Synopsys’ $34.9 Billion Ansys Acquisition Reshapes Software Infrastructure Growth Trajectory

The integration of Ansys broadens Synopsys’ software portfolio, creating strategic scale in EDA and simulation amid high leverage and cyclical pressure.

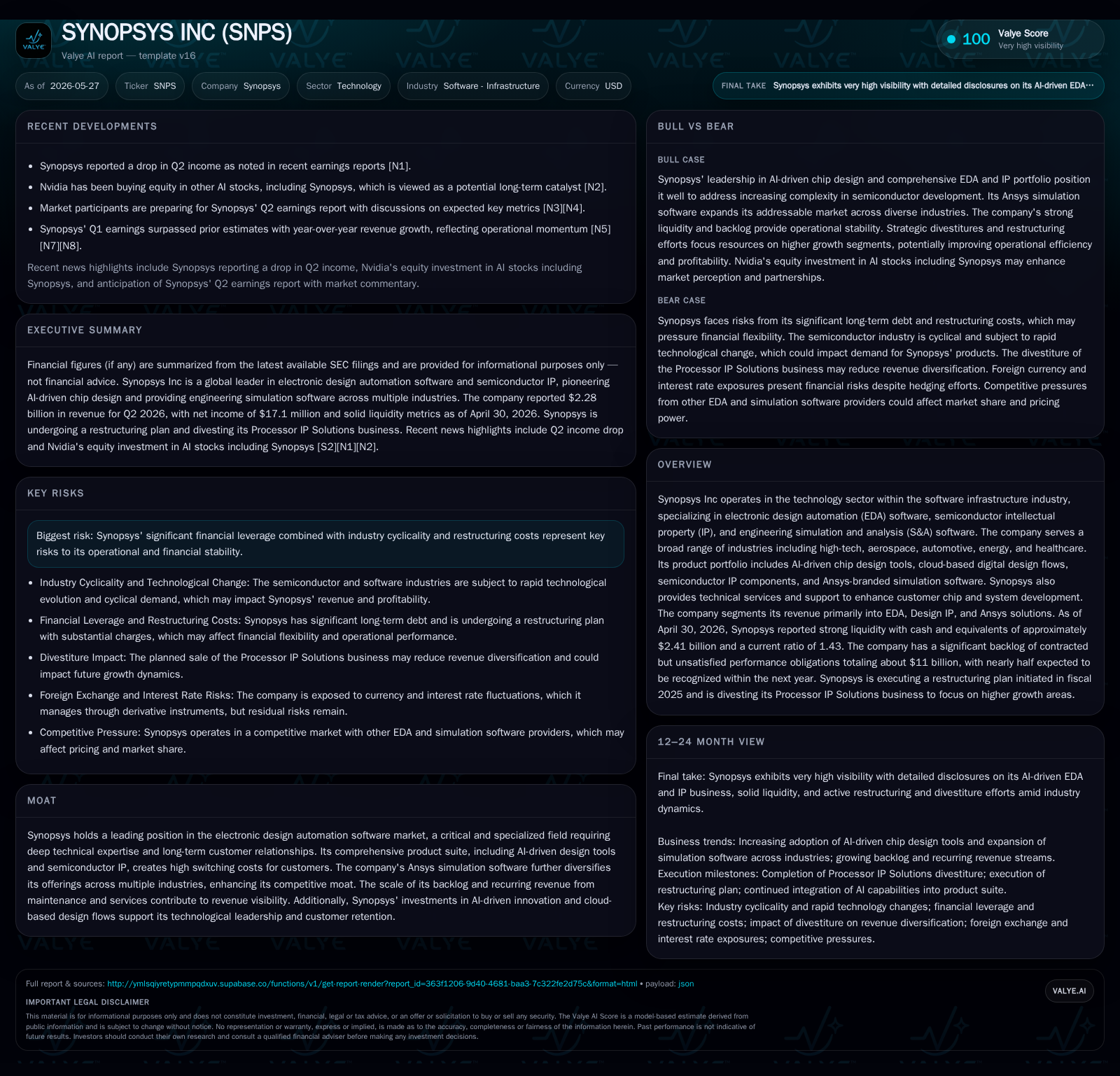

Synopsys completed the transformative $34.9 billion acquisition of Ansys in July 2025, substantially expanding its engineering simulation capabilities and market reach across industries. The latest quarterly filing reveals continued strategic integration efforts alongside operational challenges typical of such a large-scale merger. Synopsys’ core electronic design automation software, semiconductor IP offerings, and new cloud-based AI tools position it as an indispensable partner in chip and system development. However, elevated net leverage around $7.7 billion and industry cyclicality require close monitoring for margin and cash flow stability going forward.

Recent Operating Update

Synopsys Inc executed a landmark acquisition of ANSYS, Inc. on July 17, 2025, priced at approximately $34.9 billion in combined cash and equity consideration [S2][S12]. This deal fundamentally expands Synopsys’ footprint beyond its traditional electronic design automation (EDA) domain into broad engineering simulation and analysis software — an area where Ansys holds significant market leadership. The latest quarterly filing dated May 27, 2026, provides insight into the financial accounting impact of this combination, reporting substantial amortization expenses related to intangibles acquired through the deal ($807.9 million for six months ended April 30, 2026), which weighed notably on operating income [S2].

Concurrently, Synopsys announced the addition of Jesse Cohn to its Board on June 1, 2026 pursuant to a Cooperation Agreement with Elliott Investment Management — an active investor known for pushing governance changes — highlighting heightened shareholder involvement during this critical integration phase [S3]

Synopsys reported robust liquidity with $2.41 billion in cash and equivalents at fiscal quarter-end April 30, 2026 alongside current assets of $5.44 billion against current liabilities of $3.79 billion for a current ratio of approximately 1.43 [F1][S2]. Total debt levels are elevated at roughly $10.11 billion (net debt about $7.7 billion after cash), reflecting leverage undertaken for the Ansys acquisition financing [F1]. This capital structure frames key constraints as the company navigates integration while maximizing operating cash flow.

Business Model Analysis

Synopsys generates revenue primarily through three segments: EDA software licensing & maintenance, semiconductor intellectual property (IP) delivery & licensing, and engineering simulation & analysis principally through the integrated Ansys division [S1]

The traditional EDA business revolves around highly technical software tools used by semiconductor companies to design complex integrated circuits (ICs). These include AI-driven chip design automation products that accelerate logic synthesis, verification, place-and-route operations, and manufacturability checks that are critical before chips move to expensive fabrication phases.

Licenses in this segment are typically sold on subscription or perpetual terms coupled with maintenance contracts that offer updates and technical support — thus contributing significant recurring revenue streams with high customer retention due to switching costs associated with transitioning between intricate toolsets.

The Design IP segment provides silicon-proven semiconducting building blocks such as embedded memories, logic libraries, security IP modules, and interface IPs that customers integrate into chip designs for time-to-market acceleration and risk mitigation [S1].

Ansys’ products complement this offering by enabling simulation across multiple domains—including electronics thermal/EM simulation—as well as aerospace structural analysis and even healthcare device modeling—marking a geographic diversification in end markets beyond the semiconductor industry base.

Synopsys also invests heavily in cloud-based digital design flows powered by AI which enhance collaborative chip development efficiency across dispersed engineering teams while enabling consumption-based pricing models on scalable cloud infrastructure.

Industry Structure and Competitive Position

The global electronic design automation market is oligopolistic with a small number of dominant players possessing proprietary toolchains necessary for advanced semiconductor manufacturing nodes. Synopsys stands among the top-tier firms alongside Cadence Design Systems and Mentor Graphics (now Siemens EDA), leveraging decades of domain expertise.

Its moat is fortified by technical complexity barriers: sophisticated algorithms underlying chip synthesis demand deep specialized knowledge honed over many years; customers face steep learning curves that discourage tool-switching post-adoption.

Moreover, Synopsys' semiconductor IP portfolio creates additional ecosystem lock-in given silicon-proven quality reduces validation cycles—a critical value-add in a capital-intensive industry where errors carry massive cost ramifications.

The addition of Ansys positions Synopsys uniquely to offer end-to-end solutions from chip design to system-level engineering simulation across aerospace, automotive electrification (EV), energy sectors such as renewables grid management systems, and advanced healthcare technology devices where multi-physics simulation is vital.

However, this breadth also invites operational complexity relative to peers focused solely on EDA or standalone simulation software companies like Dassault Systèmes or Siemens PLM.

Growth Drivers

Structural demand drivers include:

- Expansion in AI hardware requiring increasingly complex chips optimized via advanced EDA methodologies.

- Growing adoption of electrified vehicles increasing requirements for semiconductor safety-critical designs supported by stringent verification tools.

- Aerospace sector modernization emphasizing simulation-led product validation aligning well with integrated Ansys offerings.

- Healthcare device innovation relying on multi-physics simulations complements Synopsys’ newly combined capabilities.

- Cloud transition accelerating usage-based licensing models enhancing revenue predictability.

- Ongoing penetration into emerging markets with semiconductor ecosystem growth spurring license expansions.

Synopsys’ investments in AI-enhanced design tools create differentiation by reducing design cycle durations while improving yields—a competitive edge supporting pricing power amidst cyclical semiconductor spending fluctuations.

Risks and Growth Constraints

Key risks center on:

- High financial leverage ($7.7 billion net debt) elevates exposure to rising interest rates or tightening credit markets potentially constraining flexibility [F1][S2].

- Semiconductor industry cyclicality may induce revenue volatility especially if OEM capital expenditures pause impacting new license sales signs.

- Integration risks from combining two sizable complex organizations include cultural alignment challenges and possible disruption in innovation workflows limiting synergy realization.

- Restructuring charges related to overlapping functions or technology rationalization may pressure margins temporarily.

- Competitive threat exists from technology shifts or disruptive entrants developing alternative design methodologies or open-source IP initiatives.

- Geopolitical uncertainties affecting global semiconductor supply chains could impact customer demand patterns unpredictably.

What to Watch Next

Investors should focus on milestones such as:

- Quarterly cadence of revenue growth from the merged Ansys segment demonstrating successful cross-selling synergy execution.

- Renewal rates and net retention metrics in core EDA licenses indicating client satisfaction post-acquisition.

- Progression towards rationalizing overlapping R&D investments without compromising innovation pipeline velocity.

- Stabilization or reduction of leverage through debt paydown plans enabled by operating cash flow improvements.

- Adoption rate trends of cloud-based AI-enhanced workflows signaling forward-looking competitive strength.

- Management commentary regarding how Elliott’s Board representation impacts strategic priorities or capital allocation decisions [S3]

Monitoring these indicators will clarify if Synopsys can sustain its leadership while navigating integration complexities under macroeconomic pressures.

Selected Financial Context

As of April 30, 2026, Synopsys held approximately $2.41 billion in cash equivalents against total current assets near $5.44 billion versus current liabilities around $3.79 billion for a current ratio healthy at 1.43 [F1][S2]. Long-term debt registered near $10.11 billion translates into net debt about $7.7 billion after deducting cash—a direct consequence of funding the Ansys acquisition [F1].

Amortization expense related to intangibles surged substantially post-acquisition—$807.9 million over the last six months compared to markedly lower prior periods—reflecting acquired developed technology and customer relationships amortizing over shorter useful lives than core organic assets [S2]. This elevated non-cash charge depressed GAAP earnings but does not affect operating cash flows directly.

Operating income pre-amortization remains supported by recurring maintenance revenues underpinning revenue visibility despite macro headwinds; managing structural cost efficiencies will be critical going forward as Synergy capture leads margin expansion levers [F1][S2]

This analysis synthesizes recent SEC filings and public disclosures through May 27, 2026 without providing investment research views or price targets.

Financial position in context

As of 2026-04-30, companyfacts shows $2.4bn in cash and equivalents and $10.1bn of total debt [F1]. The same snapshot implies net debt of roughly $7.7bn, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $5.4bn and current liabilities of $3.8bn imply a current ratio near 1.43x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments