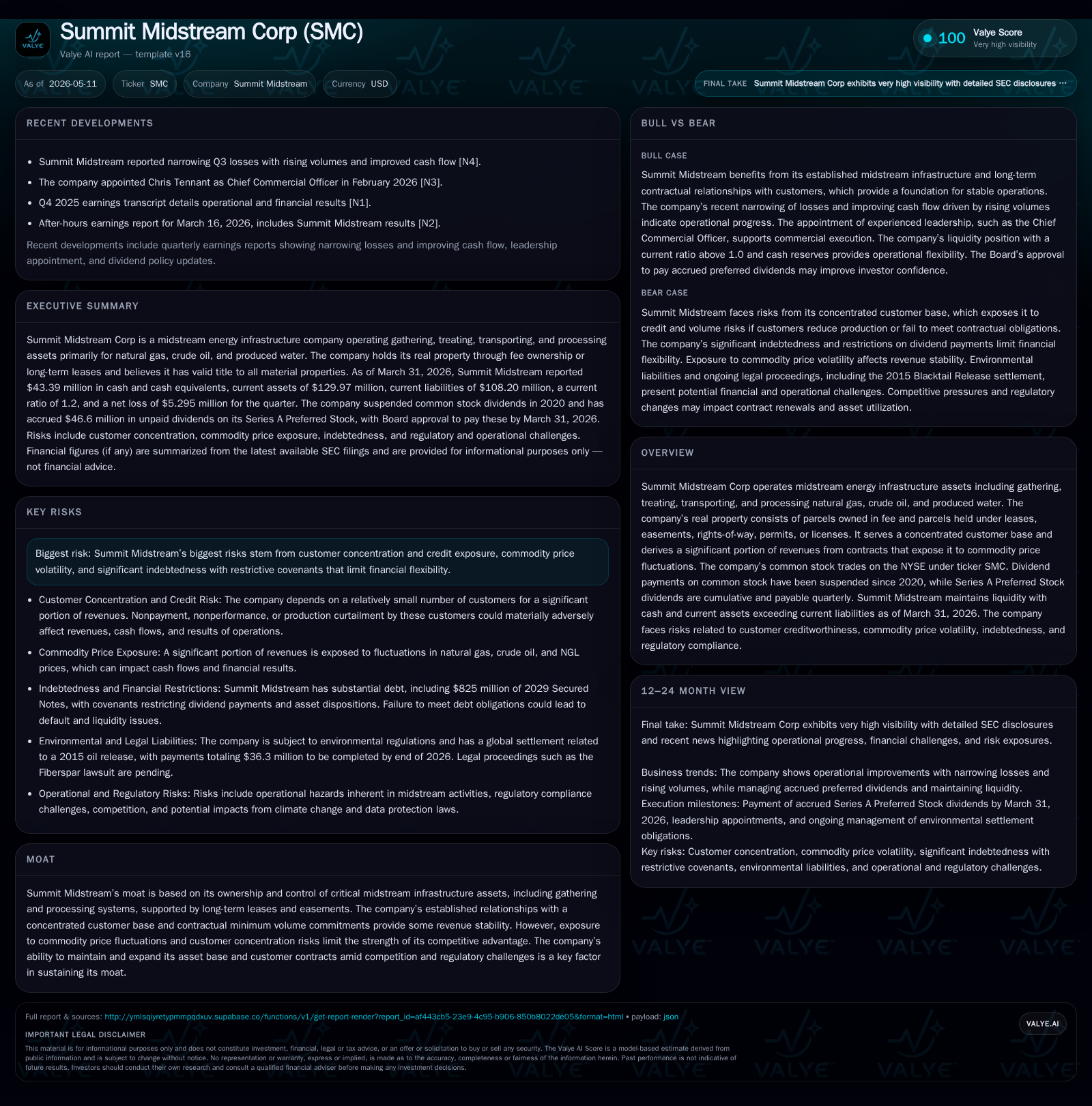

Summit Midstream Corp’s Q1 2026 update signals operational continuity in its midstream infrastructure business, with cash and current assets exceeding liabilities providing near-term financial breathing room. However, the company remains constrained by high indebtedness exceeding $1 billion as of year-end 2025, and significant exposure to a concentrated customer base and commodity price volatility. Dividend payments on common stock remain suspended, reflecting prioritization of debt reduction and capital reinvestment amid restrictive covenants. The firm’s competitive position derives from ownership of critical gathering and processing assets secured by long-term easements, yet growth depends on customer drilling activity and ability to finance necessary expansions. Key watchpoints include upstream production trends, commodity price shifts influencing throughput volumes, resolution of the Fiberspar litigation trial in April 2026, and management’s execution in managing leverage within increasingly complex credit markets.

Recent Operating Update

Summit Midstream Corporation's most recent quarterly filing dated May 11, 2026 ([S2]), together with an event filing released same day ([S3]), provide a near-term snapshot that confirms stable operations but underlines persistent financial constraints. As of March 31, 2026, the company reported cash and equivalents totaling approximately $43.4 million and current assets exceeding liabilities with a current ratio of around 1.2 ([F1]), signaling short-term liquidity adequacy.

However, total outstanding debt remains substantial at about $1.05 billion as of December 31, 2025 ([F1]), resulting in a net debt figure slightly exceeding $1 billion after accounting for cash resources. This heavy indebtedness drives restrictive covenants limiting dividend payments — no dividends have been paid on common stock since suspension in May 2020, per both latest filings ([S1], [S7]). The board recently approved payments of all accrued preferred dividends totaling $46.6 million as of end-2025 ([S24]).

Operationally, Summit continues providing gathering, treating, transporting, and processing services for natural gas, crude oil, and produced water primarily through assets held in fee or long-term lease/easement arrangements ([S1]). Revenue generation hinges significantly on volumes transported through its systems.

Business Model

Summit's core earnings derive from fees charged to upstream producers for midstream services across gathering pipelines and processing facilities. Its infrastructure supports natural gas liquids (NGLs), crude oil streams, produced water handling – effectively covering vital energy value chain segments between production wells and downstream markets.

Key revenue mechanics hinge on contracted minimum volume commitments (MVCs) that establish baseline throughput fees (“take-or-pay” style), but variability arises as actual volumes fluctuate with upstream operators’ drilling activity and market-driven production changes ([S26]). Pricing power is partially durable due to captive asset locations buttressed by easements; however, pricing sensitivity remains given competitive midstream operators nearby offering alternative transport options.

Customer bills depend on:

- Volume: Directly proportional to production levels and successful well completion by customers.

- Rate/Mix: Contractual rates subject to periodic adjustments plus service mix changes (e.g., increased processing vs. simple gathering).

- Contractual Terms: MVC penalties apply if customers under-deliver volumes but enforcement depends on their financial health.

Margins face pressure from operating expenses driven by maintenance of aging pipelines in challenging terrain prone to environmental incidents ([S13]).

Industry Structure and Competitive Position

The midstream energy sector is characterized by capital-intensive infrastructure requiring extensive rights-of-way acquisition amid regulatory scrutiny. Summit's competitive moat largely stems from ownership/control of key pipelines combined with long-term leases/easements ensuring operational continuity absent rapid replacement alternatives ([S1], Valye analysis). This confers moderate pricing resilience versus spot market fluctuations.

Competition arises chiefly from regional midstream operators jockeying to secure customer contracts amid fluctuating upstream activity levels. Summit faces challenges maintaining customer loyalty because producer decisions weigh factors like cost efficiency, capacity availability, geographic proximity, environmental/permitting considerations.

Customer concentration is pronounced: few producers account for a substantial portion of revenue ([S10]), amplifying vulnerability to individual operational or financial disruptions among these counterparties.

Growth Drivers

Growth prospects are linked intrinsically to the broader upstream industry's health:

- Drilling & Completion Activity: Increased fracking/completion efforts drive higher volumes requiring processing/gathering.

- Production Sustainability: Maintaining or growing output levels from existing wells sustains throughput.

- Expansion Capital Investments: Supporting customers’ development programs via new asset construction when economic conditions justify capital deployment ([S18]).

- Fee Contract Adjustments: Opportunities may arise to renegotiate contracts or add ancillary services enhancing per-unit revenue.

Risks / Watchpoints / Growth Constraints

Several interrelated risks constrain Summit’s operational agility:

- Commodity Price Volatility: Downturns reduce upstream activity curtailing volumes; prolonged low-price scenarios risk bankruptcies or contract renegotiations affecting revenues ([S14], [S20]).

- Customer Concentration & Credit Risk: Dependency on few large customers increases exposure to nonpayment or curtailed production incidents ([S10], [S14]).

- Legal / Environmental Liabilities: Pending April 2026 trial related to unpaid claims by Fiberspar Corporation amounting to over $5 million poses uncertainty ([S20]). Ongoing compliance under prior settlements (2015 Blacktail Release) continues affecting cash flows ([S13]).

- Leverage & Covenant Restrictions: Over $1 billion net debt limits flexibility—debt service requirements restrict dividends/investments; covenant breaches could trigger defaults ([S4], [S5], [S8]).

- Capital Market Access: Prevailing investor sentiment unfavourable toward fossil fuel sectors constrains refinancing or equity raises needed for growth capital ([S18]).

- Operational Hazards: Pipelines face risks from natural disasters or accidents impacting system integrity ([S26]).

What to Watch Next

Key upcoming developments likely impacting Summit’s trajectory include:

- Upstream Production Trends: Changes in drilling intensity or well productivity proximate to Summit's infrastructure will signal near-term volume outlook.

- Results from Fiberspar Litigation Trial: Scheduled for April 2026; outcome could affect contingent liabilities or financial provisions substantially.

- Debt Refinancing Efforts: Any announcements regarding maturities or covenant negotiations will clarify financial flexibility constraints.

- Dividend Policy Updates: While common stock dividends remain unlikely absent material business change ([S24]), progress in preferred stock payments will inform overall cash flow priorities.

- Regulatory Environment Changes: New environmental regulations or tariffs impacting operations or supply chains should be monitored closely.

Financial Profile (Latest Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $43mm | |

| 2026-03-31 | ||

| Total debt | $1055mm | |

| 2025-12-31 | ||

| Net debt | $1012mm | |

| 2025-12-31 | ||

| Current assets | $130mm | |

| 2026-03-31 | ||

| Current liabilities | $108mm | |

| 2026-03-31 | ||

| Current ratio | 1.2x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $43.4 million | |

| 2026-03-31 [F1] | ||

| Current Assets | $129.97M | |

| 2026-03-31 [F1] | ||

| Current Liabilities | $108.2M | |

| 2026-03-31 [F1] | ||

| Total Debt | $1.055B | |

| 2025-12-31 [F1] | ||

| Net Debt (est.) | $1.012B | Approximate |

| Current Ratio | 1.2 | |

| 2026-03-31 [F1] |

Despite holding adequate liquidity to cover short-term obligations as reflected by its current ratio above one,[F1] Summit remains highly leveraged which constrains strategic maneuvering.

Disclaimer: This analysis is based strictly on publicly disclosed information as of May 11, 2026 including SEC filings referenced herein. It does not constitute investment advice or recommendations regarding securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments